UK Partnership Agreement Clause Library

Clause name | Purpose | Clause category | Drafting considerations | Typical use case |

|---|---|---|---|---|

Core | ||||

Parties And Legal Status | Identifies the partners and confirms the business is a partnership. | Formation and structure | State names, addresses, entity types and whether any partner acts through a company or trustee. | Any new partnership formed to trade in the UK. |

Business Purpose And Scope | Defines the activities the partnership is authorised to carry on. | Formation and structure | Avoid overly broad wording if partner authority should be limited by business type. | Partnerships where partners must not bind the firm outside agreed activities. |

Commencement Date | States when the partnership and agreement begin. | Formation and structure | Align start date with tax, accounting, premises and employment arrangements. | A business transferring from sole trader to partnership. |

Partnership Name | Sets the trading name used by the firm. | Formation and structure | Check business name rules, trade marks, domain names and professional restrictions. | Partners trading under a shared firm or practice name. |

Principal Place Of Business | Records the main business address of the partnership. | Formation and structure | Include process for changing address and notifying banks, HMRC, clients and regulators. | Firms operating from premises or a registered professional office. |

Fixed Term Or Partnership At Will | States whether the partnership is indefinite or for a fixed term. | Formation and structure | If not at will, specify term, renewal, break rights and early termination consequences. | Project partnerships or indefinite trading businesses. |

Governing Law And Jurisdiction | Selects the law and courts that govern the agreement. | Compliance and administration | Specify England and Wales, Scotland or Northern Ireland as appropriate. | Partners based in different UK nations or with cross-border dealings. |

Optional | ||||

Entire Agreement | Confirms the written agreement supersedes prior partnership understandings. | Compliance and administration | Do not attempt to exclude liability for fraud or mandatory statutory rights. | Partners have negotiated by email or relied on informal oral promises. |

Core | ||||

Variation Of Agreement | Sets how changes to the agreement must be approved and recorded. | Management and decision-making | Require written consent and decide whether unanimous or special majority approval is needed. | Partnerships expecting changes in profit shares or management rights. |

Optional | ||||

Severance | Preserves the agreement if part of it is unenforceable. | Compliance and administration | Useful where restrictive covenants or penalty-sensitive clauses are included. | Professional firms with post-exit restrictions. |

Core | ||||

Initial Capital Contributions | Records what each partner contributes at the start. | Finance and capital | List cash, assets, goodwill, IP or equipment and state agreed values. | Partners contributing unequal money or business assets. |

Situational | ||||

Additional Capital Calls | Sets when partners must provide further funding. | Finance and capital | Specify approval threshold, contribution proportions and remedies for default. | Capital-intensive businesses needing periodic investment. |

Core | ||||

Capital Accounts | Tracks each partner's capital balance in the firm. | Finance and capital | Define credits, debits, revaluations, losses and treatment on exit. | Partnerships with unequal contributions or complex asset ownership. |

Optional | ||||

Current Accounts | Records drawings, profit allocations and short-term partner balances. | Finance and capital | Distinguish current accounts from fixed capital accounts. | Accountancy, medical or consultancy partnerships with monthly drawings. |

Core | ||||

Profit Sharing Ratio | Sets how profits are divided between partners. | Finance and capital | State fixed shares, variable formula, partner classes and timing of allocations. | Partners want unequal profit shares instead of the statutory equal default. |

Loss Sharing Ratio | Sets how business losses are borne by partners. | Finance and capital | Align with profit shares unless a different risk allocation is intended. | A senior partner funds losses while a junior partner contributes labour. |

Partner Drawings | Controls regular withdrawals against expected profits. | Finance and capital | Set monthly limits, approval rights, clawback and treatment if profits are insufficient. | Partners need predictable monthly income from the business. |

Optional | ||||

Interest On Capital | States whether partners receive interest on capital contributed. | Finance and capital | Specify rate, accrual, payment priority and whether interest is an expense or profit allocation. | One partner contributes significantly more capital than others. |

Situational | ||||

Partner Loans | Regulates money lent by partners to the firm outside capital. | Finance and capital | Document rate, repayment date, priority, security and whether loans need approval. | A partner provides temporary working capital to the firm. |

Core | ||||

Business Expenses And Reimbursement | Sets when partners are reimbursed for partnership expenses. | Finance and capital | Require receipts, spending limits, approval rules and tax-compliant expense categories. | Partners incur travel, software, stock or client entertainment costs. |

Partnership Bank Accounts | Controls opening, operating and signing authority for bank accounts. | Finance and capital | Set authorised signatories, dual approval limits and online banking controls. | Any partnership receiving client or trading income. |

Borrowing And Credit Facilities | Sets limits on taking loans, overdrafts or credit for the firm. | Finance and capital | Specify consent thresholds, security, personal guarantees and maximum debt levels. | Partnerships using overdrafts, asset finance or trade credit. |

Partnership Property | Identifies assets belonging to the firm rather than individual partners. | Finance and capital | List premises, equipment, stock, goodwill, IP, vehicles and ownership evidence. | Partners bring personal assets into business use. |

