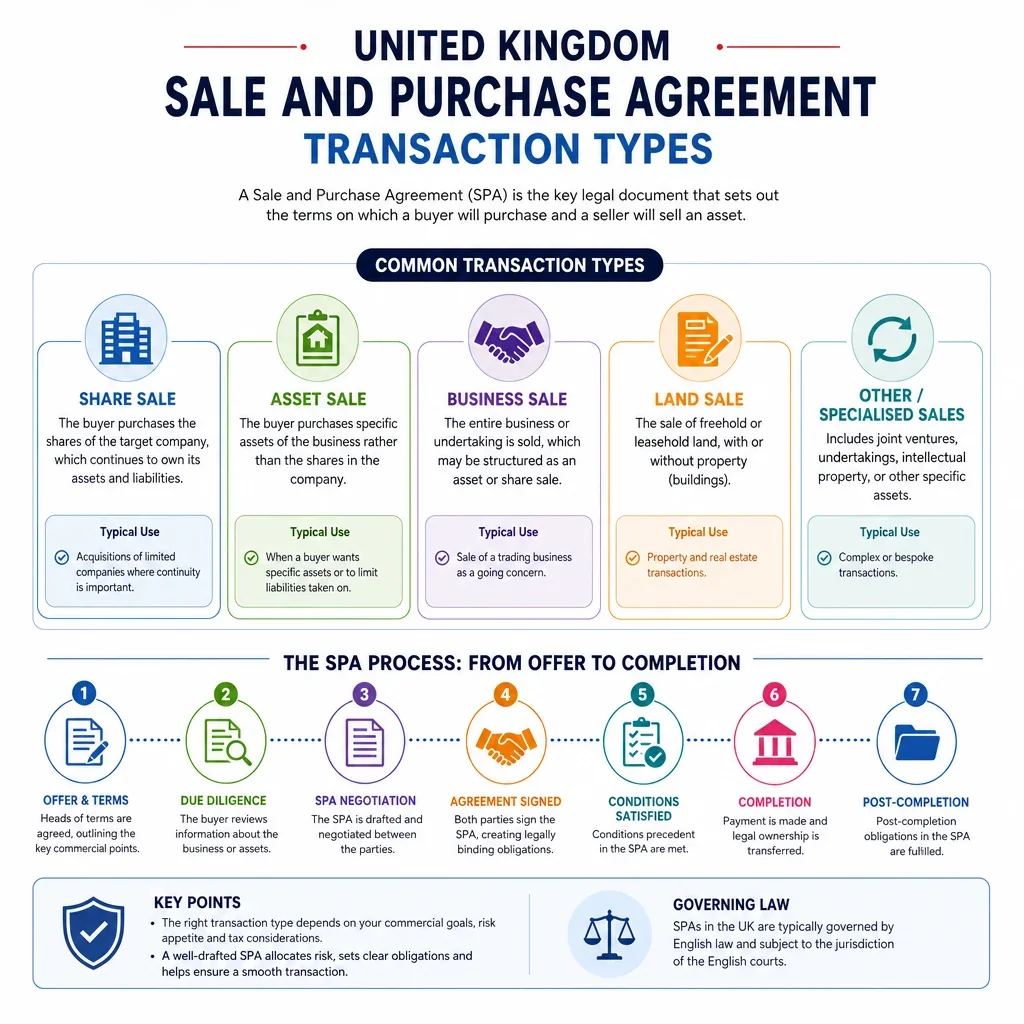

Key Commercial Terms For Sale And Purchase Agreements In The United Kingdom

Commercial Term | Importance | Information Required | Inclusion Frequency | Examples |

|---|---|---|---|---|

Price | ||||

Purchase price | Sets the core economic bargain and valuation basis. | Agreed valuation, currency, VAT position, asset or share basis. | Usually essential | Fixed price of £1,000,000 for all shares price allocated across assets. |

Price allocation | Supports tax, accounting and asset transfer treatment. | Asset values, goodwill value, stock value, plant value, tax advice. | Often included | £300,000 goodwill, £150,000 stock, £50,000 equipment. |

Completion accounts adjustment | Adjusts price after completion by reference to actual financial position. | Accounting policies, target working capital, debt, cash, timetable, dispute process. | Depends on transaction | Price increased for excess cash and reduced for debt or working capital shortfall. |

