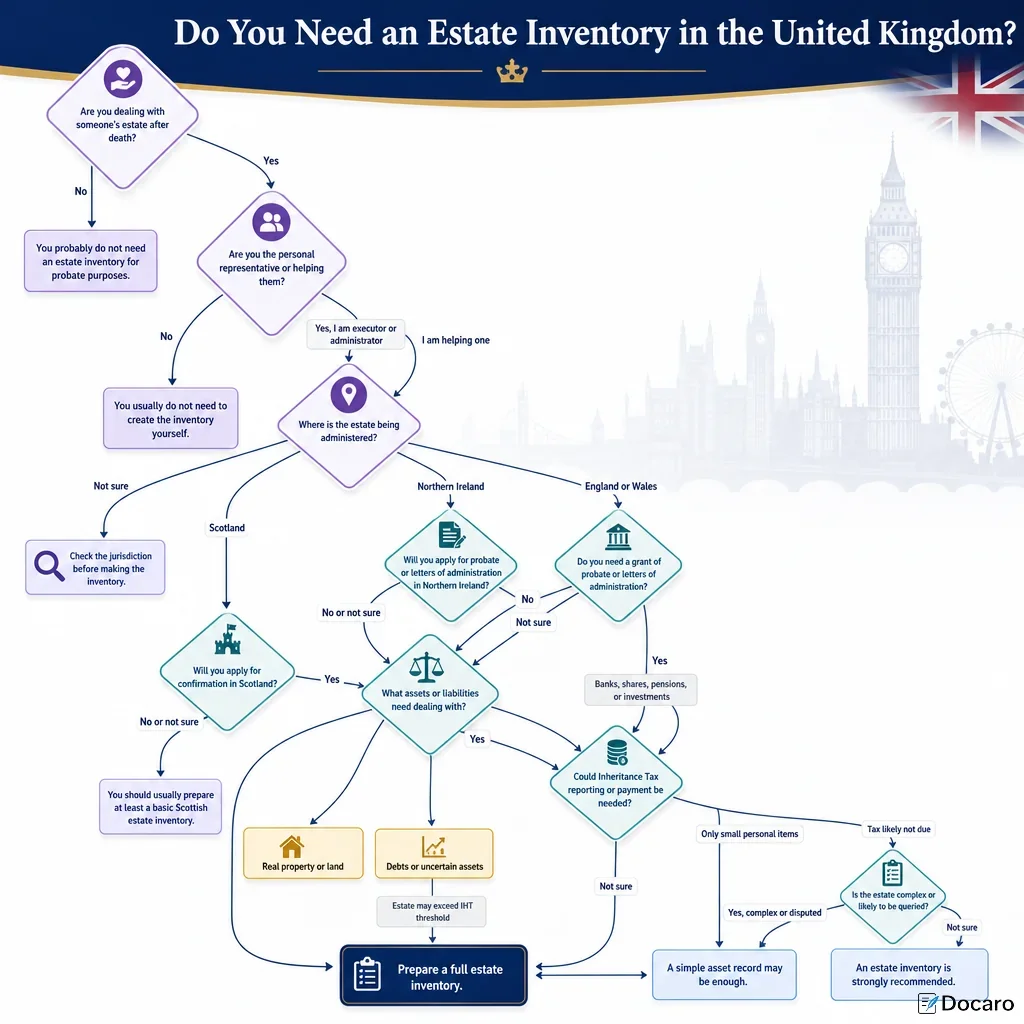

Do You Need An Estate Inventory In The United Kingdom?

Are you dealing with someone\'s estate after death?