Situational | ||||

Assets Held In A Partner's Name | Clarifies beneficial ownership of assets registered to one partner. | Finance and capital | Address land, vehicles, IP registrations and trust or nominee arrangements. | A lease or domain name is held by one partner for the firm. |

Core | ||||

Books And Accounting Records | Requires proper books and partner access to records. | Compliance and administration | State software, retention, inspection rights, confidentiality and accountant access. | Partners need transparent financial information and HMRC-ready records. |

Annual Accounts | Requires preparation and approval of yearly partnership accounts. | Compliance and administration | Specify accounting standards, year end, accountant appointment and approval deadline. | All partnerships filing partner tax returns based on annual results. |

Accounting Reference Date | Sets the financial year end for partnership accounts. | Finance and capital | Consider tax basis periods, cashflow, seasonal trading and accountant advice. | A partnership choosing a 31 March or 5 April year end. |

Tax Returns And Partner Tax Responsibilities | Allocates responsibility for partnership and individual partner tax filings. | Compliance and administration | Name the nominated partner and require timely information from each partner. | Any UK partnership required to file a partnership tax return. |

Nominated Partner For HMRC | Appoints the partner responsible for managing the partnership tax return. | Compliance and administration | Include replacement procedure if the nominated partner retires or is unavailable. | Partnerships using HMRC Self Assessment for partnership income. |

Situational | ||||

VAT Registration And Administration | Allocates responsibility for VAT registration, returns and payment. | Compliance and administration | Monitor turnover thresholds, VAT schemes, invoice wording and penalties. | Trading partnerships with taxable supplies near the VAT threshold. |

Core | ||||

Insurance | Requires appropriate business, employer and professional insurance cover. | Compliance and administration | Specify cover types, minimum limits, insured parties and renewal responsibility. | Partnerships with staff, premises, clients or professional liability exposure. |

Situational | ||||

Employees And Payroll | Allocates authority and responsibility for hiring staff and payroll compliance. | Compliance and administration | Define hiring authority, PAYE, pensions, employment contracts and disciplinary decisions. | Partnerships employing administrative, professional or operational staff. |

Workplace Conduct And Equality | Requires partners to comply with equality and workplace conduct obligations. | Compliance and administration | Link to anti-harassment, grievance, disciplinary and staff management policies. | Partnerships with employees, consultants, clients or regulated workplace duties. |

Data Protection | Sets partner duties for handling personal data lawfully. | Compliance and administration | Address controller roles, security, breaches, processors, ICO fees and subject requests. | Firms processing client, customer, employee or patient information. |

Core | ||||

Confidentiality | Protects business, client and partner confidential information. | Compliance and administration | Define exceptions, permitted disclosures, duration and return or deletion of information. | Any partnership handling pricing, client lists, know-how or financial information. |

Situational | ||||

Anti-Bribery And Corruption | Requires partners to avoid bribery and improper inducements. | Compliance and administration | Include gifts, hospitality, facilitation payments, reporting and training obligations. | Partnerships dealing with public bodies, procurement or overseas agents. |

Anti-Money Laundering Compliance | Requires AML checks, monitoring and reporting where applicable. | Compliance and administration | Apply to regulated sectors and define client due diligence and reporting officer duties. | Legal, accountancy, estate agency or trust and company service partnerships. |

Sanctions Compliance | Requires compliance with UK financial sanctions and trade restrictions. | Compliance and administration | Include screening, reporting, payment controls and high-risk client procedures. | Partnerships with international clients, payments or suppliers. |

Health And Safety | Requires safe systems of work and legal health and safety compliance. | Compliance and administration | Assign responsibility for risk assessments, training, reporting and insurance coordination. | Partnerships with workplaces, employees, workshops, clinics or site visits. |

Licences, Permits And Professional Authorisations | Ensures required business licences and professional permissions are maintained. | Compliance and administration | Identify responsible partner, renewal dates, conditions and consequences of breach. | Regulated trades, clinics, hospitality, taxis or professional practices. |

Core | ||||

Partner Duties And Time Commitment | Sets expected work, roles and standards for each partner. | Management and decision-making | Define full-time or part-time commitments, role descriptions and performance review process. | One partner works operationally while another contributes capital or expertise. |

Authority To Bind The Firm | Defines when partners may enter contracts for the firm. | Management and decision-making | Internal limits may not protect against third parties unless clearly communicated. | Partners want spending or contract approval limits. |

Ordinary Course Business Authority | Clarifies transactions partners can make without further approval. | Management and decision-making | Define ordinary course by transaction type, value, risk and business sector. | Retail, consultancy or professional firms with routine client contracts. |

Reserved Matters | Lists decisions needing enhanced approval. | Management and decision-making | Include borrowing, asset sales, hiring, litigation, premises, new partners and dissolution. | Partners need veto rights over high-value or strategic decisions. |

Voting Rights | Sets how partner votes are counted. | Management and decision-making | Choose per capita, profit-share weighted or class-based voting. | A partnership has unequal ownership or senior and junior partners. |

