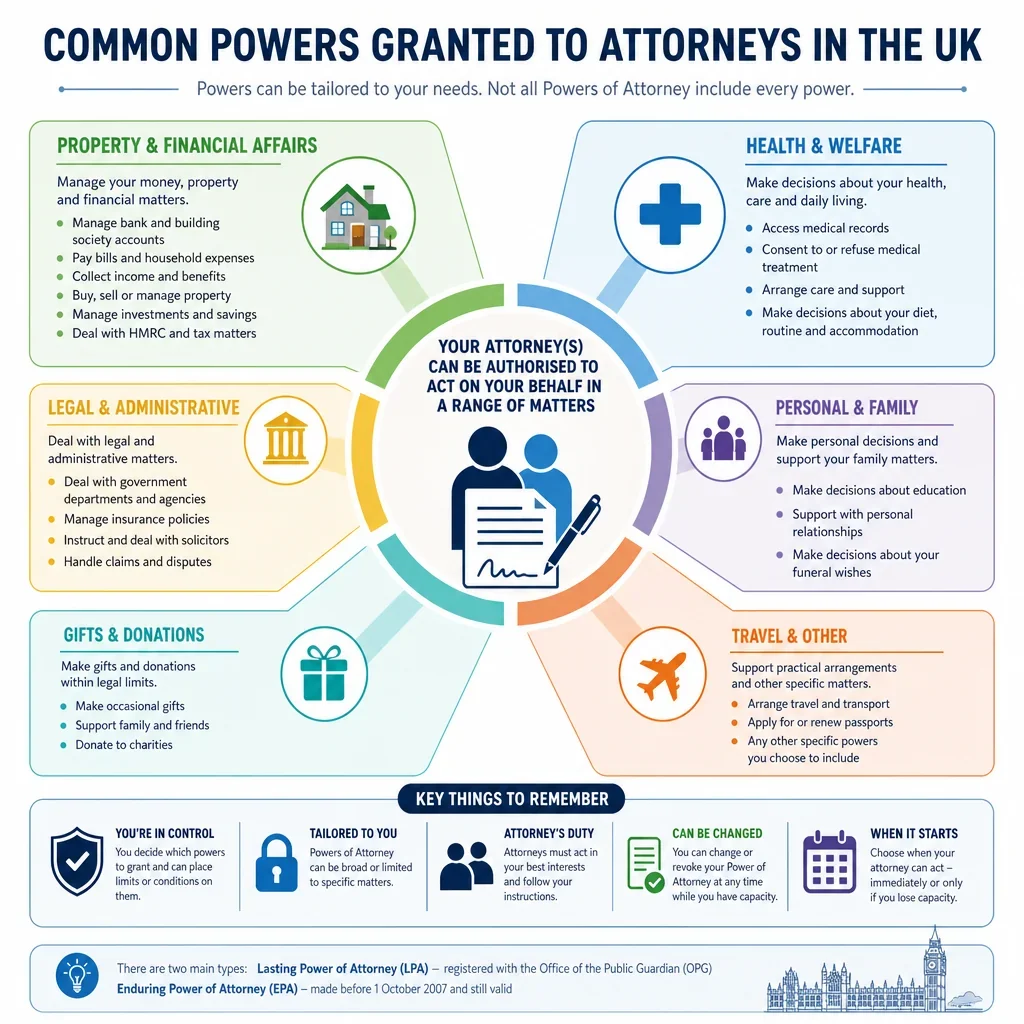

Common Powers Granted To Attorneys In The UK

Created:

Understanding common attorney powers helps you decide what authority to grant and how it may be used. This guide supports anyone exploring an AI Generated British Power of Attorney.

Power Name | Power Scope | Description | Relevant to Financial Documents | Relevant to Welfare Documents | Drafting Notes |

|---|---|---|---|---|---|

Banking and payments | |||||

Operate Bank And Building Society Accounts | General | Open, close and manage current, savings and building society accounts. | true | false | Banks may require certified copies and may restrict access until registration or identification checks are complete. |

Pay Bills And Household Expenses | General | Pay utilities, rent, mortgage, insurance, subscriptions and other regular expenses. | true | false | Can be broad, but unusual or large payments may need records explaining benefit to the donor. |

Set Up Direct Debits And Standing Orders | General | Create, amend or cancel recurring payments from the donoru0027s accounts. | true | false | Useful for care fees, utilities and mortgage payments attorneys should keep clear payment records. |

