Financial Disclosure Items For Prenuptial Agreements In The United Kingdom

Disclosure Item | What to Include | Example Evidence | Disclosure Importance | Valuation Notes |

|---|---|---|---|---|

Property | ||||

Family home | Address, ownership shares, mortgage, equity and occupation rights. | Land Registry title register, mortgage statement, valuation report. | High | Use recent market appraisal deduct mortgage and sale costs if relevant. |

Second home or holiday home | Address, ownership, use, mortgage and estimated equity. | Title register, mortgage statement, estate agent valuation. | High | Consider seasonal markets, rental potential and capital gains tax. |

Buy-to-let property | Property value, mortgage, rental income, tenancy and expenses. | Tenancy agreement, rent statements, title register, mortgage statement. | High | Value may depend on tenancy terms, yield and tax position. |

Overseas property | Location, legal owner, value, mortgage and local restrictions. | Foreign title deed, local valuation, mortgage documents, tax bills. | High | Convert currency and check local ownership, tax and sale costs. |

Land or development plot | Title, acreage, planning status, restrictions and estimated value. | Title plan, planning documents, valuation, option agreement. | High | Planning permission can materially change value. |

Property held through a company or trust | Beneficial interest, control rights, property value and liabilities. | Company filings, trust deed, title documents, accounts. | High | Look through structure where practical legal and tax advice may be needed. |

Bank Accounts | ||||

Current accounts | Bank, account holder, balance, overdraft and regular payments. | Recent bank statements, online balance screenshots. | High | Use a consistent valuation date and include overdrafts separately if material. |

Savings accounts | Provider, account type, balance, interest rate and access restrictions. | Savings statements, passbook, online account summary. | High | Note notice periods, fixed terms and early withdrawal penalties. |

Cash ISAs | Provider, balance, product type and withdrawal terms. | ISA statement, provider summary, annual tax certificate. | Medium | Tax-free status affects income but not basic capital value. |

Premium Bonds | Holder number, total holding and any unclaimed prizes. | NS&I statement, online account record, prize history. | Medium | Capital value is usually the holding amount prizes are variable. |

Foreign bank accounts | Country, currency, holder, balance and access restrictions. | Foreign bank statements, online balance, exchange rate record. | High | Convert using agreed date exchange rate and note transfer limits. |

Investments | ||||

Stocks and shares ISAs | Provider, portfolio value, holdings and investment risk level. | ISA valuation, portfolio statement, platform report. | High | Market values fluctuate use a clear valuation date. |

Listed shares | Company, number of shares, market price and account holder. | Broker statement, share certificate, portfolio valuation. | High | Value at quoted market price consider dealing costs and tax. |

Unit trusts and investment funds | Fund name, units, value, platform and income distributions. | Platform statement, fund valuation, tax voucher. | High | Use latest unit price and note exit charges or illiquidity. |

Investment bonds | Provider, surrender value, withdrawals and tax status. | Provider statement, surrender valuation, policy document. | Medium | Surrender value may differ from headline value and may trigger tax. |

Gilts and government bonds | Issuer, nominal amount, maturity, coupon and market value. | Broker statement, custody statement, valuation report. | Medium | Market value changes with interest rates and maturity date. |

Private company shares | Company, share class, percentage, rights and estimated value. | Share certificate, Companies House filing, accounts, valuation. | High | Minority discounts, restrictions and lack of market can reduce value. |

Cryptocurrency and digital assets | Asset type, wallet or exchange, quantity and sterling value. | Exchange statements, wallet records, transaction history. | High | Highly volatile value at agreed date and keep transaction records. |

Share options and employee share schemes | Scheme type, grants, vesting dates, exercise price and restrictions. | Award letters, scheme rules, employer portal, tax documents. | High | Unvested or conditional awards may need specialist valuation. |

Gold, bullion and commodities | Type, weight, purity, storage location and market value. | Purchase receipts, storage certificates, dealer valuation. | Medium | Use spot price less dealer spread and storage or sale costs. |

Pensions | ||||

Defined contribution pension | Provider, scheme, fund value, contributions and access age. | Annual pension statement, online valuation, contribution record. | High | Use current fund value note tax limits and withdrawal restrictions. |

Defined benefit or final salary pension | Scheme name, accrued benefits, retirement age and transfer value. | Annual benefit statement, cash equivalent transfer value, scheme booklet. | High | Transfer value may not reflect true income value actuarial advice may help. |