Majority Decision-Making | Sets which matters may be decided by majority. | Management and decision-making | Separate ordinary business from fundamental changes requiring unanimity. | Partnerships with three or more partners needing operational efficiency. |

Unanimous Consent Matters | Identifies decisions requiring all partners' consent. | Management and decision-making | Usually include changing business nature, admitting partners and amending core rights. | Founders want protection against fundamental changes. |

Optional | ||||

Partner Meetings | Sets meeting frequency, notice and procedure. | Management and decision-making | Include quorum, remote attendance, minutes and emergency meeting rules. | Multi-partner firms needing regular formal governance. |

Situational | ||||

Managing Partner | Appoints a partner to manage daily operations. | Management and decision-making | Define powers, reporting duties, remuneration and removal process. | Professional firms with one operational lead. |

Management Committee | Delegates governance to a smaller partner committee. | Management and decision-making | Set composition, election, delegated powers, reporting and reserved matters. | Larger professional partnerships with many equity partners. |

Core | ||||

Conflicts Of Interest | Requires disclosure and management of partner conflicts. | Management and decision-making | Define competing interests, voting exclusions, consent and profit account duties. | Partners have outside businesses, investments or family transactions with the firm. |

Good Faith And Fiduciary Duties | Confirms partners owe duties of honesty, disclosure and loyalty. | Management and decision-making | Do not dilute mandatory fiduciary-style obligations without careful legal advice. | Any partnership where partners share control and confidential information. |

Outside Interests And Competing Businesses | Restricts partners from competing with the firm without consent. | Management and decision-making | Define permitted interests, passive investments, disclosure and remedies. | Consultants, advisers or tradespeople could divert work to separate businesses. |

Accounting For Secret Profits | Requires partners to account for unauthorised benefits from partnership dealings. | Finance and capital | Cover commissions, rebates, referral fees, supplier incentives and related-party gains. | Partners negotiate supplier discounts or referral payments. |

Situational | ||||

Intellectual Property Ownership | Allocates ownership of IP created or used by the partnership. | Formation and structure | Address pre-existing IP, created IP, licences, moral rights and post-exit use. | Software, design, media, consultancy or brand-led partnerships. |

Core | ||||

Goodwill | States how business goodwill is owned, valued and dealt with on exit. | Finance and capital | Define whether goodwill is included in buyout valuation or excluded by agreement. | Client-based practices where reputation and recurring work have material value. |

Situational | ||||

Client And Customer Relationships | Clarifies ownership and management of client relationships and records. | Management and decision-making | Address client lists, handover, data protection, professional rules and non-solicitation. | Professional services firms with portable client relationships. |

Optional | ||||

Branding And Marketing Approval | Controls use of the partnership name, logo and public statements. | Management and decision-making | Set approval for websites, social media, advertising claims and reputation risks. | Consumer-facing or regulated partnerships with public marketing. |

Core | ||||

Admission Of New Partners | Sets how new partners may join the firm. | Partners and membership | Specify consent threshold, capital contribution, deed of adherence and profit share. | Growing firms promoting employees or bringing in investors. |

Situational | ||||

Partner Classes | Creates categories such as equity, salaried or junior partners. | Partners and membership | Clarify voting, capital, profit, risk, employment status and tax treatment. | Professional practices with equity and non-equity partners. |

Optional | ||||

Probationary Partner Period | Allows a trial period before full partner rights apply. | Partners and membership | Define status, pay, notice, capital and conversion criteria. | A firm tests a lateral hire before equity admission. |

Core | ||||

Transfer Of Partnership Interest | Restricts assignment or transfer of a partner's economic interest. | Partners and membership | Distinguish economic assignment from admission to management or partner status. | Preventing a partner from selling rights to an outsider. |

Voluntary Retirement | Sets how a partner may leave by notice. | Disputes and exit | State notice period, handover duties, valuation date and client communications. | A partner wants to leave without dissolving the business. |

Situational | ||||

Expulsion Of A Partner | Allows removal of a partner in specified circumstances. | Disputes and exit | Must be express, clear, exercised in good faith and include fair procedure. | Serious misconduct, fraud, insolvency, regulatory breach or persistent non-performance. |

Compulsory Retirement Events | Triggers exit on specified events affecting a partner. | Disputes and exit | Define insolvency, loss of licence, incapacity, criminal conduct and material breach. | Regulated practices needing automatic removal if eligibility is lost. |

Core | ||||

Death Of A Partner | Sets consequences if a partner dies. | Disputes and exit | Address continuation, estate payment, insurance, valuation and authority to trade. | Partners want the firm to continue after a death. |

Situational | ||||

Incapacity Of A Partner | Deals with long-term illness or inability to participate. | Disputes and exit | Define incapacity evidence, temporary cover, voting rights and buyout triggers. | Small partnerships dependent on each partner's active work. |

Core | ||||

Bankruptcy Or Insolvency Of A Partner | Sets consequences if a partner becomes bankrupt or insolvent. | Disputes and exit | Include notice, suspension of authority, buyout and dealings with trustee in bankruptcy. | Protecting the firm from a partner's personal financial distress. |