Withdraw Cash | General | Withdraw cash for the donoru0027s personal spending and day-to-day needs. | true | false | Cash use should be documented because it is harder to evidence than card or bank payments. |

Use Cards And Online Banking | Specific | Use bank cards, telephone banking, mobile apps or online banking where the provider allows it. | true | false | Providers often have their own attorney access rules avoid sharing the donoru0027s passwords if terms prohibit it. |

Receive Income And Money Owed | General | Collect salary, rent, pensions, refunds, compensation and other money due to the donor. | true | false | State if the attorney may redirect income to a managed account in the donoru0027s name. |

Repay Debts And Manage Credit | General | Pay loans, credit cards, overdrafts and other debts owed by the donor. | true | false | Borrowing new money should be dealt with separately and is usually more sensitive. |

Borrow Money Or Arrange Credit | Specific | Apply for loans, overdrafts or credit facilities for the donoru0027s benefit. | true | false | Consider requiring written consent, professional advice or a monetary cap. |

Property transactions | |||||

Buy Property | Specific | Negotiate and complete the purchase of land or buildings for the donor. | true | false | May need clear authority for deposits, mortgage documents, conveyancers and HM Land Registry forms. |

Sell Property | Specific | Market, negotiate and complete the sale of the donoru0027s house, flat or land. | true | false | Often vital for funding care include authority to sign contracts, transfers and Land Registry papers. |

Mortgage Or Remortgage Property | Specific | Grant, vary or repay a mortgage or legal charge over the donoru0027s property. | true | false | Lenders may require express wording and independent legal advice. |

Let Or Manage Rental Property | General | Find tenants, sign tenancies, collect rent and deal with repairs or agents. | true | false | Include authority for tenancy deposits, licences, safety checks and property management agents. |

Maintain And Insure Property | General | Arrange repairs, services, security, utilities and buildings or contents insurance. | true | false | Useful where the donor enters care but keeps an empty home. |

Arrange A Move Or Downsizing | Conditional | Organise moving, storage, sale of contents and related payments. | true | true | Financial powers cover payments welfare powers may cover where the donor lives. |

Tax and benefits | |||||

Deal With HMRC | General | File tax returns, deal with PAYE, claim repayments and communicate with HMRC. | true | false | HMRC may need separate agent authorisation or proof of attorney authority. |

Prepare And Submit Tax Returns | Specific | Complete, sign and submit Self Assessment or other tax returns for the donor. | true | false | Consider authority to appoint accountants and approve electronic filing. |

Claim And Manage Benefits | General | Claim, renew and manage state benefits, allowances and related payments. | true | false | DWP appointeeship may still be relevant for benefits administration. |

Deal With Care Funding Assessments | Specific | Provide financial information and respond to local authority care funding assessments. | true | true | Financial disclosure is financial needs and care planning decisions are welfare-related. |

Investments and pensions | |||||

Manage Investments | General | Buy, sell and manage shares, funds, bonds and investment accounts. | true | false | Include authority to use regulated advisers and discretionary investment managers if intended. |

Appoint A Discretionary Investment Manager | Specific | Allow a regulated manager to make investment decisions for the donoru0027s portfolio. | true | false | Often needs express wording because it delegates investment decisions to a third party. |

Manage Pensions | General | Communicate with pension providers, receive payments and manage pension choices. | true | false | Pension transfers, drawdown or beneficiary nominations may need specific advice and provider forms. |

Take Pension Drawdown Decisions | Specific | Choose pension withdrawals, annuity options or income drawdown for the donor. | true | false | High-risk decisions should usually require regulated financial advice. |

Manage Insurance Policies | General | Arrange, renew, claim on or cancel insurance for the donoru0027s assets and needs. | true | false | Life policies, investment bonds and beneficiary choices may need specific wording. |

Business operations | |||||

Run A Sole Trader Business | Specific | Operate the donoru0027s sole trader business, pay suppliers and collect income. | true | false | State limits on contracts, borrowing, employees, stock and sale or closure of the business. |

Exercise Shareholder Rights | Specific | Vote shares, receive dividends and sign shareholder documents for the donor. | true | false | Company articles and shareholdersu0027 agreements may restrict attorney action. |

