UK Business Structure Comparison For Partnership Planning

Overview | Legal personality | Liability position | Management approach | Common use cases |

|---|---|---|---|---|

Ordinary partnership | ||||

Two or more people carrying on business together with a view to profit. | No separate legal personality | Unlimited personal liability | Partners usually manage directly, subject to any partnership agreement. | Small professional firms, family businesses, joint ventures and low-admin co-owned businesses. |

Limited liability partnership | ||||

A body corporate used by members who want partnership-style flexibility with limited liability. | Separate legal personality | Limited liability | Members manage under an LLP agreement default rules apply if no agreement covers an issue. | Professional services, consultancies, property ventures and member-managed businesses seeking liability protection. |

Limited company | ||||

A registered company owned by shareholders or guarantors and run through company law rules. | Separate legal personality | Limited liability | Directors manage the company shareholders control major ownership decisions. | Scalable trading businesses, investment-backed startups, subsidiaries and businesses wanting clear ownership shares. |

Sole trader | ||||

An individual trading personally, keeping business profits after tax and bearing business risk. | No separate legal personality | Unlimited personal liability | The owner makes all decisions and may hire staff or contractors. | Freelancers, consultants, tradespeople and early-stage one-person businesses. |

Limited partnership | ||||

A partnership with at least one general partner and one limited partner. | Depends on jurisdiction or arrangement | Mixed liability | General partners manage limited partners risk losing protection if they take part in management. | Private funds, investment holding structures and passive investor arrangements. |

Ordinary partnership | ||||

Default law can impose equal profit sharing unless partners agree otherwise. | No separate legal personality | Unlimited personal liability | Every partner may usually take part in management unless agreed otherwise. | Co-founders wanting a simple structure but needing bespoke profit and authority terms. |

Limited liability partnership | ||||

An LLP must be registered and make public filings at Companies House. | Separate legal personality | Limited liability | Designated members handle key statutory filing and administrative duties. | Businesses accepting more compliance in exchange for limited liability and partnership-style tax treatment. |

Limited company | ||||

A share structure can separate ownership, voting rights, dividends and management roles. | Separate legal personality | Limited liability | Board-led management with shareholder rights set by articles and any shareholders agreement. | Startups issuing shares, businesses seeking external investors and companies with non-managing owners. |

Sole trader | ||||

A one-owner business may become a partnership if another person joins as co-owner for profit. | No separate legal personality | Unlimited personal liability | Single-owner control until ownership or profit-sharing arrangements change. | Testing a business alone before admitting a partner or incorporating. |

Limited partnership | ||||

Limited partners contribute capital but generally should not manage the business. | Depends on jurisdiction or arrangement | Depends on role or agreement | General partner controls operations limited partners remain passive to preserve limited liability. | Capital raising from passive investors where a general partner controls the venture. |

Ordinary partnership | ||||

Each partner can usually bind the firm when acting in the ordinary course of business. | No separate legal personality | Unlimited personal liability | Authority limits should be documented because partners may create obligations for the firm. | Trading partnerships where spending limits, contract authority and bank mandates need control. |

Limited liability partnership | ||||

LLPs allow flexible member arrangements while remaining a separate registered entity. | Separate legal personality | Limited liability | Members can allocate voting, profits, duties and exit terms by LLP agreement. | Senior professionals sharing profits without adopting a shareholder-director model. |

Limited company | ||||

A company separates the entity, directors, shareholders and business assets. | Separate legal personality | Limited liability | Directors owe statutory duties and manage day-to-day operations. | Owner-managed companies where personal and business assets should be separated. |

Sole trader | ||||

The simplest UK business form for one person, with no Companies House incorporation. | No separate legal personality | Unlimited personal liability | Owner-managed with minimal formal governance requirements. | Low-risk solo work where incorporation or partnership governance is unnecessary. |

Limited partnership | ||||

A limited partnership must be registered to obtain limited partnership status. | Depends on jurisdiction or arrangement | Mixed liability | Formal role separation between managing general partners and passive limited partners. | Structured investment ventures needing recognised investor classes. |

Ordinary partnership | ||||

Without tailored terms, default dissolution rules can disrupt the business. | No separate legal personality | Unlimited personal liability | Agreement should cover retirement, expulsion, death, buyout and continuation. | Any continuing co-owned business needing succession and exit planning. |

Limited liability partnership | ||||

An LLP continues as a body corporate despite changes in membership. | Separate legal personality | Limited liability | Membership changes are managed through the LLP agreement and statutory filings. | Firms expecting partner admissions, retirements or succession over time. |