Valuation On Exit | Sets how a departing partner's interest is valued. | Disputes and exit | Define valuation basis, goodwill, discounts, expert determination and valuation date. | Any retirement, expulsion, death or buyout scenario. |

Buyout Payment Terms | Sets when and how an exiting partner is paid. | Disputes and exit | Specify instalments, interest, set-off, security and cashflow protection. | The firm cannot afford an immediate lump-sum payment on exit. |

Liabilities After Exit | Allocates responsibility for debts before and after a partner leaves. | Disputes and exit | Use notices to creditors and indemnities, but recognise third-party liability rules. | A retiring partner wants protection from future trading debts. |

Notice Of Partner Changes | Requires notice of retirement, admission or dissolution to relevant parties. | Compliance and administration | Notify clients, suppliers, banks, HMRC, insurers, regulators and public channels. | Reducing apparent authority risk after a partner leaves. |

Situational | ||||

Post-Exit Non-Compete | Restricts a departing partner from competing for a limited period. | Disputes and exit | Keep scope, duration and geography no wider than reasonably necessary. | A partner could immediately open a competing local practice. |

Non-Solicitation Of Clients And Staff | Restricts poaching clients, customers, suppliers or employees after exit. | Disputes and exit | Define protected clients, contact period, duration and legitimate business interest. | Client relationship businesses where goodwill may walk out with a partner. |

Non-Dealing With Clients | Prevents a departing partner from acting for specified clients for a period. | Disputes and exit | Narrowly define clients and period to improve enforceability. | A professional partner has strong personal relationships with key clients. |

Garden Leave For Departing Partner | Keeps a departing partner away from work during notice while still bound. | Disputes and exit | State access restrictions, pay or drawings, duties and maximum period. | A partner resigns to join a competitor. |

Core | ||||

Exit Handover | Requires departing partners to transfer work, records and relationships smoothly. | Disputes and exit | Cover client files, passwords, devices, work in progress and introductions. | A client-facing partner leaves the firm. |

Return Of Partnership Property | Requires return of firm property, data and materials on exit. | Disputes and exit | Include laptops, phones, records, keys, cards, client files and confidential data. | Partners use firm equipment and store documents remotely. |

Internal Dispute Escalation | Creates a staged process for resolving partner disputes internally. | Disputes and exit | Set negotiation meetings, deadlines, without-prejudice status and interim authority. | Deadlock or disagreement over strategy, spending or roles. |

Optional | ||||

Mediation | Requires partners to attempt mediated settlement before litigation or arbitration. | Disputes and exit | Specify mediator appointment, costs, timetable and urgent relief carve-outs. | Partners want confidential, cost-controlled dispute resolution. |

Situational | ||||

Expert Determination | Refers technical issues to an independent expert for decision. | Disputes and exit | Define expert qualifications, procedure, binding effect and manifest error review. | Disputes over valuation, accounts, WIP or profit calculations. |

Optional | ||||

Arbitration | Provides private binding dispute resolution outside court. | Disputes and exit | Specify seat, rules, number of arbitrators, language and interim relief. | High-value or confidential partner disputes. |

Situational | ||||

Deadlock Resolution | Provides a mechanism when partners cannot agree on key matters. | Disputes and exit | Use escalation, casting vote, buy-sell, mediation or winding-up triggers carefully. | Two-partner firms with equal voting rights. |

Shotgun Or Buy-Sell Mechanism | Allows one partner to trigger a buyout process after deadlock. | Disputes and exit | Use cautiously where partners have unequal financial strength or information. | Equal joint venture partnerships needing a clean separation route. |

Core | ||||

Dissolution Events | Identifies events that end the partnership. | Disputes and exit | Override unwanted defaults and distinguish dissolution from partner retirement. | Partners want continuity despite death, retirement or bankruptcy. |

Winding Up Procedure | Sets how assets and liabilities are dealt with after dissolution. | Disputes and exit | Specify liquidator role, asset sales, debt payment order and final accounts. | Orderly closure of the partnership business. |

Priority Of Payments On Dissolution | States order for paying debts, advances, capital and surplus. | Finance and capital | Align with statutory order unless the partners intend a lawful variation. | Partnership assets are sold after closure. |

Continuation Of Business After Exit | Allows remaining partners to continue the firm after a partner leaves. | Disputes and exit | Coordinate with dissolution defaults, buyout rights, notices and business name use. | The firm should survive retirement, death or expulsion of one partner. |

Situational | ||||

Use Of Firm Name After Exit | Controls whether the business name may be used after a partner leaves. | Disputes and exit | Consider goodwill, professional rules, misleading trading names and consent. | A firm name includes the surname of a retiring partner. |

Core | ||||

Limits On Partner Authority | Internally restricts certain acts unless approved. | Management and decision-making | Notify third parties where restrictions should affect external liability. | Preventing unilateral borrowing, asset sales or long-term contracts. |