Act In Relation To A Directorship | Conditional | Handle practical company matters linked to the donoru0027s role as director where lawful. | true | false | An attorney cannot automatically perform personal director duties check articles, board approval and company law advice. |

Employ And Pay Staff | Specific | Hire, manage and pay carers, domestic staff or business employees. | true | true | Include PAYE, pensions, insurance and employment compliance where the donor is an employer. |

Health and care decisions | |||||

Make Medical Treatment Decisions | General | Make decisions about healthcare, treatment and medical appointments if the donor lacks capacity. | false | true | Requires a health and welfare LPA and normally only applies when the donor lacks capacity for the decision. |

Decide About Life-Sustaining Treatment | Specific | Give or refuse consent to life-sustaining treatment decisions if authorised. | false | true | The LPA form requires a specific choice otherwise the attorney may not have this authority. |

Agree Care And Support Plans | General | Discuss and agree care arrangements with social services or care providers. | false | true | Funding payments may need a separate property and financial affairs LPA. |

Personal welfare | |||||

Decide Where The Donor Lives | General | Decide whether the donor lives at home, with family, or in a care home. | false | true | A financial attorney may pay for accommodation but cannot make welfare residence decisions without welfare authority. |

Decide Daily Routine And Personal Care | General | Make decisions about washing, dressing, diet, activities and daily support. | false | true | Preferences can guide attorneys without making impractical binding instructions. |

Health and care decisions | |||||

Access Health And Care Records | Specific | Request and view relevant medical, care and social services records. | false | true | Providers may require proof of welfare authority and data protection checks. |

Make Complaints About Health Or Care | Specific | Raise complaints or concerns with the NHS, care providers or local authorities. | false | true | May sit alongside authority to access records and speak to professionals. |

Legal and administrative matters | |||||

Deal With Government Departments | General | Communicate with DWP, HMRC, DVLA, local authorities and other public bodies. | true | true | Some bodies use separate identity, consent or appointee processes. |

Appoint Professional Advisers | General | Instruct solicitors, accountants, financial advisers, surveyors and agents. | true | true | State if professional fees can be paid from the donoru0027s funds. |

Conduct Legal Claims Or Proceedings | Specific | Start, defend, settle or compromise legal claims for the donor. | true | true | Litigation may require solicitor involvement and separate court rules on capacity and litigation friends. |

Sign Contracts And Forms | General | Sign forms, contracts, notices and routine documents on the donoru0027s behalf. | true | true | Deeds, property transfers and regulated transactions may require specific signing formalities. |

Manage Digital Accounts And Communications | Specific | Access or manage email, online accounts and digital services where permitted. | true | true | Terms of service and data protection rules may limit access list important accounts where appropriate. |

Make Limited Gifts | Conditional | Make customary gifts on occasions or to charities within statutory limits. | true | false | Larger gifts, tax planning gifts or estate planning gifts usually need Court of Protection approval. |

Banking and payments | |||||

Make Loans To Others | Conditional | Lend the donoru0027s money to family members or others if clearly authorised. | true | false | Should normally require written terms, security, affordability and no conflict of interest. |

Legal and administrative matters | |||||

Act As Trustee Or Deal With Trust Property | Conditional | Carry out trust-related acts only where the law and trust terms allow it. | true | false | Ordinary attorney authority may not cover trustee duties separate trustee delegation may be needed. |

Work With Replacement Attorneys | Conditional | Allow replacement attorneys to step in if an original attorney can no longer act. | true | true | The LPA should state when replacements act and whether attorneys act jointly, jointly and severally, or jointly for some matters. |

Exclude Self-Dealing Transactions | Excluded | Prevent attorneys from buying donor assets, taking benefits or acting in conflicts without approval. | true | true | Useful where an attorney may also be a beneficiary, tenant, business partner or buyer. |

Make Best Interests Decisions | General | Decide for the donor by applying the statutory best interests checklist where capacity is lacking. | true | true | Instructions cannot override the Mental Capacity Act best interests framework. |

Act Only After Loss Of Capacity | Conditional | Limit attorney action until the donor lacks capacity for the relevant decision. | true | true | Financial LPAs can sometimes be used with consent while the donor has capacity welfare LPAs are normally capacity-dependent. |

Apply To The Court Of Protection | Specific | Ask the Court of Protection for directions, approval or authority where needed. | true | true | Important for disputed decisions, major gifts, serious welfare issues or uncertain attorney powers. |