Locked box mechanism | Fixes price using historic accounts and shifts economic risk from the locked box date. | Locked box accounts, leakage rules, permitted leakage, interest or value accrual. | Depends on transaction | Price fixed at £5,000,000 based on accounts dated 31 March, with no leakage. |

Price, Liability | ||||

Leakage covenant | Prevents value extraction by the seller after the locked box date. | Related party payments, dividends, fees, debt releases, permitted leakage list. | Depends on transaction | Seller repays any dividend, management fee or connected-party payment not permitted. |

Price, Payment, Post-completion | ||||

Earn-out | Defers part of price based on future performance, but creates dispute risk. | Metric, period, accounting rules, management controls, payment cap, audit rights. | Depends on transaction | Additional £500,000 if EBITDA exceeds £1,200,000 in the next financial year. |

Price, Payment | ||||

Deferred consideration | Spreads payment over time and creates seller credit risk. | Payment dates, amount, interest, security, default events, set-off rights. | Often included | £200,000 payable six months after completion, subject to warranty claim set-off. |

Price, Payment, Liability | ||||

Retention | Gives buyer short-term security for claims or adjustment payments. | Retained amount, release date, claims process, interest, escrow or buyer holding. | Often included | 10% retained for 12 months to cover warranty or completion accounts claims. |

Payment, Liability | ||||

Escrow arrangement | Holds funds independently until release conditions are satisfied. | Escrow agent, account details, release triggers, dispute rules, costs. | Depends on transaction | £250,000 held by solicitors pending final tax clearance or claim period expiry. |

Payment | ||||

Deposit | Shows commitment and may compensate seller if buyer fails to complete. | Deposit amount, stakeholder status, forfeiture events, completion credit treatment. | Depends on transaction | 5% deposit paid on exchange and credited against completion payment. |

Payment method | Avoids completion disputes over cleared funds and bank transfer logistics. | Bank details, payment timing, currency, CHAPS or Faster Payments limits. | Usually essential | Completion funds paid by CHAPS to the seller solicitor client account. |

Price, Payment | ||||

Currency and exchange risk | Allocates FX risk where assets, accounts or parties use different currencies. | Payment currency, conversion date, exchange rate source, hedging arrangements. | Depends on transaction | Dollar accounts converted to sterling using Bank of England spot rate on completion. |

VAT treatment | Determines whether VAT is added, included, recoverable or outside scope. | VAT registration, asset type, TOGC status, property option to tax, invoices. | Often included | Price stated exclusive of VAT business sale treated as transfer of a going concern. |

Payment, Assets or shares | ||||

Stamp duty on share transfer | UK share transfers may require stamp duty before registration. | Consideration, stock transfer form, company details, exemptions or reliefs. | Often included | Buyer pays 0.5% stamp duty on UK company shares above the threshold. |

SDLT responsibility | Allocates filing and payment responsibility for land interests in England and Northern Ireland. | Property location, consideration, lease details, reliefs, filing deadline. | Depends on transaction | Buyer files SDLT return and pays SDLT for transferred freehold premises. |

Payment, Liability | ||||

Late payment interest | Encourages prompt payment and compensates delay. | Interest rate, accrual date, compounding, default payment events. | Often included | Interest at 4% above base rate on unpaid deferred consideration. |

Assets or shares | ||||

Shares being sold | Identifies legal title transferred and ensures buyer obtains intended control. | Share class, number, nominal value, certificate numbers, shareholder register. | Usually essential | 100 ordinary shares of £1 each, representing 100% of issued share capital. |

Assets or shares, Liability | ||||

Title to shares warranty | Confirms seller owns the shares free from encumbrances. | Register of members, share certificates, charges, options, pre-emption rights. | Usually essential | Seller warrants full legal and beneficial ownership of the sale shares. |

Assets or shares, Timing | ||||

Stock transfer form | Provides the instrument used to transfer certificated shares. | Transferor, transferee, share details, consideration, certificate, execution date. | Usually essential | Executed stock transfer form delivered at completion for stamping if required. |

Assets or shares | ||||

Assets being sold | Defines exactly what property, rights and business items transfer. | Asset schedule, location, ownership evidence, exclusions, encumbrances. | Usually essential | Goodwill, stock, equipment, domain names, customer contracts and business records. |

Excluded assets | Prevents accidental transfer of assets the seller intends to retain. | Retained cash, receivables, personal items, excluded contracts, retained IP. | Often included | Seller retains cash at bank, tax refunds and pre-completion debtor balances. |

