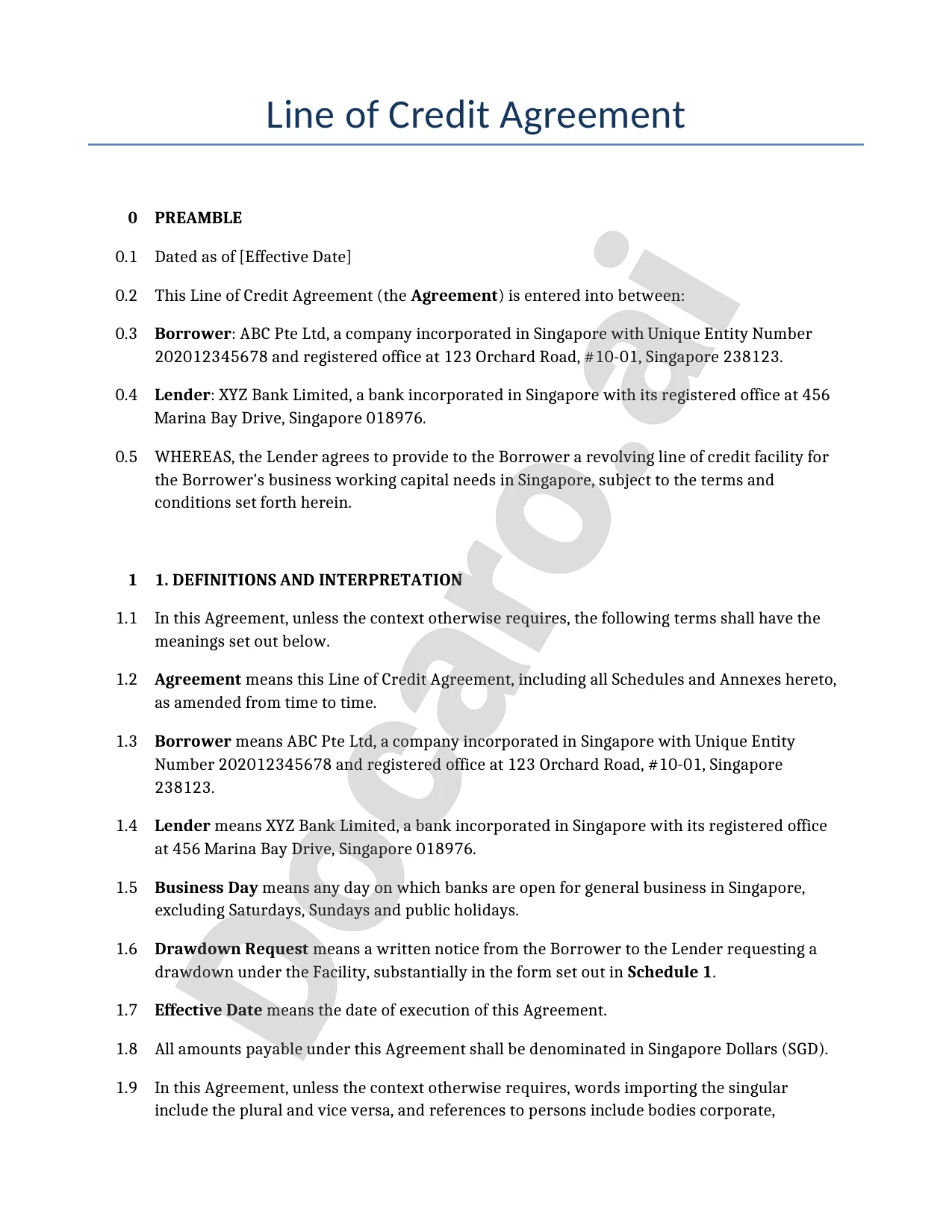

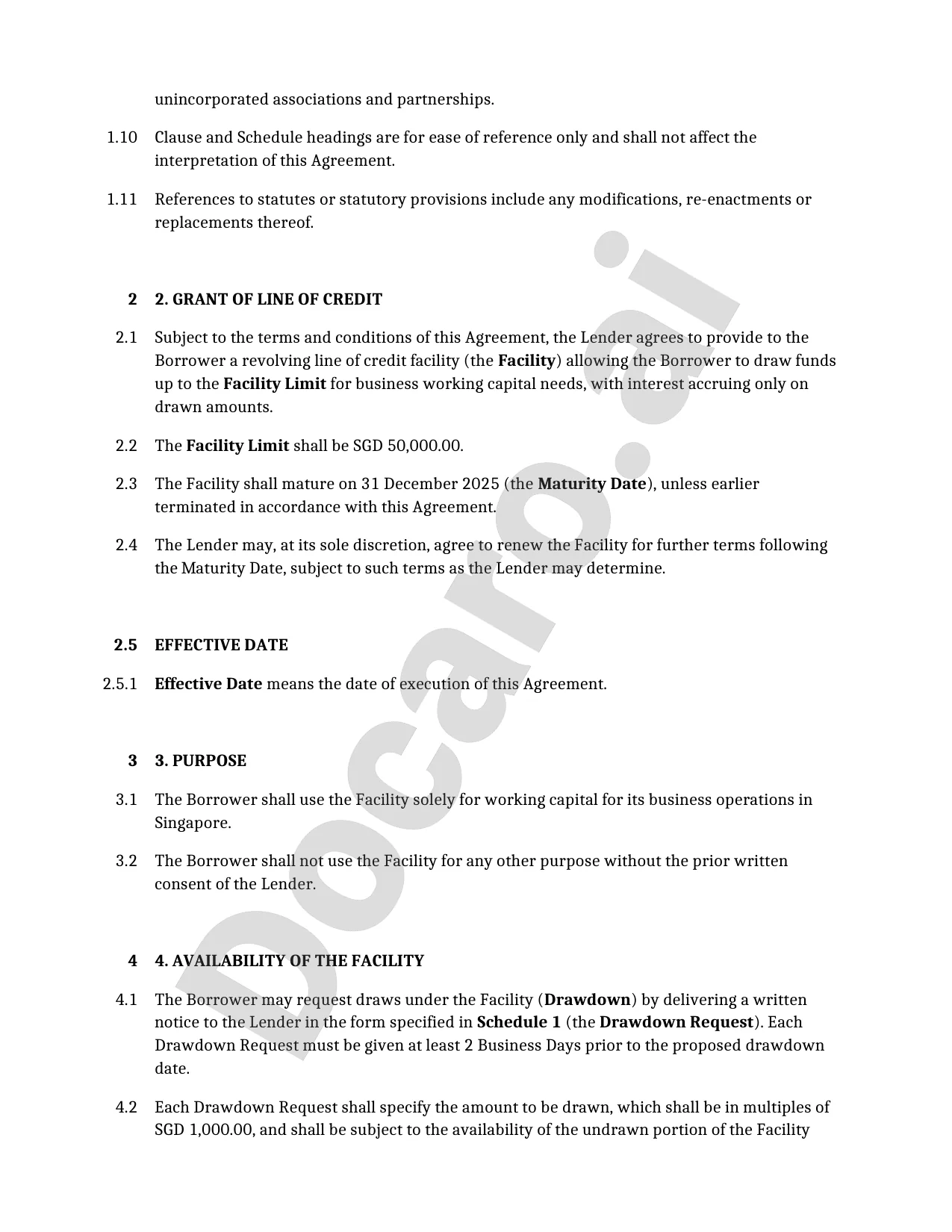

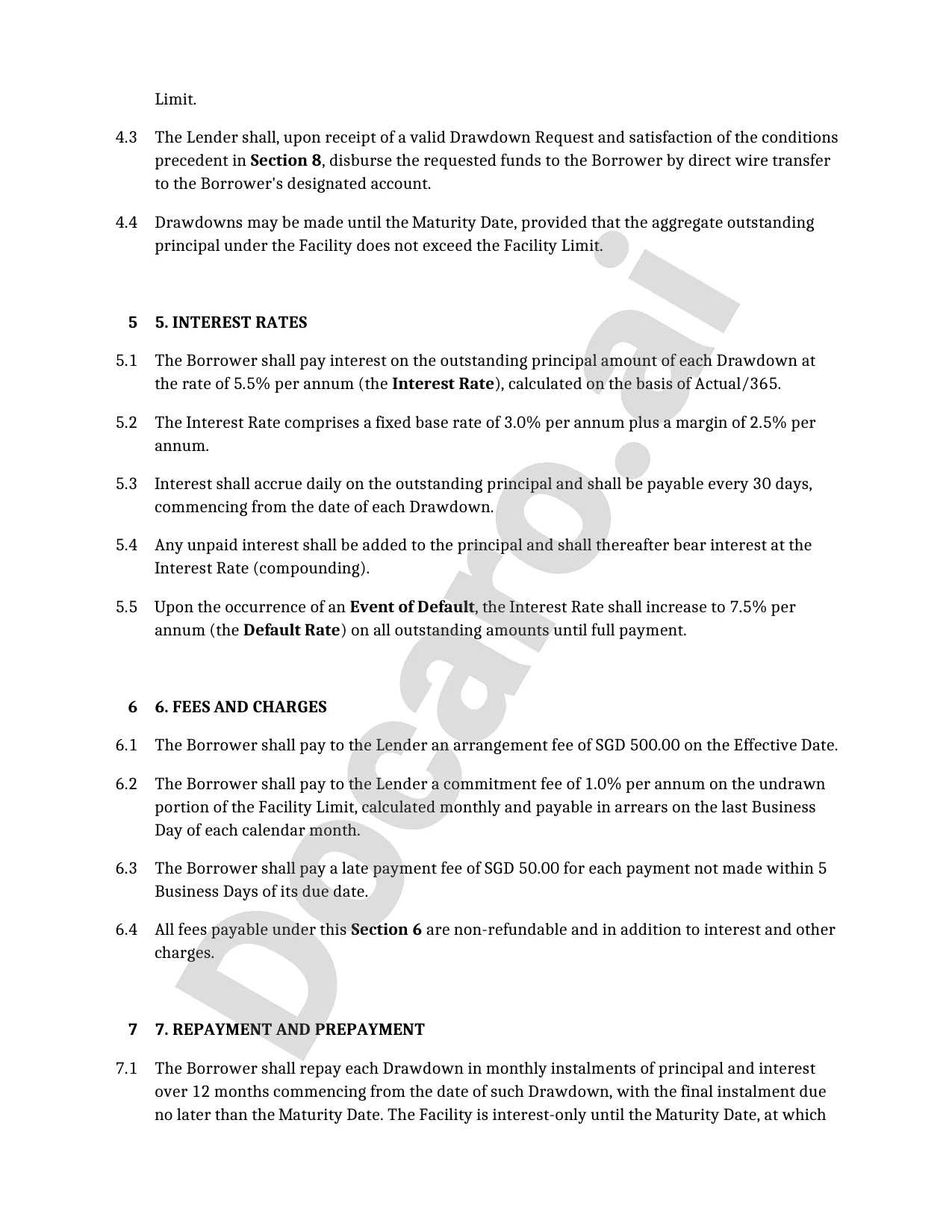

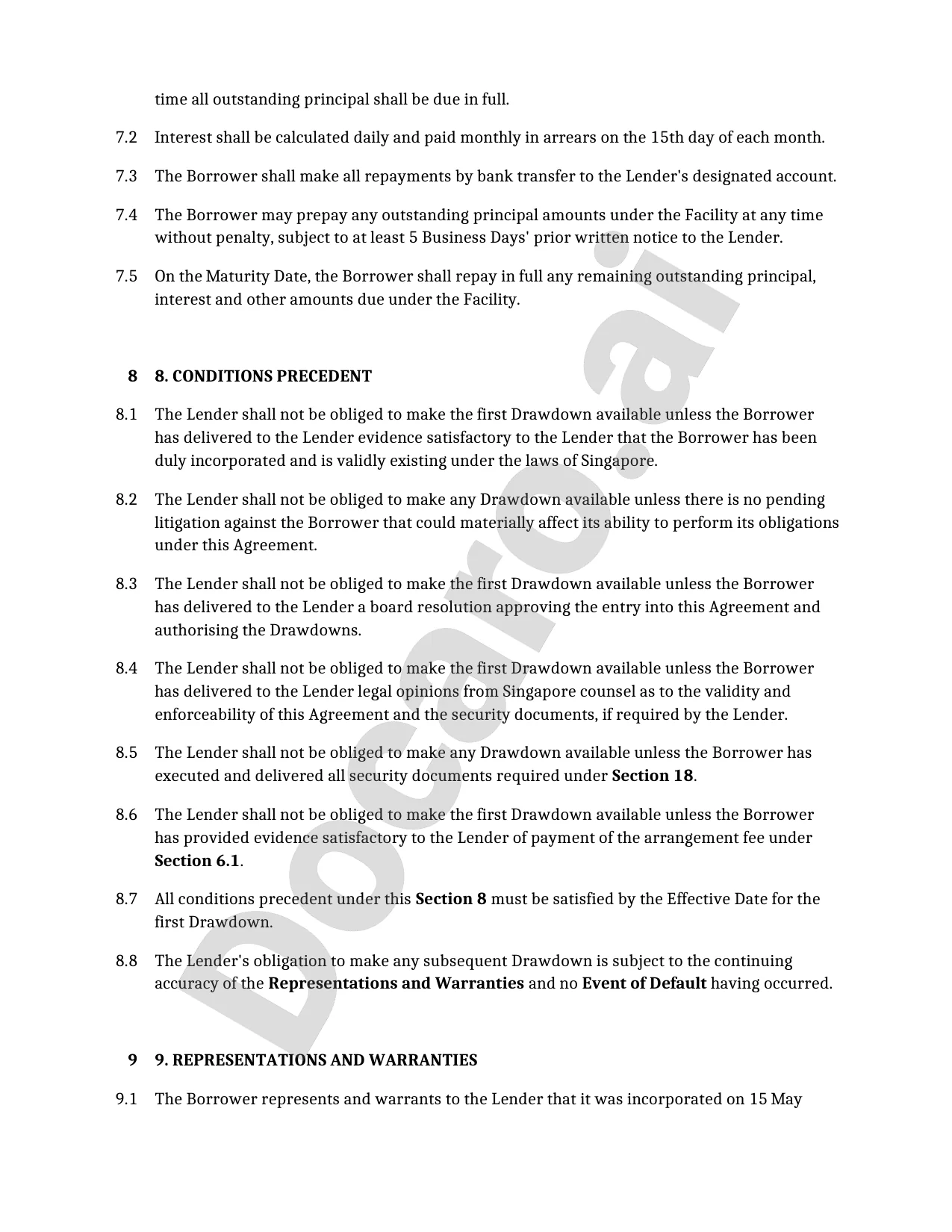

AI Generated Singaporean Line of Credit Agreement

PDF & Word - 2026 Updated

Docaro Pricing

When do you need a Line of Credit Agreement in Singapore?

- Borrowing repeatedly from a lenderUse this agreement when you need flexible access to funds up to a set limit without applying for a new loan each time.

- Business expansion or cash flow needsIt's essential for companies facing temporary shortfalls or growth opportunities to maintain smooth operations.

- Personal financial flexibilityIndividuals can use it for ongoing expenses like home improvements or education without rigid repayment schedules.

- Protecting both parties' interestsA well-drafted agreement clearly outlines terms like interest rates and repayment to prevent misunderstandings and disputes.

- Ensuring legal compliance in SingaporeIt helps meet local financial regulations, reducing risks of penalties or invalid terms in court.

Singaporean Legal Rules for a Line of Credit Agreement

- Governing LawLine of credit agreements in Singapore are primarily governed by the common law and principles from the Sale of Goods Act, adapted for financial services.

