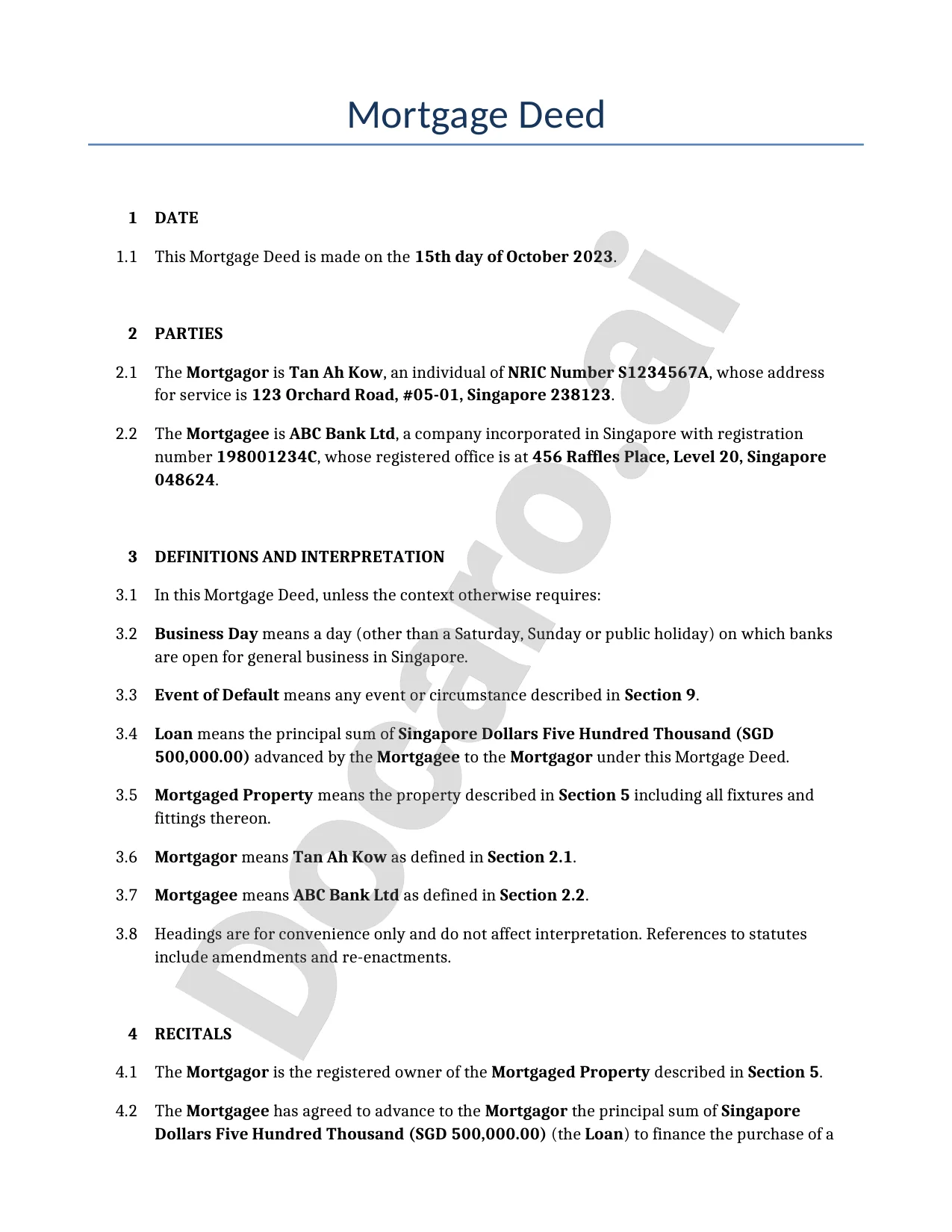

AI Generated Singaporean Mortgage Deed

PDF & Word - 2026 Updated

Docaro Pricing

When do you need a Mortgage Deed in Singapore?

- Securing a Home LoanYou need a mortgage deed when borrowing money from a bank to buy property, as it acts as a promise that the property can be taken if you don't repay the loan.

- Protecting the LenderThis document is essential for lenders to legally claim the property if payments are missed, ensuring they recover their money.

- Formalizing Property OwnershipIt records the agreement between borrower and lender, making the loan terms clear and official under Singapore law.

- Avoiding Loan DisputesA well-drafted mortgage deed prevents misunderstandings by clearly outlining repayment details, interest, and consequences of default.

- Ensuring Legal ValidityUsing a properly prepared document helps avoid errors that could invalidate the agreement, protecting both parties from future legal issues.

Singaporean Legal Rules for a Mortgage Deed

- What It IsA mortgage deed is a legal agreement where you give your property as security to a lender in exchange for a loan, allowing the lender to take the property if you don't repay.

- Governing LawThese deeds are mainly controlled by Singapore's Conveyancing and Law of Property Act and the Land Titles Act, which set the rules for property transfers and securities.