Liability For Partnership Debts | Explains how partners bear firm debts and obligations between themselves. | Finance and capital | Internal indemnities do not necessarily remove external creditor claims. | Partners want internal contribution rules for loans, leases and supplier debts. |

Liability For Partner Wrongful Acts | Allocates responsibility for loss caused by a partner's wrongful act or omission. | Finance and capital | Coordinate with insurance, indemnities, misconduct and expulsion clauses. | Professional negligence, fraud, misrepresentation or operational accidents. |

Indemnities Between Partners | Requires partners to reimburse the firm for unauthorised or wrongful losses. | Finance and capital | Define covered losses, exclusions, conduct of claims and insurance recoveries. | A partner exceeds authority or breaches compliance obligations. |

Optional | ||||

Internal Limitation Of Responsibility | Limits how losses are allocated internally for specified acts. | Finance and capital | Do not imply protection against third-party claims or unlawful exclusions. | Partners allocate risk for specialist workstreams or departments. |

Situational | ||||

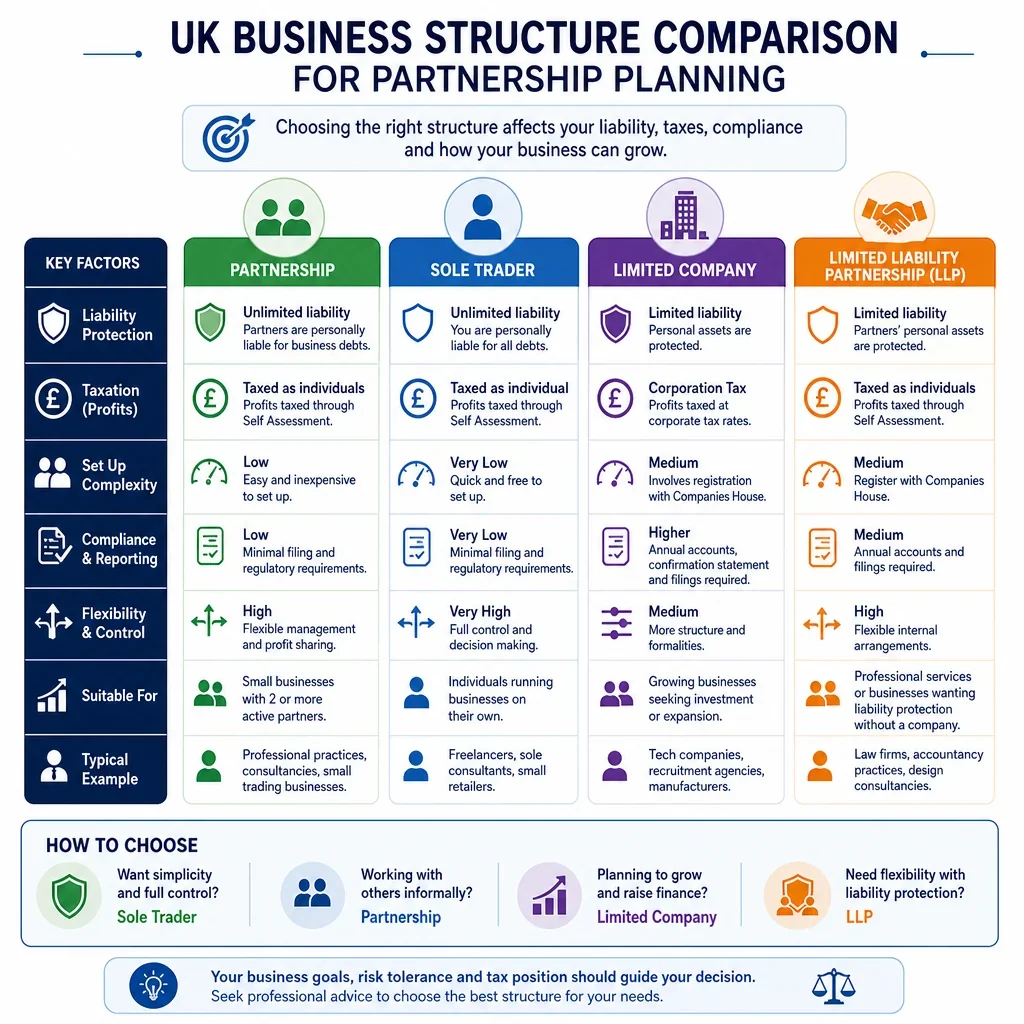

Ordinary Partnership Or LLP Distinction | Clarifies whether the arrangement is an ordinary partnership or LLP. | Formation and structure | Use LLP agreement terms if incorporated as a limited liability partnership. | Partners considering limited liability and Companies House filing duties. |

LLP Designated Members | Appoints LLP members responsible for statutory filings and compliance. | Compliance and administration | Only relevant to LLPs ordinary partnerships do not have designated members. | An LLP needs clear Companies House responsibility. |

LLP Companies House Filings | Allocates responsibility for confirmation statements, accounts and register updates. | Compliance and administration | Only use for LLPs include deadlines, approval process and filing costs. | LLPs required to file accounts and confirmation statements. |