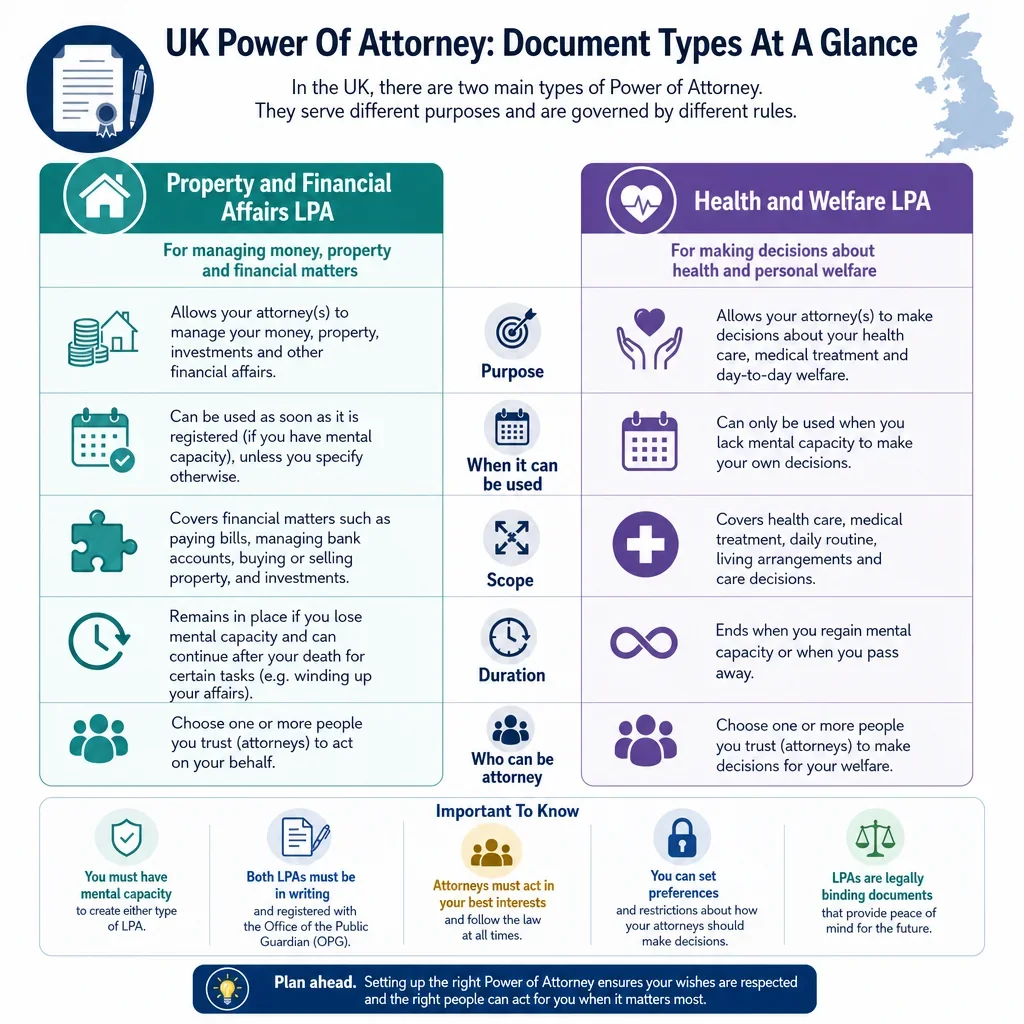

What Powers Should A UK Power Of Attorney Include?

A property and financial affairs power of attorney usually needs broad powers for everyday money management, including bank accounts, bills, benefits, tax, property insurance and correspondence. If it may be used for investments, pensions, business assets, gifts, loans, digital access or property sales, those areas should be considered expressly because third parties may ask to see clear wording.

Which Attorney Powers Need Special Care In The UK?

- Gifts are restricted: under the Mental Capacity Act 2005, an attorney under a lasting power of attorney can only make limited gifts unless the Court of Protection authorises more.

- Health and welfare decisions are separate: medical treatment, care, residence and life-sustaining treatment decisions belong in a health and welfare LPA, not a financial document.

- Trustee functions are limited: acting as a trustee or dealing with jointly owned trust property may need separate trustee powers or court authority.

- Some powers should be conditional: instructions often limit powers to when the donor lacks capacity, when a professional advises, or when a transaction exceeds a set value.