State Pension entitlement | Forecast amount, qualifying years and pension age. | State Pension forecast, National Insurance record. | Medium | Usually disclosed as income expectation rather than capital asset. |

Self-invested personal pension | Provider, investments, fund value, charges and nominated beneficiaries. | SIPP statement, portfolio valuation, provider documents. | High | Underlying assets may be illiquid or hard to value. |

Pension in drawdown | Remaining fund, withdrawals, tax-free cash used and income level. | Drawdown statement, payment history, tax statement. | High | Distinguish capital fund from taxable income withdrawals. |

Annuity income | Provider, annual income, indexation, guarantees and survivor benefits. | Annuity policy, payment statements, P60. | Medium | Usually valued as income stream capital value may be unavailable. |

Business Interests | ||||

Sole trader business | Trading name, assets, profits, liabilities and goodwill. | Accounts, tax returns, bank statements, asset list. | High | Goodwill and maintainable earnings may require accountant valuation. |

Partnership interest | Profit share, capital account, drawings and exit terms. | Partnership agreement, accounts, tax returns, capital account statement. | High | Partnership deed may restrict sale or valuation method. |

LLP member interest | Capital contribution, profit share, drawings and member rights. | LLP agreement, accounts, Companies House filings, tax returns. | High | Check retirement, expulsion and transfer provisions. |

Limited company shareholding | Company, shares, voting rights, dividends, loans and salary. | Accounts, confirmation statement, share register, dividend vouchers. | High | Consider earnings, assets, minority discount and shareholder restrictions. |

Director loan account | Balance owed to or from company and repayment terms. | Company accounts, loan account ledger, board minutes. | High | Positive or overdrawn balances can change net asset position. |

Business premises owned personally | Property value, rental arrangements, mortgage and business use. | Title register, lease, accounts, valuation, mortgage statement. | High | Separate property value from trading business value. |

Business intellectual property | Patents, trademarks, copyright, licences and income streams. | IPO registrations, licence agreements, royalty statements. | Medium | Value depends on enforceability, income and remaining protection period. |

Personal Possessions | ||||

Cars, motorcycles and other vehicles | Make, model, owner, finance, mileage and estimated value. | V5C, finance agreement, valuation guide, sale listing. | Medium | Deduct hire purchase or PCP settlement figure where relevant. |

Jewellery and watches | Description, owner, insured value and estimated resale value. | Insurance schedule, purchase receipt, jeweller valuation. | Medium | Insurance value can exceed resale value use realistic market value. |

Art, antiques and collectibles | Description, provenance, ownership, insurance and estimated value. | Auction valuation, provenance records, insurance schedule. | Medium | Condition, provenance and market demand strongly affect value. |

Boats, aircraft and leisure vehicles | Asset details, owner, finance, storage costs and value. | Registration, finance agreement, broker valuation, insurance schedule. | Medium | Maintenance, mooring, depreciation and sale costs can be significant. |

High-value household contents | Items over agreed threshold, owner, value and location. | Insurance schedule, receipts, photographs, valuations. | Low | Second-hand value is often much lower than replacement value. |

Income | ||||

Employment salary and wages | Employer, gross pay, net pay, benefits and deductions. | Payslips, P60, employment contract, P11D. | High | Use recent annualised income and note variable hours or bonuses. |

Bonuses and commission | Expected, historic and discretionary payments with conditions. | Bonus letters, payslips, employment contract, employer statement. | High | Average several years if variable distinguish guaranteed from discretionary. |

Self-employed income | Turnover, profit, drawings, tax and business expenses. | Tax returns, SA302, accounts, business bank statements. | High | Normalise income where profits fluctuate or expenses are discretionary. |

Dividend income | Company, amount, frequency and sustainability of dividends. | Dividend vouchers, tax return, company accounts, bank statements. | High | Dividends may depend on company profit and director control. |

Rental income | Gross rent, expenses, mortgage interest and net income. | Tenancy agreement, rent statements, tax return, letting account. | High | Allow for voids, repairs, agent fees and tax treatment. |

Trust income or distributions | Trust name, entitlement, distributions and trustee discretion. | Trust accounts, distribution statements, trust deed, tax vouchers. | High | Discretionary interests are harder to value than fixed entitlements. |

Maintenance received | Payer, amount, duration and whether court ordered. | Court order, child maintenance calculation, bank statements. | Medium | Reliability and duration affect financial planning. |