PSC Register And Beneficial Ownership | Requires beneficial ownership information to be collected and maintained where applicable. | Compliance and administration | Relevant mainly to LLPs and companies require members to provide accurate information. | An LLP must identify people with significant control. |

Core | ||||

Notices | Sets how formal notices under the agreement are served. | Compliance and administration | Include email, post, deemed receipt, address updates and urgent notices. | Retirement, default, dispute and variation notices must be validly served. |

Optional | ||||

Electronic Signatures And Counterparts | Allows signing in counterparts and by electronic signature where valid. | Compliance and administration | Use deed formalities where needed and check witnessing rules for deeds. | Partners sign remotely from different locations. |

Situational | ||||

Execution As A Deed | Provides formal execution where deed status is required or preferred. | Compliance and administration | Consider deeds for no consideration, powers of attorney or longer limitation periods. | A partnership deed with restrictive covenants or property-related commitments. |

Core | ||||

No Assignment Of Agreement | Prevents partners transferring rights or obligations without consent. | Partners and membership | Coordinate with transfer of partnership interest and succession provisions. | Maintaining control over who participates in the business. |

Optional | ||||

Force Majeure | Deals with events preventing performance of partnership obligations. | Compliance and administration | Define covered events, notice, mitigation and effect on financial obligations. | Partnerships exposed to premises closure, supply disruption or major IT failure. |

Situational | ||||

Business Continuity And Disaster Recovery | Requires plans for disruption to operations, systems or premises. | Compliance and administration | Cover data backups, authority during emergencies, client communications and insurance. | Partnerships reliant on IT systems, premises or regulated client service continuity. |

Core | ||||

Record Retention | Sets how long business and accounting records are kept. | Compliance and administration | Align tax, VAT, employment, insurance, professional and data retention duties. | Ensuring records are available for HMRC, disputes and client audits. |

Partner Access To Information | Confirms partners may inspect books and obtain firm information. | Management and decision-making | Balance access rights with confidentiality, privilege, data protection and IT security. | A non-managing partner wants visibility over finances and contracts. |

Situational | ||||

Legal Professional Privilege And Client Confidentiality | Protects privileged and professionally confidential client material. | Compliance and administration | Coordinate with regulator rules, data protection, conflicts and exit handover. | Solicitors or regulated legal service partnerships. |

Professional Regulatory Compliance | Requires partners to maintain professional standards and registrations. | Compliance and administration | Identify regulator, practising certificates, CPD, reporting duties and breach consequences. | Law, accountancy, surveyor, medical, dental or financial services practices. |

Client Complaints Handling | Allocates responsibility for handling client or customer complaints. | Compliance and administration | Include escalation, timescales, regulator reporting and compensation authority. | Consumer-facing or regulated professional partnerships. |

Premises And Lease Obligations | Allocates responsibility for business premises and lease commitments. | Finance and capital | Identify tenant, guarantees, rent shares, repairs, fit-out and exit from lease. | Shops, clinics, offices, workshops or hospitality partnerships. |

Personal Guarantees | Controls when partners may give guarantees for firm obligations. | Finance and capital | Require consent, indemnities, release efforts and equality between guarantors. | Bank loans, leases or supplier accounts require partner guarantees. |

Granting Security Over Partnership Assets | Controls mortgages, charges or security over firm property. | Finance and capital | Require approval and check registration requirements for relevant asset type. | Financing equipment, vehicles, stock or premises. |

Optional | ||||

Procurement And Supplier Contracts | Sets approval rules for purchasing and supplier commitments. | Management and decision-making | Set thresholds, preferred suppliers, conflicts and contract review requirements. | Businesses with stock, subcontractors or recurring supplier spend. |

Core | ||||

Litigation And Claims Authority | Controls starting, defending or settling legal claims for the firm. | Management and decision-making | Define approval thresholds, settlement authority, insurance notification and privileged advice. | A customer claim or supplier dispute could affect all partners. |

Optional | ||||

Tax Reserves | Allows the firm to retain funds for tax and liabilities before distributions. | Finance and capital | Specify reserve policy, release timing and treatment on partner exit. | Partnerships with uneven cashflow or large tax payment dates. |

Situational | ||||

Good Leaver And Bad Leaver Treatment | Changes exit value or rights depending on departure circumstances. | Disputes and exit | Define events precisely and avoid penalties or unconscionable valuation outcomes. | Misconduct or voluntary early exit should not receive full goodwill value. |

Retirement Age | Sets any mandatory retirement age or age-related retirement rule. | Partners and membership | Age-based rules need objective justification under equality law. | Professional firms planning succession and equity turnover. |

Family Leave And Extended Absence | Sets treatment of partners during parental, caring or extended leave. | Partners and membership | Address drawings, profit share, cover, voting, discrimination risk and return rights. | Professional partnerships with individual partners taking extended leave. |