Why Do Banks, Care Providers And Land Registry Wording Matter?

In practice, attorneys often have to satisfy banks, HM Land Registry, pension providers, local authorities and care providers. Clear powers and instructions can reduce refusal risk, especially for selling property, managing investments, accessing records, paying care fees, dealing with HMRC or communicating with government departments.

Want to Generate Your own Power of Attorney?

Docaro AI can help you write your own Power of Attorney for use in the United Kingdom in minutes.

FAQs

Common powers include managing bank accounts, paying bills, buying or selling property, handling investments, dealing with tax, and making health or care decisions where legally authorised.

Show All FAQs

You Might Also Be Interested In

Learn about UK Power of Attorney document types, their uses, and how to choose the right form for your needs.

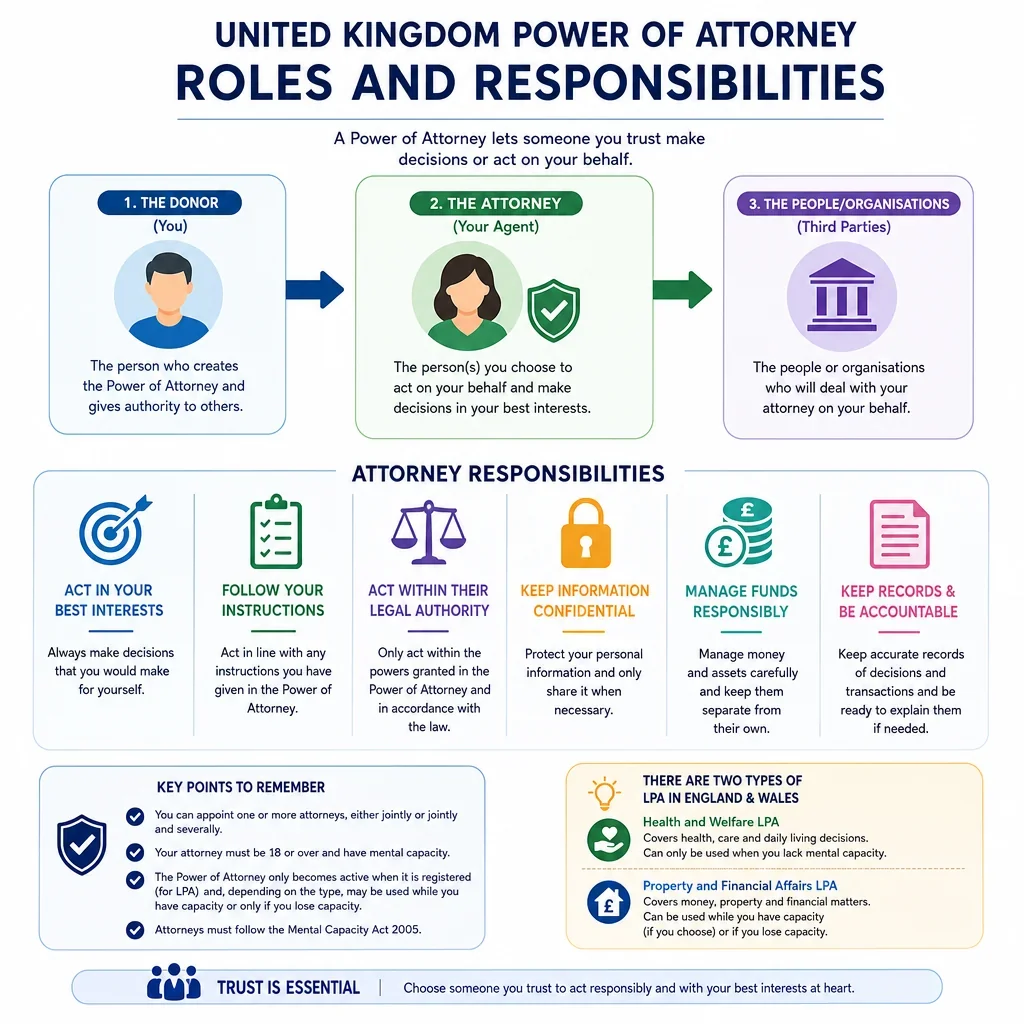

Understand key United Kingdom power of attorney roles, duties and responsibilities, so you can choose and act with confidence.