AI Generated Singaporean Personal Guarantee

PDF & Word - 2026 Updated

Docaro Pricing

When do you need a Personal Guarantee in Singapore?

- Securing Business LoansYou need a personal guarantee when lending money to a business to ensure the owner personally promises to repay if the business cannot.

- Renting Commercial SpaceLandlords often require a personal guarantee for business leases to protect against missed rent payments by the company.

- Supporting Supplier AgreementsSuppliers may ask for a personal guarantee when extending credit to a new or risky business to safeguard their payments.

- Partnering in Joint VenturesIn business partnerships, a personal guarantee helps build trust by having individuals back the venture's obligations.

- Why a Well-Drafted Document MattersA clear and properly written personal guarantee prevents misunderstandings and ensures it holds up in Singapore courts if needed.

Singaporean Legal Rules for a Personal Guarantee

- What It IsA personal guarantee is a promise by an individual to pay back a debt if the main borrower fails to do so.

- Voluntary AgreementYou must enter into a personal guarantee willingly, without any pressure or deception.

- Clear TermsThe guarantee document should spell out exactly what you are agreeing to, including the amount and conditions.

- Full DisclosureThe lender must provide all relevant information about the loan before you sign the guarantee.

- Limits on LiabilityYour responsibility is usually limited to the amount stated in the guarantee, but it can extend to interest and costs.

- When It EndsThe guarantee typically ends when the main debt is fully repaid or if the agreement specifies an end date.

- Legal ProtectionSingapore courts can cancel a guarantee if it was signed under duress, fraud, or if key details were hidden.

- Seek AdviceIt's wise to get independent legal advice before signing to understand the risks involved.

Using the wrong structure for a personal guarantee can expose the guarantor to unlimited liability or invalidate the guarantee entirely.

What a Proper Personal Guarantee Should Include

- Guarantor's IdentityClearly state the full name, address, and contact details of the person providing the guarantee.

- Main Debt DescriptionDescribe the loan or debt being guaranteed, including the amount, purpose, and terms of repayment.

- Guarantee ScopeSpecify what the guarantee covers, such as the full amount or a limited portion of the debt.

- Unconditional PromiseConfirm that the guarantor agrees to pay the debt without needing to be asked first if the main borrower fails.

- Duration of GuaranteeIndicate how long the guarantee lasts, such as until the debt is fully repaid or a set time period.

- Rights WaiverState that the guarantor gives up the right to delay payment if the lender makes changes to the main agreement.

- Governing RulesNote that the guarantee follows Singapore laws and specify which courts handle any disputes.

- Signatures and DatesInclude spaces for the guarantor, borrower, and lender to sign and date the document.

Why Free Templates Can Be Risky for Personal Guarantees

Free templates for personal guarantees often use generic wording that doesn't comply with Singapore's specific legal requirements under the Contracts Act or Insolvency Act. This can lead to unenforceable guarantees, disputes over liability limits, or failure to protect against creditor claims in bankruptcy scenarios.

Our AI generates bespoke personal guarantee documents tailored to your exact circumstances, incorporating Singapore-specific clauses for enforceability, clear liability terms, and robust protections, ensuring a legally sound agreement without the pitfalls of one-size-fits-all templates.

Generate Your Document in 4 Easy Steps

Why Use Our Docaro?