Pregnancy And Maternity Protections | Requires decisions affecting pregnant partners to avoid unlawful discrimination. | Partners and membership | Check partner status, maternity arrangements, profit allocation and detriment risks. | A partner takes maternity leave or reduces duties temporarily. |

Disability Adjustments For Partners | Supports reasonable adjustments for disabled partners where required. | Partners and membership | Coordinate role duties, premises, technology, confidentiality and equality obligations. | A partner needs adjusted working arrangements due to disability. |

Suspension Of Partner Rights | Allows temporary restriction of duties, access or voting during serious issues. | Disputes and exit | Use fair process, limited duration, confidentiality and emergency client protection. | Investigation of fraud, misconduct, regulatory breach or safeguarding risk. |

Partner Misconduct Procedure | Sets investigation and decision process for alleged partner misconduct. | Disputes and exit | Include notice, evidence, representation, conflicts, sanctions and appeal. | Handling harassment, dishonesty, persistent breach or professional misconduct allegations. |

Whistleblowing And Protected Disclosures | Provides a route for reporting wrongdoing and protects lawful disclosures. | Compliance and administration | Coordinate with employment status, regulator reporting and confidentiality limits. | Regulated or employer partnerships where staff or partners report wrongdoing. |

Modern Slavery Compliance | Requires supply-chain controls and statements where legally required. | Compliance and administration | Relevant for larger businesses or high-risk supply chains assign due diligence duties. | Partnerships in retail, construction, manufacturing, care or labour supply chains. |

Consumer Law Compliance | Requires compliance when supplying goods, services or digital content to consumers. | Compliance and administration | Address pricing, cancellation rights, complaints, refunds and marketing claims. | Retail, ecommerce, training, fitness or consumer service partnerships. |

Website And Online Trading Compliance | Allocates responsibility for legal requirements of online sales and websites. | Compliance and administration | Cover terms, privacy notices, cookies, distance selling, accessibility and platform accounts. | Partnerships selling services or products through a website. |

Environmental Compliance | Requires compliance with waste, pollution and environmental duties. | Compliance and administration | Assign responsibility for permits, waste transfer notes, hazardous materials and inspections. | Manufacturing, construction, healthcare, food or vehicle repair partnerships. |

Optional | ||||

Subcontractors And Consultants | Controls appointment and management of external contractors. | Management and decision-making | Address approval, contracts, IR35, confidentiality, IP and insurance. | Partnerships using freelancers, locums, associates or delivery contractors. |

Situational | ||||

Off-Payroll Working And Status Checks | Allocates responsibility for contractor employment status and tax checks. | Compliance and administration | Check whether off-payroll rules apply and keep status determinations on file. | Partnerships engaging contractors through personal service companies. |

HMRC Enquiries And Tax Investigations | Sets who manages HMRC enquiries and how costs are shared. | Compliance and administration | Include cooperation duties, access to records, adviser appointment and indemnities. | HMRC opens a compliance check into partnership returns. |

Key Person Insurance And Proceeds | Provides funding and allocation rules for insurance on key partners. | Finance and capital | Align policy ownership, trust arrangements, tax advice and buyout obligations. | Funding a deceased or incapacitated partner buyout. |

Cross-Option On Death | Gives survivors and estate matching options to buy or sell the deceased interest. | Disputes and exit | Coordinate with wills, inheritance tax advice, insurance and valuation provisions. | Family business or professional firm wants succession certainty. |

Core | ||||

Rights Of A Deceased Partner's Estate | Defines what the estate receives and whether it has management rights. | Disputes and exit | Usually limit estate to economic rights and information needed for valuation. | A deceased partner's spouse or executors are not intended to join the firm. |

Situational | ||||

Profits After Dissolution Or Exit | Deals with profits made using an outgoing partner's share after exit. | Disputes and exit | Agree interest or profit share alternative to avoid statutory uncertainty. | Buyout payment is delayed while the firm continues trading. |

Work In Progress And Unbilled Fees | Allocates value of unfinished work at accounts or partner exit. | Finance and capital | Define valuation method, write-offs, contingency fees and client billing risk. | Law, accountancy, consultancy or project-based partnerships. |

Optional | ||||

Bad Debts And Write-Offs | Controls how unpaid invoices and write-offs affect profits and partners. | Finance and capital | Set authority to write off debts and treatment in profit allocation or exit valuation. | Client service firms with credit exposure and uncollected fees. |

Situational | ||||

Partner Salaries Or Priority Profit Shares | States whether partners receive fixed remuneration before residual profits. | Finance and capital | Clarify whether payments are salary-like drawings or priority profit allocations. | A managing partner receives extra reward for operational duties. |

Optional | ||||

Performance Bonuses | Allows additional profit allocation based on performance measures. | Finance and capital | Define metrics, discretion, timing, tax treatment and disputes over calculations. | Sales-led or professional firms rewarding client origination. |

Partner Performance Review | Creates a process for reviewing partner contribution and conduct. | Partners and membership | Link outcomes to profit share, duties, training, warnings or exit triggers. | Firms with unequal workloads or performance-based profit sharing. |