State benefits and tax credits | Benefit type, amount, claimant and review dates. | Award notices, bank statements, Universal Credit journal. | Medium | Means-tested benefits can change after marriage or cohabitation. |

Debts | ||||

Residential mortgage | Lender, balance, rate, term, repayment type and secured property. | Mortgage statement, offer, redemption statement. | High | Deduct from property value note early repayment charges. |

Personal loans | Lender, balance, rate, monthly payment and term. | Loan agreement, statement, credit report. | High | Use settlement figure if different from statement balance. |

Credit card balances | Provider, balance, limit, interest rate and minimum payment. | Recent statements, online account summary, credit report. | High | Balances can change quickly use current statement date. |

Overdrafts | Bank, current balance, limit, interest and fees. | Bank statement, account summary, facility letter. | Medium | Treat used overdraft as debt, not a negative bank asset. |

Student loans | Plan type, balance, repayments and expected write-off terms. | Student Loans Company statement, payslip deductions, online account. | Medium | Repayments are income-linked balance may not equal practical burden. |

Tax liabilities | HMRC debt, tax year, type, penalties and payment plan. | HMRC statement, self assessment account, payment plan letter. | High | Include accrued interest, penalties and upcoming balancing payments. |

Business debts and trade creditors | Creditor, amount, due date, security and personal liability. | Accounts, creditor ledger, loan agreements, invoices. | High | Clarify whether debt is personal, company or guaranteed. |

Personal guarantees | Guaranteed debt, creditor, limit, trigger and secured assets. | Guarantee deed, facility letter, security documents. | High | Contingent liability may need risk assessment, not simple face value. |

Pending claims or litigation liabilities | Claim type, parties, amount claimed, prospects and costs exposure. | Court papers, solicitor letters, settlement offers, insurance response. | High | Value is uncertain include legal costs and insurance cover. |

Loans from family or friends | Lender, amount, terms, repayments and whether documented. | Loan agreement, bank transfers, messages, repayment records. | High | Distinguish genuine repayable loan from informal gift. |

Expected Inheritance | ||||

Known expected inheritance | Source, estimated amount, timing and conditions if reasonably known. | Will extract, estate accounts, solicitor letter, family trust documents. | Medium | Inheritances are uncertain until received avoid overstating certainty. |

Future trust entitlement | Trust name, beneficiary status, vesting date and trustee discretion. | Trust deed, trustee letter, accounts, beneficiary statement. | High | Discretionary interests may have no fixed value but are still relevant. |

Inheritance from estate in probate | Estate, entitlement, estimated net value and expected distribution date. | Grant of probate, estate accounts, executor correspondence, will. | High | Deduct estate debts, tax and administration expenses. |

Other Assets | ||||

Life assurance with surrender value | Provider, policy owner, beneficiaries, surrender value and premiums. | Policy schedule, surrender value statement, annual statement. | Medium | Term life cover may have no asset value unless surrender value exists. |

Endowment policies | Provider, maturity date, surrender value and linked mortgage if any. | Annual statement, surrender quote, policy document. | Medium | Maturity projection may differ from current surrender value. |

Personal injury or compensation claim | Claim type, expected award, interim payments and restrictions. | Solicitor letter, medical report, settlement offer, court documents. | Medium | Awards may include future care needs and may be uncertain. |

Money owed to you | Debtor, amount, due date, security and repayment history. | Loan agreement, invoice, bank transfer, acknowledgment of debt. | Medium | Discount if recovery is doubtful or debtor has limited means. |

Expected tax refunds | Tax year, refund type, amount claimed and status. | HMRC correspondence, self assessment account, refund calculation. | Low | Treat as uncertain until accepted or paid by HMRC. |

Expected Inheritance | ||||

Inheritance Tax Act 1984 references for estate values | Potential estate tax affecting expected net inheritance. | Estate accounts, IHT forms, executor calculations. | Medium | Inheritance should be considered net of tax and estate liabilities. |

Other Assets | ||||

Financial circumstances relevant under Matrimonial Causes Act 1973 | Income, earning capacity, property, resources, needs and obligations. | Full asset schedule, income evidence, liability statements. | High | Relevant because court considers resources and obligations on divorce. |