Singapore

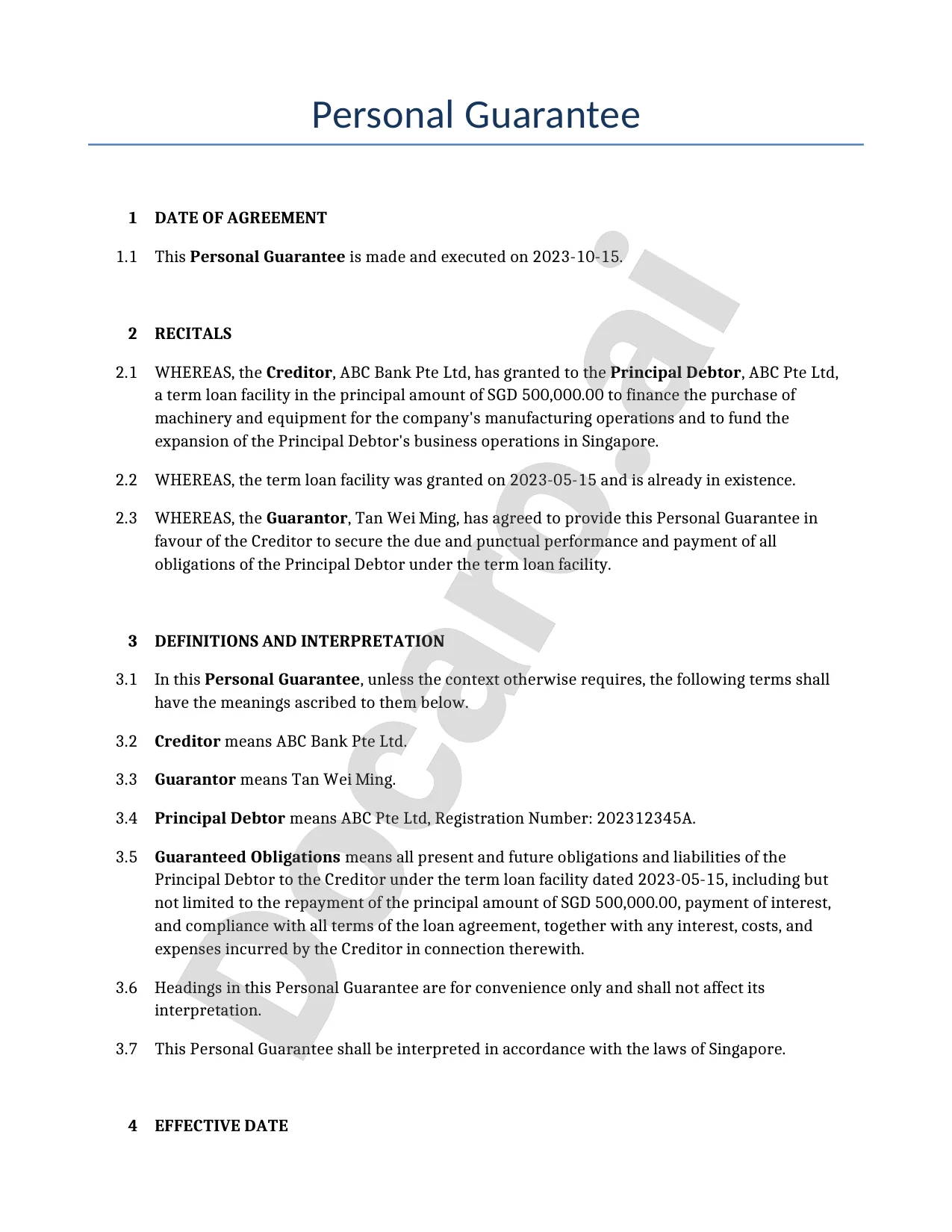

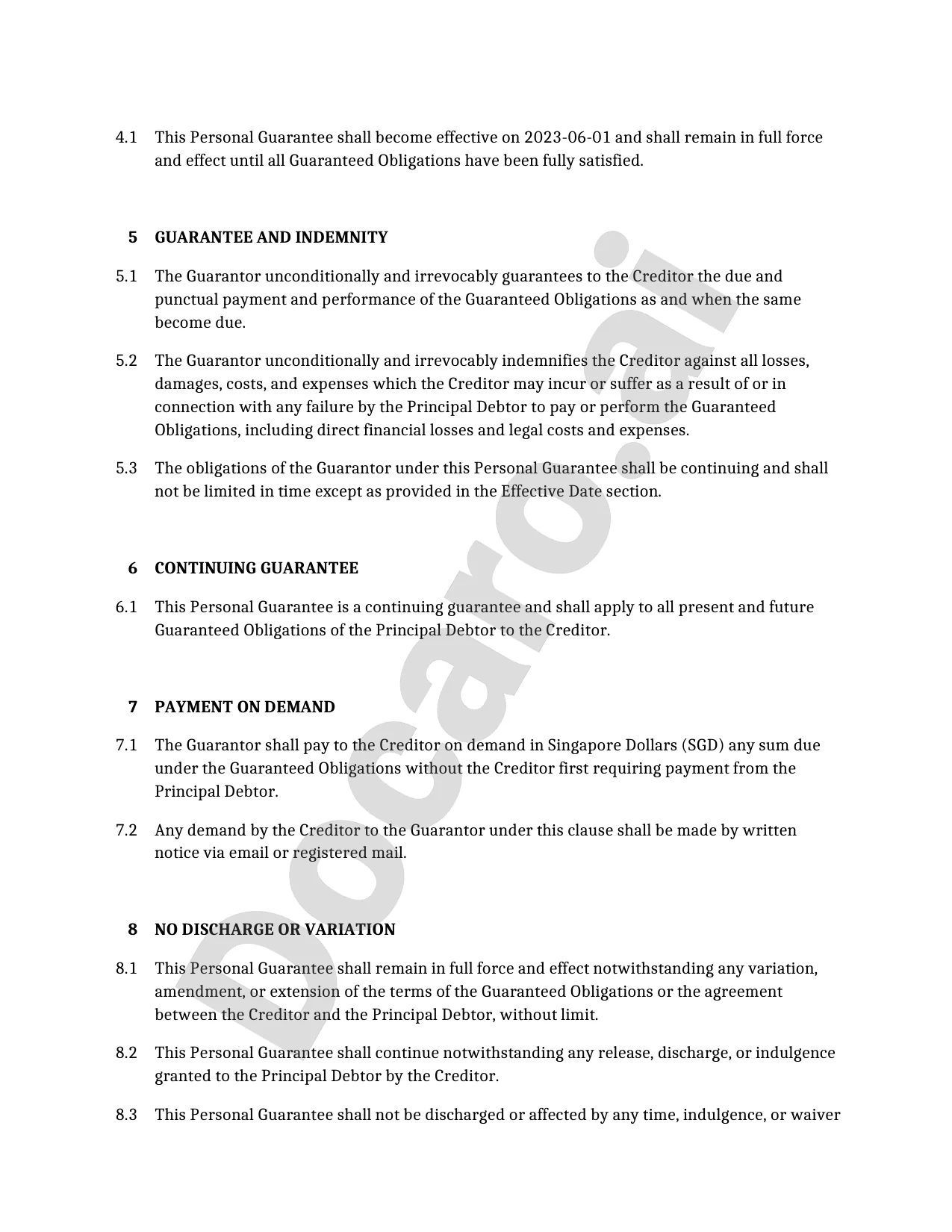

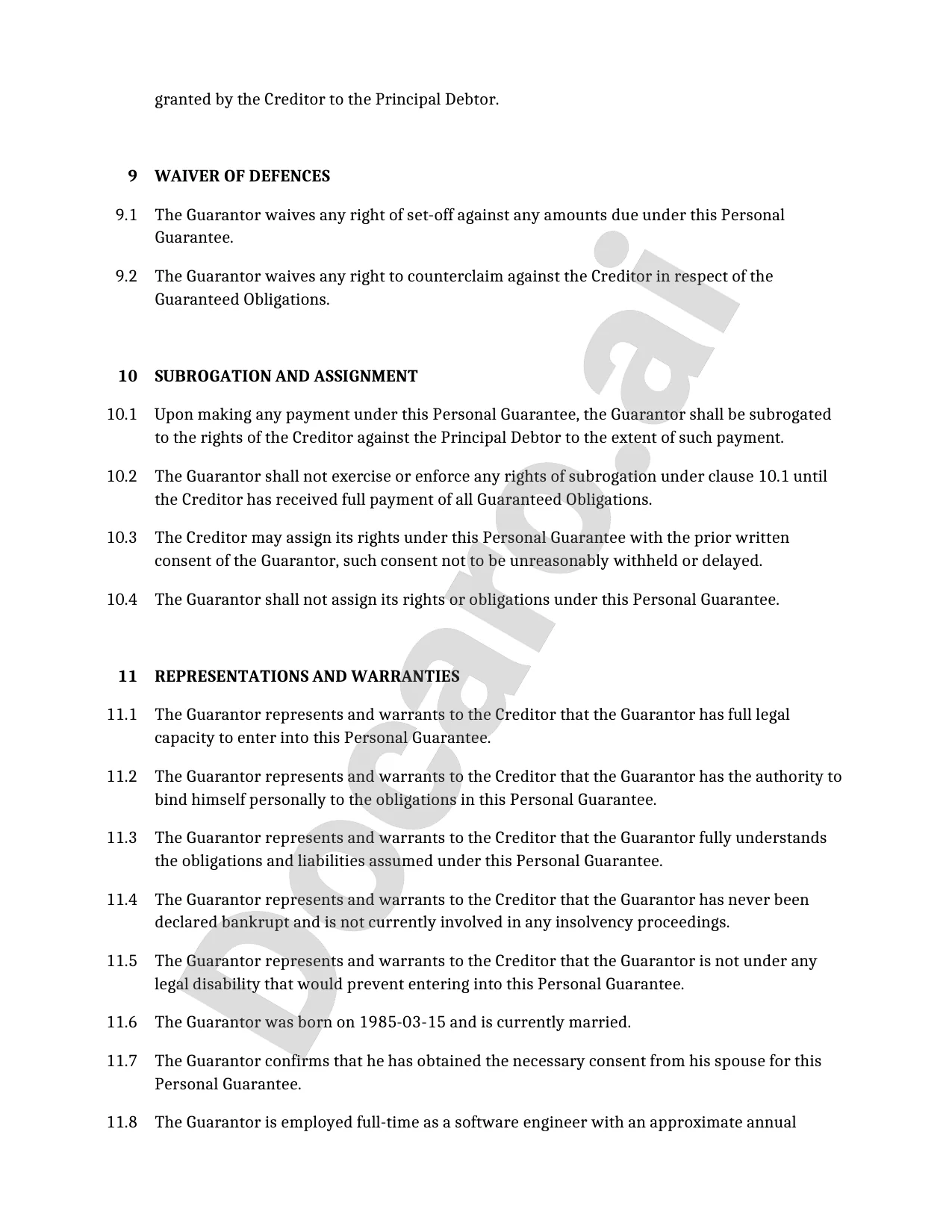

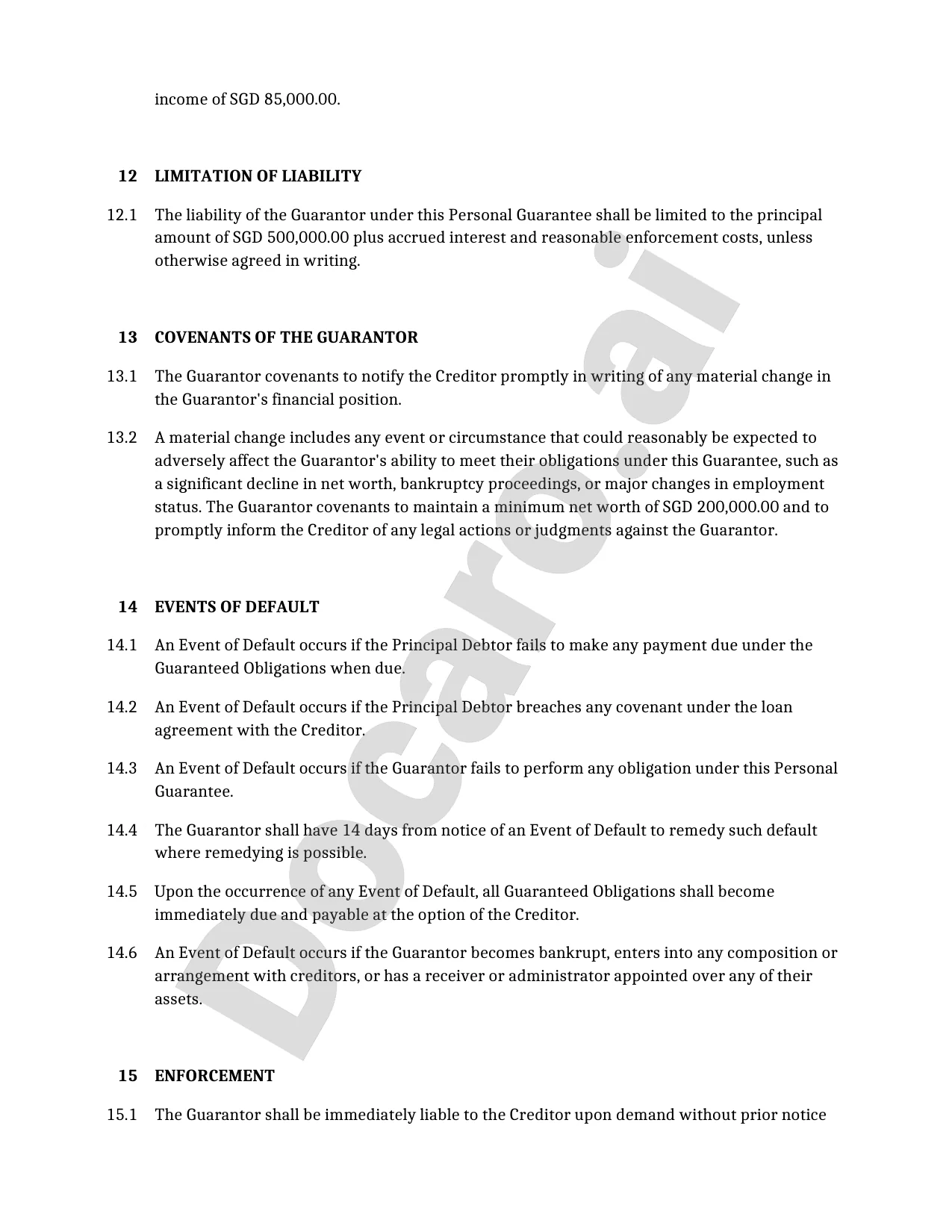

SingaporeFree Example Personal Guarantee Template

Below is a free template example of a Personal Guarantee for use in Singapore generated by our AI model.

The clauses in your actual Personal Guarantee will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

Useful Resources When Considering a Personal Guarantee in Singapore

Singapore Reference Legislation

Personal Guarantee FAQs

Document Generation FAQs

Related Articles