Situational | ||||

Training And Continuing Professional Development | Requires partners to maintain skills and professional competence. | Compliance and administration | Specify minimum CPD, records, costs and regulator requirements. | Regulated professions needing annual training evidence. |

Information Security And Cyber Controls | Requires controls to protect firm systems, data and accounts. | Compliance and administration | Cover passwords, MFA, device use, backups, breach reporting and access removal. | Partnerships using cloud accounting, client portals or remote working. |

Optional | ||||

Remote And Hybrid Working | Sets rules for partners working away from business premises. | Management and decision-making | Address availability, supervision, confidentiality, health and safety and data security. | Partners work from home or different regional offices. |

Core | ||||

Access To Digital Accounts | Controls ownership and access to email, cloud, banking and platform accounts. | Compliance and administration | Ensure firm-owned accounts, admin rights, password controls and exit removal. | A partner sets up key software or social media in their own name. |

Optional | ||||

Social Media And Public Communications | Controls statements made on behalf of or about the firm. | Management and decision-making | Cover authority, confidentiality, defamation risk, advertising rules and account ownership. | Partners promote the firm through LinkedIn, X, Instagram or YouTube. |

Situational | ||||

Related Party Transactions | Controls transactions involving partners, relatives or connected businesses. | Management and decision-making | Require disclosure, independent approval, market terms and voting exclusions. | The firm rents premises or buys services from a partner's company. |

Optional | ||||

Gifts And Hospitality | Controls acceptance and giving of gifts or hospitality. | Compliance and administration | Set thresholds, registers, approvals and anti-bribery escalation. | Partnerships involved in procurement, referrals or public sector work. |

Charitable Donations And Sponsorship | Controls donations, sponsorships and community spending by the firm. | Finance and capital | Set budget, approval, branding, tax treatment and conflicts checks. | Local partnerships sponsoring events or charities. |

Core | ||||

Bank Mandate Changes | Sets process for adding or removing bank signatories. | Finance and capital | Coordinate with exits, suspensions, dual approval and fraud controls. | A partner retires or a finance partner is appointed. |

Situational | ||||

Change Of Control Of Corporate Partner | Controls ownership changes in a company that is a partner. | Partners and membership | Define control, notification, consent rights and deemed transfer consequences. | A limited company holds a partnership interest. |

Nominees And Trust Arrangements | Controls partners holding interests or assets for others. | Partners and membership | Require disclosure of beneficial owners and consider tax, AML and PSC duties. | A partner holds an interest through a trust or nominee arrangement. |

Optional | ||||

Succession Planning | Plans future leadership, ownership and client transition. | Partners and membership | Link to admission, retirement, valuation, mentoring and key client handover. | Founder-led firms preparing for retirement or promotion of juniors. |

No Waiver | Prevents delay or leniency from waiving contractual rights. | Compliance and administration | Still act consistently and document waivers expressly where intended. | A firm tolerates late capital payments but wants to preserve remedies. |

Third Party Rights | States whether non-partners can enforce terms of the agreement. | Compliance and administration | Exclude or identify rights for estates, affiliates, indemnified persons or successors. | Departed partners, estates or group companies may benefit from indemnities. |

Costs Of Preparing The Agreement | Allocates legal, accounting and formation costs. | Finance and capital | State whether costs are partnership expenses or borne individually. | Partners incur professional fees before trading begins. |

Situational | ||||

Pre-Formation Liabilities | Allocates debts or commitments incurred before the partnership formally starts. | Formation and structure | List contracts, deposits, loans and whether the firm adopts or reimburses them. | One founder signed a lease or bought equipment before formation. |

What Clauses Should A UK Partnership Agreement Usually Include?

A UK partnership agreement should usually deal with capital, profit sharing, partner authority, decision-making, admission and retirement, accounts, disputes, and dissolution. Without clear drafting, default rules under the Partnership Act 1890 may apply, including equal profit sharing, broad partner authority, and dissolution consequences that may not match the partners' commercial expectations.

Why Are Default Partnership Rules Risky?

The default statutory position can be unsuitable for modern businesses. For example, partners may be jointly liable for firm debts and each partner may bind the firm when acting in the usual course of partnership business. A written agreement can narrow internal authority, require consent for major decisions, and set clear financial rules, although third-party protection rules still need careful handling.

Which Clauses Are Especially Important For UK Tax And Compliance?

Clauses on accounts, tax responsibility, drawings, expenses, record keeping, VAT, data protection, anti-money laundering checks, and PSC or Companies House obligations where relevant help partners manage day-to-day compliance. These clauses should reflect whether the arrangement is an ordinary partnership, an LLP, or a regulated professional practice.

How Can A Partnership Agreement Reduce Exit Disputes?

Exit clauses should cover retirement notice, compulsory expulsion, death or incapacity, valuation, payment terms, restrictive covenants, client handover, and continuing use of the business name. These provisions are particularly important because partner exits often affect ownership, liability, goodwill, staff, premises, and client relationships at the same time.

FAQs

You Might Also Be Interested In