Limited company | ||||

Ownership can change by share transfer without necessarily changing the company entity. | Separate legal personality | Limited liability | Directors continue managing unless changed under company procedures. | Businesses needing transferable ownership, succession planning or employee share incentives. |

Sole trader | ||||

Profits are treated as the owner's income rather than divided between partners. | No separate legal personality | Unlimited personal liability | No internal profit allocation or partner voting rules are needed. | Solo trading where all income, goodwill and decisions belong to one person. |

Limited partnership | ||||

Scottish partnerships generally have separate legal personality, unlike English partnerships. | Depends on jurisdiction or arrangement | Mixed liability | General partner management remains central Scottish personality affects legal holding and proceedings. | Scottish limited partnerships and fund structures needing UK-jurisdiction analysis. |

Ordinary partnership | ||||

In Scotland, a firm is a legal person distinct from the partners. | Depends on jurisdiction or arrangement | Unlimited personal liability | Partners still typically manage directly, subject to agreement and Scots law context. | Scottish professional firms and family businesses needing jurisdiction-specific drafting. |

Limited liability partnership | ||||

LLPs are commonly taxed broadly like partnerships when carrying on business with a view to profit. | Separate legal personality | Limited liability | Members usually agree drawings, profit shares and tax reserves internally. | Profit-sharing professional businesses wanting limited liability without company-style dividends. |

Limited company | ||||

Company profits belong to the company and may be paid out through salary or dividends. | Separate legal personality | Limited liability | Directors decide distributions subject to profits, company law and shareholder rights. | Businesses retaining profits, paying dividends or reinvesting through a corporate vehicle. |

Ordinary partnership | ||||

The partnership and partners must register with HMRC for Self Assessment. | No separate legal personality | Unlimited personal liability | A nominated partner is responsible for partnership tax returns and records. | Small partnerships comfortable with tax administration but not Companies House filings. |

Limited liability partnership | ||||

An LLP needs members and designated members with statutory responsibilities. | Separate legal personality | Limited liability | Designated members take compliance responsibility all members can agree wider management roles. | Firms wanting named compliance leads without creating directors and shareholders. |

Limited company | ||||

A company must keep statutory records and file accounts and confirmation statements. | Separate legal personality | Limited liability | Directors are responsible for company records, filings and statutory registers. | Businesses willing to accept public filings for credibility and limited liability. |

Sole trader | ||||

A sole trader can employ staff without becoming a partnership or company. | No separate legal personality | Unlimited personal liability | Owner remains in control and is responsible for employer obligations. | Solo-owned businesses expanding operational capacity without sharing ownership. |

Limited partnership | ||||

The structure distinguishes active management from passive capital participation. | Depends on jurisdiction or arrangement | Mixed liability | General partner or manager runs the business limited partners monitor through reserved rights. | Private equity, venture capital, real estate and infrastructure funds. |

Ordinary partnership | ||||

Ordinary partnerships generally avoid Companies House incorporation and public accounts filing. | No separate legal personality | Unlimited personal liability | Governance can remain private if recorded in a non-public partnership agreement. | Private co-owned ventures prioritising low publicity over liability protection. |

Limited liability partnership | ||||

LLPs provide limited liability but require public registration and ongoing filings. | Separate legal personality | Limited liability | Internal LLP agreement stays private, but statutory information is filed publicly. | Professional partnerships balancing confidentiality of internal terms with public registration. |

Limited company | ||||

Ownership is usually represented by shares rather than partnership interests. | Separate legal personality | Limited liability | Economic and voting rights are structured through shares, articles and shareholder agreements. | Businesses needing different share classes, option plans or formal investor rights. |

Ordinary partnership | ||||

Partners owe duties of good faith, accounting and disclosure to each other. | No separate legal personality | Unlimited personal liability | Partners should document conflicts, outside activities and information-sharing rules. | Close working relationships where trust, loyalty and transparency are commercially important. |

Limited liability partnership | ||||

Member duties and restrictions are usually developed in a bespoke LLP agreement. | Separate legal personality | Limited liability | Agreement can set duties, reserved matters, non-competes, garden leave and expulsion triggers. | Professional and advisory firms protecting clients, goodwill and confidential information. |

Limited partnership | ||||

Limited partners contribute capital and have limited liability up to that contribution. | Depends on jurisdiction or arrangement | Depends on role or agreement | Capital and withdrawal rules should preserve the intended liability position. | Investor participation where exposure is linked to committed capital. |

Which UK Business Structure Best Fits A Partnership Agreement?