- Interest RatesInterest on lines of credit must be clearly stated and cannot exceed the maximum rate set by Singapore's Moneylenders Act if the lender is licensed as a moneylender.

- Borrower ProtectionsAgreements must include protections against unfair terms, ensuring borrowers receive clear information on fees, repayment, and default consequences under consumer protection laws.

- Disclosure RequirementsLenders are required to provide full disclosure of all terms, including risks and costs, to comply with the Credit Agreements and Promotions (Exclusion) Regulations.

- Default and EnforcementIn case of default, lenders can enforce the agreement through legal action, but must follow fair debt collection practices outlined in Singapore's regulations.

- Licensing for LendersNon-bank lenders offering lines of credit often need a license from the Ministry of Law under the Moneylenders Act to operate legally in Singapore.

- Dispute ResolutionAgreements should specify how disputes will be resolved, typically through Singapore courts or arbitration, in line with the Arbitration Act.

Using the wrong structure for a line of credit agreement may lead to unenforceable terms or unintended liabilities under Singapore's financial regulations.

What a Proper Line of Credit Agreement Should Include

- Parties InvolvedClearly identify the lender and borrower, including their full names, addresses, and contact details.

- Credit LimitSpecify the maximum amount the borrower can access from the line of credit.

- Interest RatesDetail how interest is calculated, including the rate and when it starts applying to borrowed amounts.

- Repayment TermsOutline the schedule for repaying the borrowed funds, including minimum payments and due dates.

- Fees and ChargesList any fees for setup, usage, late payments, or exceeding the credit limit.

- Security or CollateralDescribe any assets or guarantees the lender can claim if the borrower fails to repay.

- Default ConditionsExplain what happens if the borrower misses payments or breaches the agreement, like acceleration of full repayment.

- Termination RulesState how and when either party can end the agreement, including notice periods.

- Governing LawConfirm that Singapore law applies to the agreement and any disputes.

Why Free Templates Can Be Risky for Line of Credit Agreements

Generic free templates for line of credit agreements often overlook Singapore-specific regulations, such as those under the Banking Act or consumer protection laws. Inaccurate terms can lead to unenforceable clauses, disputes over interest rates, or non-compliance with disclosure requirements, potentially resulting in financial losses or legal challenges.

AI-generated bespoke line of credit agreements are customized to your exact needs, incorporating Singapore's legal standards and precise details like loan amounts, repayment schedules, and security interests. This ensures a robust, enforceable document tailored for your situation, minimizing risks and providing clarity for all parties.

Generate Your Document in 4 Easy Steps

Why Use Our Docaro?

Singapore

SingaporeFree Example Line of Credit Agreement Template

Below is a free template example of a Line of Credit Agreement for use in Singapore generated by our AI model.

The clauses in your actual Line of Credit Agreement will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

Useful Resources When Considering a Line of Credit Agreement in Singapore

Singapore Reference Legislation

Line of Credit Agreement FAQs

Document Generation FAQs

Related Articles