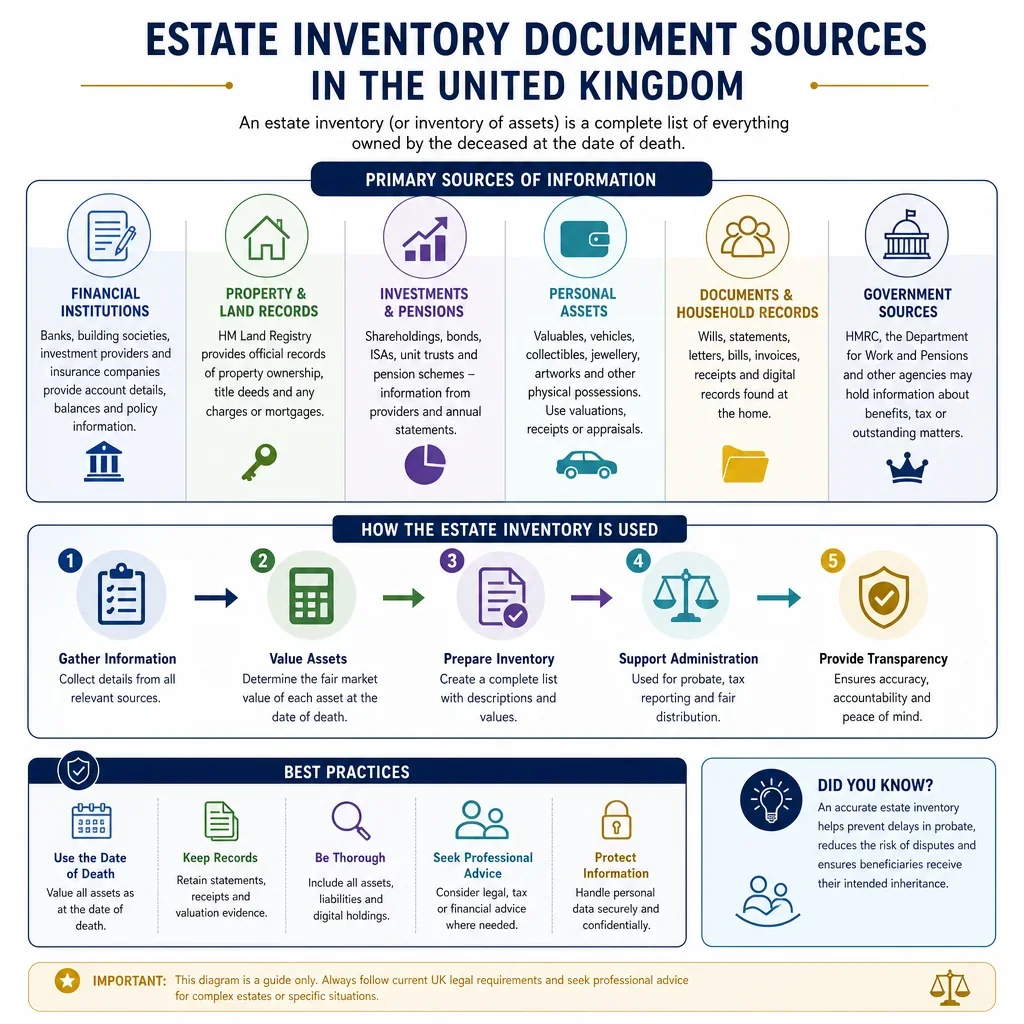

Why Is An Estate Inventory Important In The UK?

An estate inventory helps executors and administrators identify what the deceased owned and owed at the date of death. In the United Kingdom, this can affect probate, confirmation in Scotland, Inheritance Tax, creditor payments, and the final distribution to beneficiaries.

When Can The Wrong Decision Cause Problems?

If an inventory is missed or incomplete, the personal representative may use incorrect estate values, overlook debts, pay beneficiaries too early, or submit inaccurate tax information. This can lead to delays, HMRC queries, disputes between beneficiaries, and potential personal liability for the executor or administrator.

How Does An Inventory Support Probate And Tax?

For many estates, probate or confirmation requires a clear statement of assets and values. HMRC guidance on valuing an estate explains why date-of-death values matter for Inheritance Tax. A well-prepared inventory also helps show how figures were reached if a bank, court, beneficiary, or HMRC asks for evidence.

What Should A UK Estate Inventory Usually Cover?

- Assets: property, bank accounts, investments, vehicles, personal possessions, business interests, and foreign assets.

- Liabilities: mortgages, loans, credit cards, funeral costs, household bills, and tax debts.

- Evidence: statements, valuations, correspondence, title information, and notes on ownership.

- Beneficiary Records: figures used to prepare estate accounts and explain distributions.

Making the right decision early helps keep the estate administration accurate, transparent, and easier to justify if questions arise.

FAQs

You Might Also Be Interested In