Assets or shares, Price | ||||

Stock and inventory | Controls valuation, risk and treatment of obsolete or slow-moving stock. | Stock count, valuation method, obsolete stock policy, location, title evidence. | Depends on transaction | Stock valued at lower of cost and net realisable value at completion. |

Assets or shares | ||||

Plant and equipment | Identifies movable assets and whether they are owned, leased or financed. | Asset register, finance agreements, serial numbers, condition, maintenance records. | Depends on transaction | Forklifts, production machinery, laptops and vehicles listed in a schedule. |

Intellectual property transfer | Ensures brands, software, copyright and other IP needed for the business transfer. | IP schedule, registrations, licences, creators, assignments, renewal dates. | Depends on transaction | Assignment of trade marks, website content, source code and domain names. |

Assets or shares, Post-completion | ||||

Domain names and digital accounts | Protects business continuity where online presence is central to value. | Domain registrar, account logins, hosting, social accounts, transfer procedures. | Depends on transaction | Transfer .co.uk domain and give access to hosting, analytics and marketplace accounts. |

Assets or shares, Conditions | ||||

Customer and supplier contracts | Determines whether key trading relationships transfer or need consent. | Contract list, assignment clauses, change of control clauses, consent requirements. | Often included | Key supplier contract assigned only after written consent from the supplier. |

Property interests | Confirms premises used by the business can be transferred or occupied. | Title number, leases, licences, landlord consent, searches, charges, SDLT position. | Depends on transaction | Assignment of lease conditional on landlord licence to assign. |

Assets or shares, Liability | ||||

Assumed liabilities | States which debts or obligations the buyer takes on in an asset sale. | Creditors, contract liabilities, employee liabilities, tax, disputes, accruals. | Often included | Buyer assumes post-completion performance obligations but not pre-completion debts. |

Excluded liabilities | Keeps historic or unwanted liabilities with the seller in an asset sale. | Historic claims, tax liabilities, environmental issues, employee arrears, litigation. | Often included | Seller remains liable for pre-completion tax, fines and unpaid trade creditors. |

Assets or shares, Liability, Post-completion | ||||

Employee transfer and TUPE | May automatically transfer employees and associated liabilities on a business sale. | Employee list, terms, claims, consultation, measures, pensions, employee liability information. | Depends on transaction | Employees assigned to the business transfer to buyer on existing terms under TUPE. |

Liability, Post-completion | ||||

Pension liabilities | Allocates auto-enrolment, occupational pension and historic pension risk. | Schemes, contributions, deficits, auto-enrolment status, employee participation. | Depends on transaction | Seller indemnifies pre-completion pension contribution arrears. |

Assets or shares, Liability, Post-completion | ||||

Data protection and personal data transfer | Controls lawful sharing or transfer of customer, employee and supplier personal data. | Data categories, lawful basis, privacy notices, processor contracts, breach history. | Often included | Seller provides customer database only where UK GDPR compliance steps are met. |

Timing | ||||

Completion date | Sets when ownership, payment and operational control pass. | Target date, funding readiness, consents, completion deliverables, cut-off time. | Usually essential | Completion occurs at 11:00 am on the fifth business day after conditions are satisfied. |

Timing, Conditions | ||||

Signing and completion split | Allows agreement before required approvals, funding or consents are obtained. | Longstop date, interim covenants, conditions, termination rights, risk allocation. | Depends on transaction | Agreement signed today completion occurs after FCA consent and landlord approval. |

Longstop date | Allows parties to walk away if completion conditions remain unsatisfied too long. | Condition timetable, approval deadlines, extension rights, termination notice process. | Often included | Either party may terminate if completion has not occurred by 30 September. |

Timing, Assets or shares | ||||

Completion deliverables | Lists documents, approvals and actions needed to complete properly. | Board minutes, transfers, certificates, resignations, releases, keys, passwords. | Usually essential | Deliver share certificates, stock transfer forms, board approvals and director resignations. |

Timing | ||||

Execution method | Ensures the agreement and transfer documents are validly signed. | Signatories, authority, witnessing needs, deeds, electronic platform, counterparts. | Often included | Agreement executed in counterparts using electronic signatures, with deeds witnessed physically. |