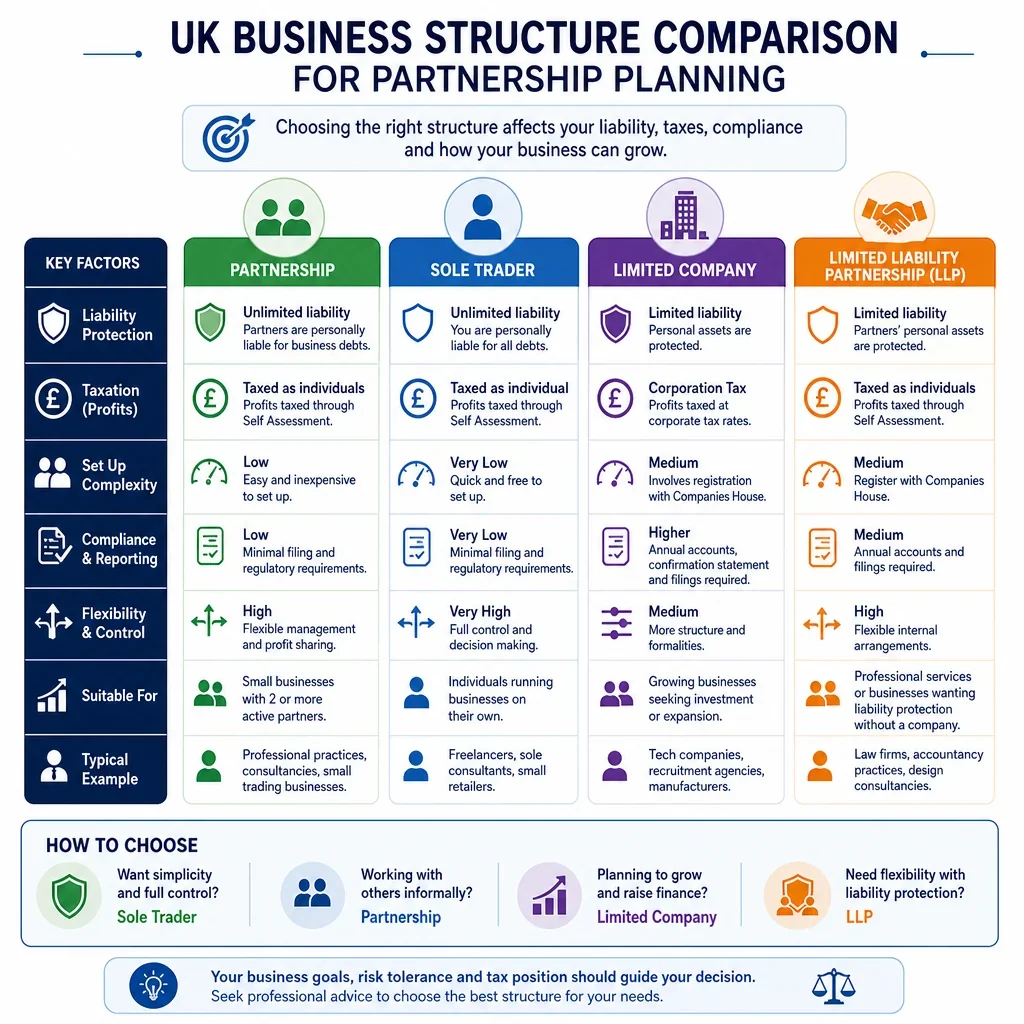

Ordinary partnerships are simple and flexible, but partners usually have unlimited personal liability and each partner can bind the firm in the ordinary course of business. A written partnership agreement is especially important to control profit shares, decision-making, exits, restrictive covenants, drawings and dispute resolution.

When Should Founders Consider An LLP Instead?

A limited liability partnership may be better where the business needs partnership-style internal flexibility but the members want a body corporate with separate legal personality and limited liability. LLPs also require public filings at Companies House, so they involve more administration and transparency than an ordinary partnership.

Why Compare A Partnership With A Limited Company?

A limited company usually offers limited liability and a clearer shareholder/director structure, but governance is based on company law, articles and shareholder agreements rather than a partnership agreement. It is often better for raising equity investment or separating ownership from day-to-day management.

What Is The Main Risk Of A Limited Partnership?

A limited partnership has mixed liability: general partners manage the business and are liable for debts, while limited partners can benefit from limited liability only if they do not take part in management. This makes the structure common for investment funds, but unsuitable where all participants want equal management rights.

Can A Sole Trader Use A Partnership Agreement?

A sole trader does not need a partnership agreement because there is only one owner and no separate business personality. If another person joins as a co-owner, the business may become a partnership and should have a written agreement before profits, losses, authority and exit rights become unclear.

FAQs

You Might Also Be Interested In