- Key RequirementsThe deed must be in writing, signed by both parties, and witnessed to ensure it's valid and enforceable.

- RegistrationYou must register the mortgage with the Singapore Land Authority within a set time to protect your lender's rights against other claims on the property.

- Borrower's RightsAs the borrower, you keep ownership of the property and can use it normally, but the lender can step in if you miss payments.

- Repayment and ReleaseOnce you fully repay the loan, the lender must provide a discharge document to remove the mortgage from the property title.

- Foreclosure ProcessIf you default, the lender can apply to court to sell the property and recover the owed amount, following strict legal steps.

Using the wrong type of mortgage deed can invalidate the security interest or expose the lender to unforeseen liabilities.

What a Proper Mortgage Deed Should Include

- Parties InvolvedClearly identify the borrower and lender with their full names, addresses, and roles in the agreement.

- Property DetailsDescribe the property being mortgaged, including its address, size, and any unique identifiers like lot numbers.

- Loan AmountState the exact amount of the loan that the mortgage secures.

- Repayment TermsOutline how and when the loan must be repaid, including interest rates and payment schedules.

- Rights and ObligationsSpecify what the borrower must do to maintain the property and what happens if payments are missed.

- Default and RemediesExplain the consequences of failing to meet the agreement and the lender's options to recover the loan.

- Release ClauseDetail the conditions under which the mortgage will be removed once the loan is fully repaid.

- Governing LawConfirm that the deed follows Singapore's laws and is subject to its jurisdiction.

Why Free Templates Can Be Risky for Mortgage Deeds

Free mortgage deed templates often rely on generic clauses that fail to address Singapore-specific legal requirements, such as those under the Land Titles Act or stamp duty regulations. Incorrect wording can lead to unenforceable securities, disputes over priority of charges, or non-compliance with registry filing standards, potentially resulting in financial losses or invalidation of the mortgage.

AI-generated bespoke mortgage deeds are tailored to your specific transaction details, incorporating precise Singapore-compliant language for parties, property descriptions, interest rates, and covenants. This ensures a robust, enforceable document that minimizes risks and aligns perfectly with local laws, providing superior protection for lenders and borrowers.

Generate Your Document in 4 Easy Steps

Why Use Our Docaro?