Timing, Assets or shares, Liability | ||||

Risk and title transfer | Determines when economic risk and ownership pass to the buyer. | Asset type, insurance, delivery point, possession, title documents, Incoterms if relevant. | Usually essential | Title and risk in assets pass on receipt of completion payment. |

Timing, Conditions, Liability | ||||

Interim business conduct covenants | Preserves business value between signing and completion. | Permitted actions, consent thresholds, ordinary course rules, emergency exceptions. | Often included | Seller must not incur debt, dispose of assets or change employee terms without consent. |

Liability | ||||

Seller warranties | Gives buyer contractual remedies if stated facts about the business are untrue. | Due diligence findings, disclosure letter, accounts, contracts, assets, employees, disputes. | Usually essential | Warranties on accounts, tax, title, contracts, litigation, employees and compliance. |

Buyer warranties | Confirms buyer capacity, authority and ability to complete payment. | Buyer constitution, approvals, funding, solvency, regulatory status. | Often included | Buyer warrants it has power, authority and funds to complete the acquisition. |

Disclosure against warranties | Limits warranty claims by qualifying warranties with known disclosed matters. | Disclosure letter, data room index, specific disclosures, general disclosures. | Usually essential | Warranty on litigation qualified by disclosed employment tribunal claim. |

Specific indemnities | Allocates identified risks pound-for-pound rather than relying on warranty damages. | Known issue, estimated exposure, claim control, mitigation, cap, duration. | Often included | Seller indemnifies buyer for disclosed tax enquiry or environmental clean-up claim. |

Tax covenant | Allocates historic tax liabilities to seller in a share sale. | Tax returns, HMRC enquiries, losses, reliefs, pre-completion tax, group tax issues. | Often included | Seller pays buyer for corporation tax arising from pre-completion profits. |

Liability cap | Limits seller exposure for warranty, indemnity or covenant claims. | Cap amount, claim types, exclusions, fraud carve-out, insured risks. | Usually essential | Warranty liability capped at 30% of price title and tax claims capped at price. |

De minimis claim threshold | Prevents small claims from being brought individually. | Minimum claim amount, aggregation rules, excluded claim types. | Often included | No warranty claim unless individual loss exceeds £5,000. |

Basket threshold | Requires aggregate losses to exceed an agreed threshold before claims proceed. | Threshold amount, tipping or deductible basis, included claim types. | Often included | Buyer may claim only when aggregate warranty losses exceed £50,000. |

Liability, Timing | ||||

Warranty claim time limits | Sets deadline for notifying claims and gives seller finality. | Notice deadline, claim issue deadline, tax claim period, fraud exceptions. | Usually essential | General warranty claims notified within 18 months tax claims within seven years. |

Claim notice procedure | Specifies how claims must be notified and progressed. | Notice address, required details, service method, follow-up proceedings deadline. | Often included | Buyer must give written notice stating grounds and estimated loss before deadline. |

Liability | ||||

Mitigation and third-party recovery | Prevents double recovery and requires reasonable loss management. | Insurance, third-party claims, tax reliefs, recovery sharing, conduct rights. | Often included | Warranty damages reduced by insurance proceeds actually recovered by buyer. |

Fraud carve-out | Preserves remedies where a party acts dishonestly or conceals information. | Carve-out wording, affected limitations, knowledge attribution, disclosure process. | Usually essential | Liability caps do not apply to fraud or fraudulent misrepresentation. |

Non-reliance clause | Seeks to limit claims based on pre-contract statements outside the SPA. | Pre-contract statements, information memorandum, data room, fraud carve-out. | Often included | Buyer confirms it has not relied on statements except express warranties. |

Reasonableness of liability limits | Some exclusions and limitations must satisfy statutory reasonableness requirements. | Bargaining strength, insurance, price, risk allocation, negotiated status. | Depends on transaction | Exclusion for misrepresentation assessed against reasonableness under UCTA and Misrepresentation Act. |

Conditions, Timing | ||||

Conditions precedent | Makes completion conditional on key approvals or events. | Required consents, responsible party, satisfaction evidence, waiver rights, deadline. | Depends on transaction | Completion conditional on landlord consent, bank release and regulatory approval. |

Conditions | ||||

Regulatory approval | Certain regulated businesses need approval before control changes. | Regulated permissions, controller details, notification forms, approval timetable. | Depends on transaction | Completion conditional on FCA approval for change in control. |