Pensions | ||||

Pension sharing legislation relevance | Pension rights that could be relevant to financial remedies. | Pension statements, transfer values, scheme information. | High | Pensions require careful valuation because income value may exceed transfer value. |

Other Assets | ||||

Understanding financial implications before signing | Enough disclosure for each party to understand the agreement. | Disclosure schedules, asset summaries, independent legal advice letters. | High | Major omissions may reduce weight given to the agreement. |

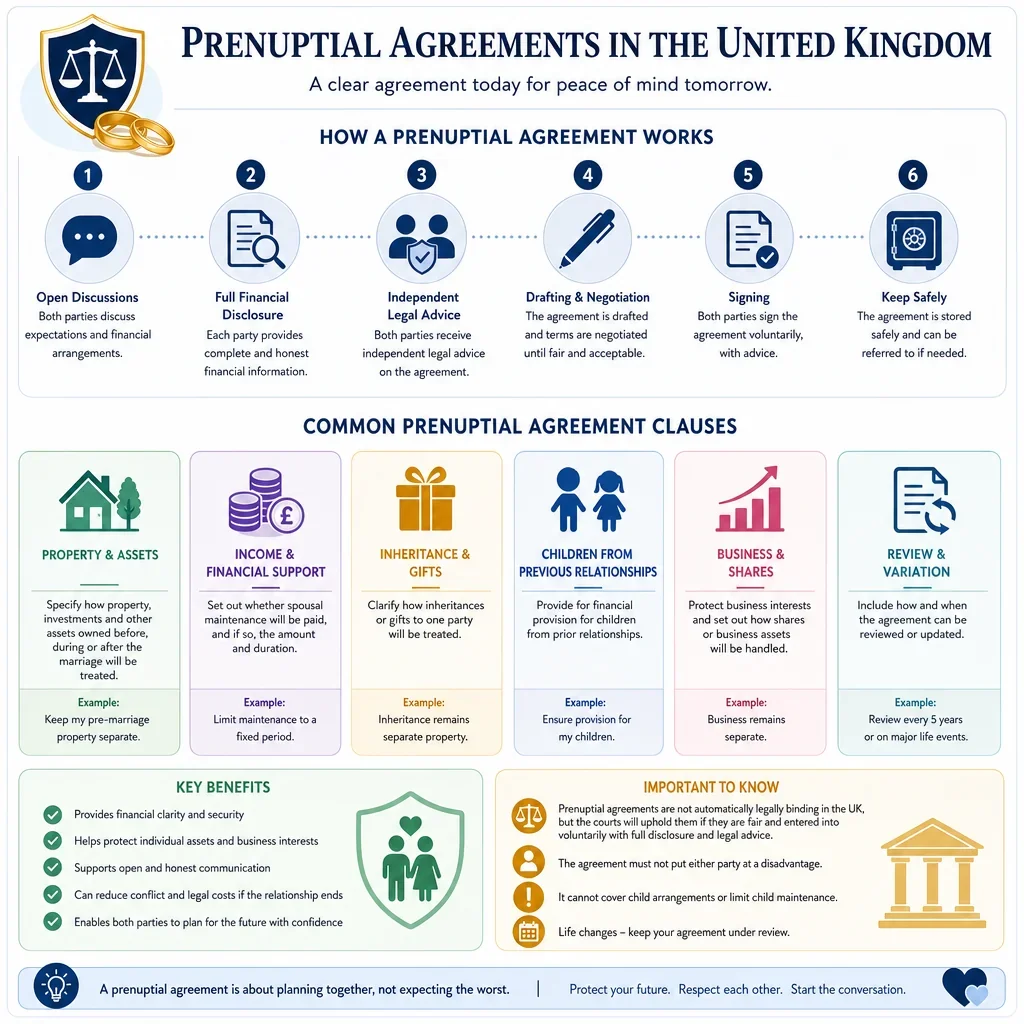

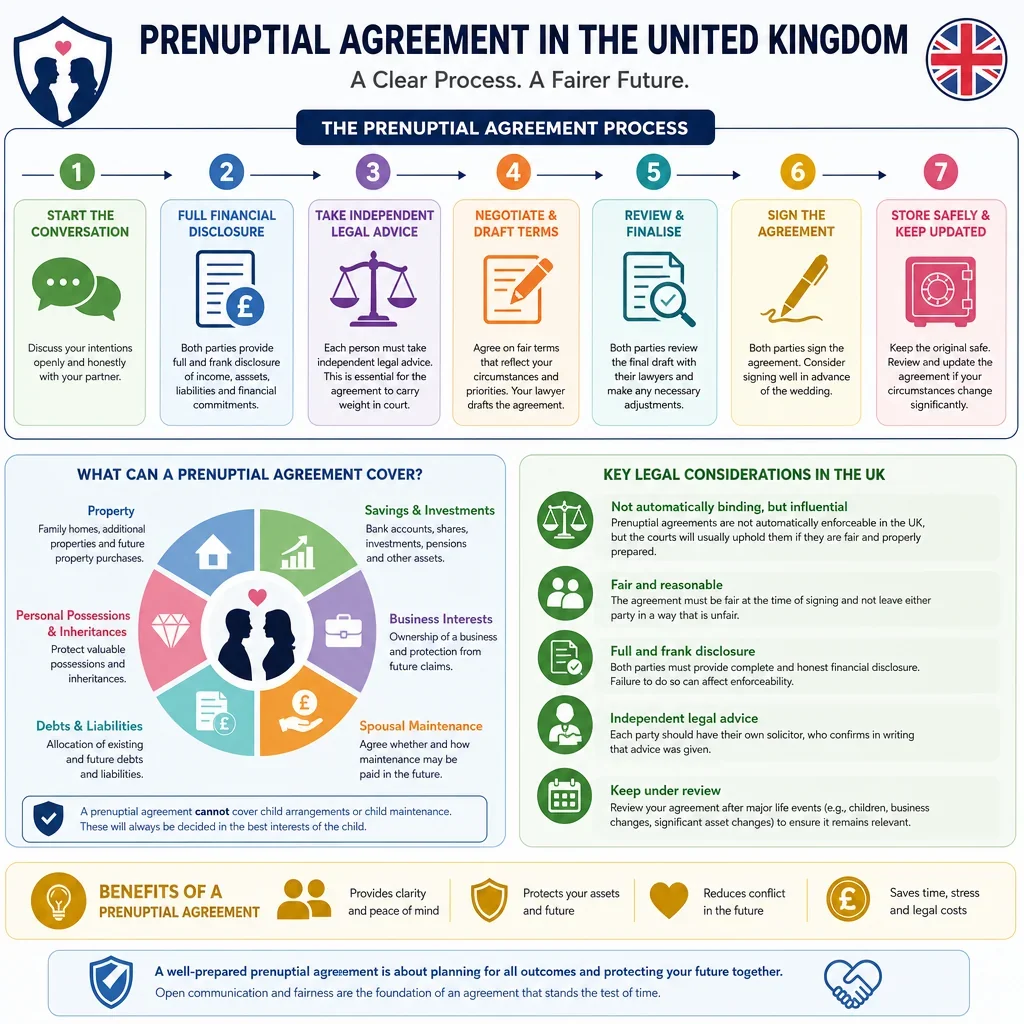

What Financial Disclosure Is Usually Needed For A UK Prenuptial Agreement?

For a UK prenuptial agreement, disclosure should normally cover the full financial picture: property, bank accounts, investments, pensions, business interests, valuable possessions, income, debts and any significant expected inheritance. The most important records are usually those with high value, uncertain value, joint ownership, tax consequences or future income potential.

Why Are Pensions And Business Interests Especially Important?

Pensions can be one of the largest matrimonial assets and should be evidenced with up-to-date pension statements, transfer values or scheme information. Business interests often need extra care because company accounts, shareholder rights, director loans and goodwill may not be obvious from a simple balance sheet.

What Evidence Should Each Person Collect Before Signing?

- Recent statements for bank accounts, savings, investments, pensions, mortgages, loans and credit cards.

- Official documents for land, companies and regulated financial products, such as Land Registry title registers, Companies House filings and pension provider statements.

- Professional valuations where values are material or disputed, especially for property, businesses, private shares, art, jewellery and overseas assets.

- Clear notes of liabilities, guarantees, tax debts and contingent obligations, because these can materially affect net wealth.

How Can Poor Disclosure Affect A Prenuptial Agreement?

In England and Wales, a prenuptial agreement is not automatically binding, but the court may give it weight if it is fair and both parties entered into it with a proper understanding of the financial implications. Incomplete disclosure of major assets, debts or income can therefore weaken reliance on the agreement, especially where it affects needs, fairness or informed consent.

FAQs

You Might Also Be Interested In