Competition and merger clearance | Large transactions may require CMA assessment or create hold-separate risk. | Turnover, share of supply, markets, competitors, transaction structure, filing strategy. | Depends on transaction | Completion conditional on CMA clearance or expiry of review period. |

National Security and Investment approval | Mandatory notification may apply to acquisitions in sensitive UK sectors. | Sector, target activities, control level, buyer identity, notification analysis. | Depends on transaction | Completion conditional on NSIA clearance for acquisition of qualifying defence supplier. |

Conditions, Assets or shares | ||||

Third-party consents | Avoids breach or loss of key rights on assignment or change of control. | Consent list, counterparties, contract clauses, landlord, lenders, licensors. | Often included | Landlord, bank and software licensor consents required before completion. |

Conditions, Payment | ||||

Buyer financing condition | Allocates risk that buyer funding is not available at completion. | Funding sources, lender conditions, commitment letters, equity funding, fallback rights. | Depends on transaction | Completion conditional on lender drawdown, or buyer has no financing condition. |

Conditions, Timing | ||||

Corporate approvals | Confirms parties have authority to sell, buy and execute documents. | Articles, shareholder agreements, board minutes, shareholder resolutions, authority limits. | Often included | Seller board approves asset sale buyer board approves acquisition and funding. |

Conditions, Assets or shares, Post-completion | ||||

Release of security | Ensures assets or shares are transferred free from charges or lender restrictions. | Charges register, lender payoff amount, deed of release, Companies House filings. | Often included | Bank releases debenture on completion after repayment from sale proceeds. |

Conditions, Liability | ||||

Material adverse change condition | May allow buyer to refuse completion if business materially deteriorates. | Trigger events, exclusions, financial thresholds, notice process, dispute method. | Optional | Buyer may terminate if key licence is revoked before completion. |

Conditions, Assets or shares, Timing | ||||

Pre-completion restructuring | Ensures target group or assets are in the agreed perimeter before sale. | Group structure, intra-group assets, tax steps, consents, transfer documents. | Depends on transaction | Seller transfers excluded property out of target before share completion. |

Post-completion, Liability | ||||

Non-compete and non-solicitation covenants | Protects goodwill bought by buyer, but must be reasonable to be enforceable. | Restricted activities, territory, duration, customers, employees, seller role. | Often included | Seller must not compete in the UK for two years or solicit key customers. |

Post-completion | ||||

Transition services | Maintains operations while buyer separates systems, staff or premises. | Services, duration, charges, service levels, data access, termination rights. | Depends on transaction | Seller provides payroll, IT support and bookkeeping for three months after completion. |

Handover assistance | Helps buyer take operational control without losing knowledge or relationships. | Key contacts, training needs, documents, systems, handover period, fees. | Often included | Seller introduces buyer to top customers and trains staff for 20 hours. |

Books and records access | Supports audits, tax filings, claims and statutory record retention. | Record types, retention period, access rights, confidentiality, copying rights. | Often included | Seller may access pre-completion tax records on reasonable notice for six years. |

Post-completion, Liability | ||||

Confidentiality | Protects deal terms, trade secrets and sensitive business information. | Confidential information scope, permitted disclosures, duration, announcements. | Usually essential | Parties keep SPA terms confidential except for legal, tax or regulatory disclosure. |

Post-completion | ||||

Public announcements | Controls market, employee, customer and press communications about the sale. | Announcement text, timing, approvals, listed company or regulatory obligations. | Often included | No announcement without prior written consent except as required by law. |

Liability, Post-completion | ||||

Insurance arrangements | Ensures assets, historic claims and business risks are covered at handover. | Policies, claims history, run-off cover, insured assets, warranty insurance. | Depends on transaction | Buyer arranges insurance from completion seller maintains run-off cover for claims-made policies. |

Liability | ||||

Warranty and indemnity insurance | Can replace or supplement seller recourse for warranty claims. | Policy terms, insured warranties, exclusions, premium, retention, claims process. | Depends on transaction | Buyer-side W&I policy covers general warranties above an insured retention. |

Post-completion, Assets or shares | ||||

Post-completion filings | Ensures statutory registers and public filings reflect the transaction. | Companies House forms, PSC updates, director changes, share register, charges. | Often included | Update register of members, PSC register and Companies House officer filings. |

Assets or shares, Post-completion | ||||

Director resignations and appointments | Transfers management control of the target company in a share sale. | Outgoing directors, resignation letters, new appointments, indemnities, filings. | Often included | Seller-appointed directors resign at completion and buyer nominees are appointed. |

Post-completion, Assets or shares | ||||

Company or business name change | Prevents confusion and protects retained or transferred goodwill. | Name rights, trade marks, Companies House availability, rebranding timetable. | Depends on transaction | Seller changes retained company name within 10 business days after asset sale. |

Assets or shares, Price, Post-completion | ||||

Debtors and creditors | Determines who receives pre-completion income and pays pre-completion debts. | Aged debtor report, creditor list, collection arrangements, bad debt policy. | Depends on transaction | Seller retains pre-completion debtors buyer collects and remits them after completion. |

Price, Payment, Post-completion | ||||

Apportionments | Splits periodic income and expenses fairly across the completion date. | Rent, rates, utilities, subscriptions, service charges, accruals, prepayments. | Often included | Rent and utilities apportioned at midnight on the completion date. |

Price | ||||

Working capital target | Ensures buyer receives a normal level of operating working capital. | Historic working capital, seasonality, accounting policies, normalised adjustments. | Depends on transaction | Price reduced pound-for-pound if completion working capital is below £750,000. |

Cash-free debt-free basis | Clarifies whether enterprise value is adjusted for cash and debt at completion. | Debt definition, cash definition, intra-group balances, finance leases, overdrafts. | Depends on transaction | Equity price equals enterprise value plus cash minus debt at completion. |

Price, Payment, Conditions | ||||

Intra-group balances | Prevents hidden debt or value leakage within a group before sale. | Intercompany loans, trading balances, releases, repayment mechanics, tax impact. | Depends on transaction | All intercompany loans are repaid or capitalised before completion. |

Liability, Conditions, Post-completion | ||||

Release or replacement of guarantees | Protects seller from continuing liability for obligations after disposal. | Guarantee list, beneficiaries, release requirements, replacement security, timing. | Depends on transaction | Buyer procures release of seller parent guarantee for premises lease. |

Liability, Post-completion | ||||

Dispute resolution | Sets forum and procedure for SPA disputes and expert determinations. | Court or arbitration, expert accountant, escalation steps, governing law. | Usually essential | English courts for legal disputes independent accountant for completion accounts disputes. |

Liability | ||||

Governing law and jurisdiction | Determines legal system and court jurisdiction for interpreting and enforcing the SPA. | Party locations, asset location, enforcement needs, preferred courts. | Usually essential | Agreement governed by English law with exclusive jurisdiction of English courts. |

Timing, Liability | ||||

Notices | Controls valid service of claims, termination notices and completion communications. | Addresses, email use, deemed receipt, service hours, recipient contacts. | Usually essential | Warranty claim notices served by hand, pre-paid post or email to named recipients. |

Payment | ||||

Transaction costs | Allocates legal, accounting, broker and filing costs. | Adviser fees, success fees, filing fees, stamp taxes, target-paid expenses. | Often included | Each party pays its own costs buyer pays stamp duty and registration fees. |

What Commercial Terms Matter Most In A UK Sale And Purchase Agreement?

Price, payment mechanics, assets or shares, timing, liability, conditions and post-completion obligations should be agreed before drafting. In UK transactions, the main risk is often not the headline price but uncertainty over adjustments, completion deliverables, tax responsibility, warranty limits and what happens between signing and completion.

Why Should The Price Mechanism Be Agreed Early?

The dataset shows that UK SPAs commonly need a clear choice between locked box, completion accounts, fixed price or earn-out mechanics. This affects how economic risk transfers, what accounts are needed, whether leakage is prohibited and whether the buyer can adjust the price after completion.

Which Terms Usually Need Specialist Attention?

- Tax covenant, warranties and indemnities are especially important because they allocate historic business risk and usually require negotiation of caps, baskets, time limits and disclosure.

- Share transfers require Companies Act 2006 checks, board approval, stock transfer forms and stamp duty analysis.

- Asset transfers require a detailed asset schedule and may need third-party consent for contracts, property, licences or employees.

- TUPE may apply to business or asset sales involving employees, requiring careful employee information and liability allocation.

What Information Should Be Ready Before Drafting?

Parties should collect the target accounts, asset or share details, contract lists, debt and cash balances, employee information, property documents, IP schedules, consents, tax records and disclosure materials. Missing information commonly delays completion or weakens warranty, indemnity and price adjustment drafting.

FAQs

You Might Also Be Interested In