Singapore

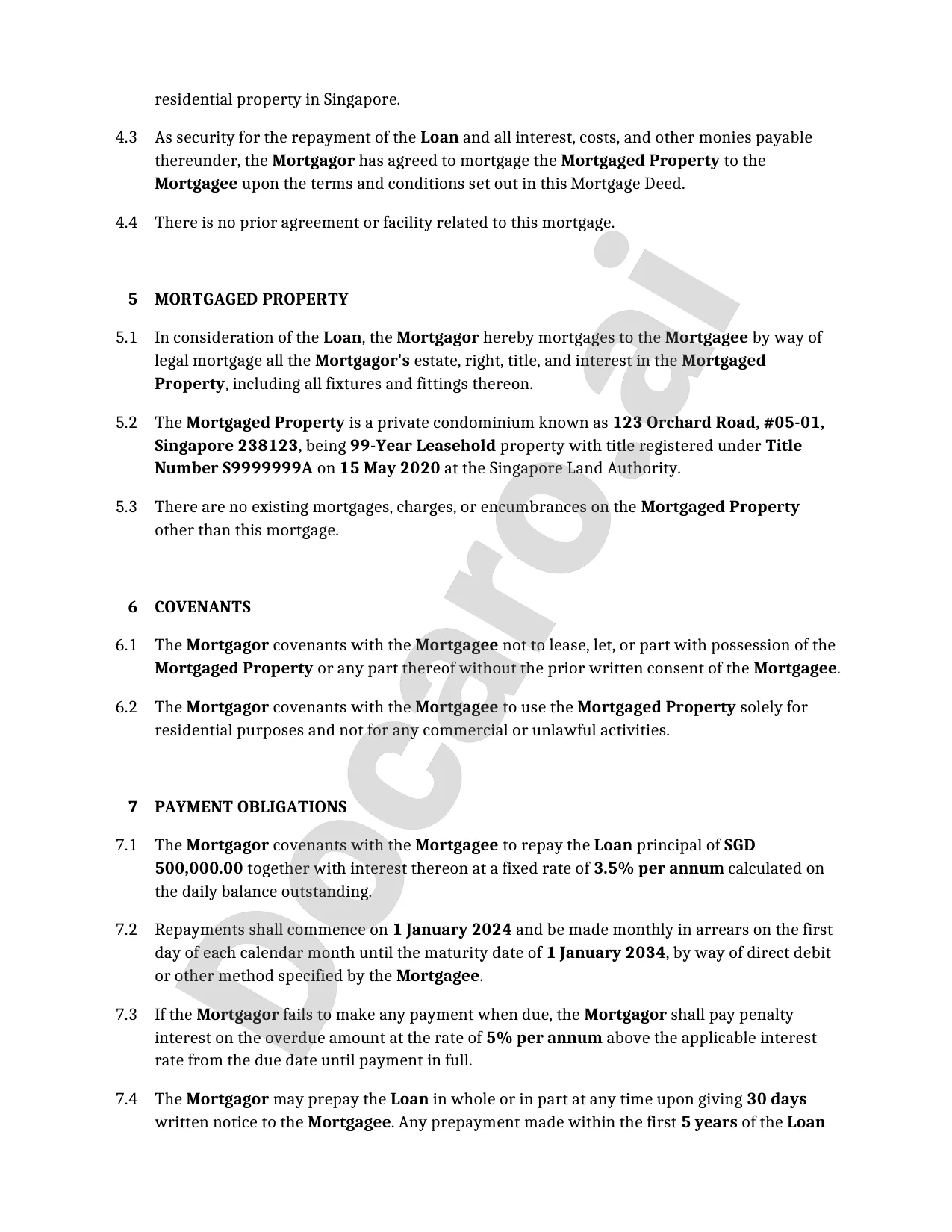

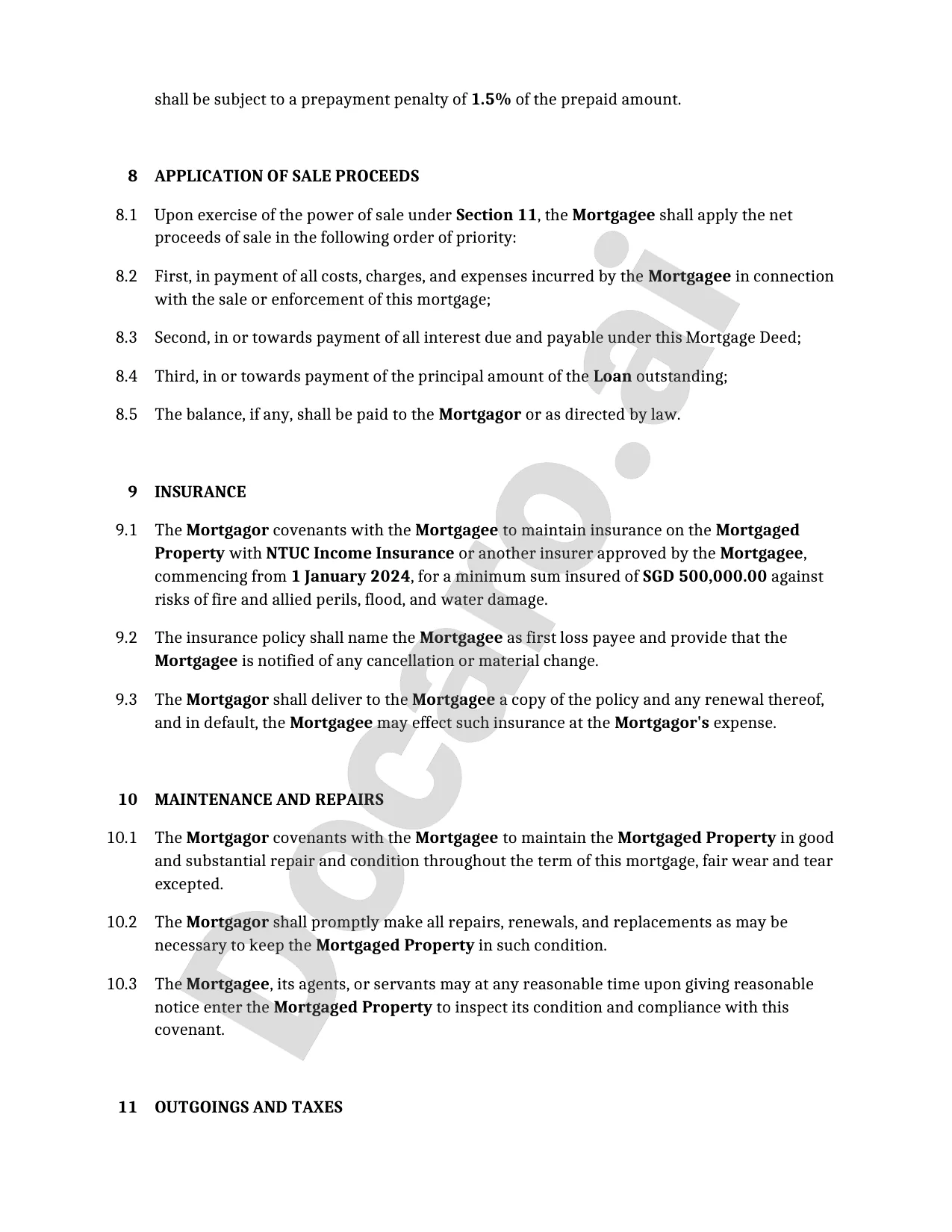

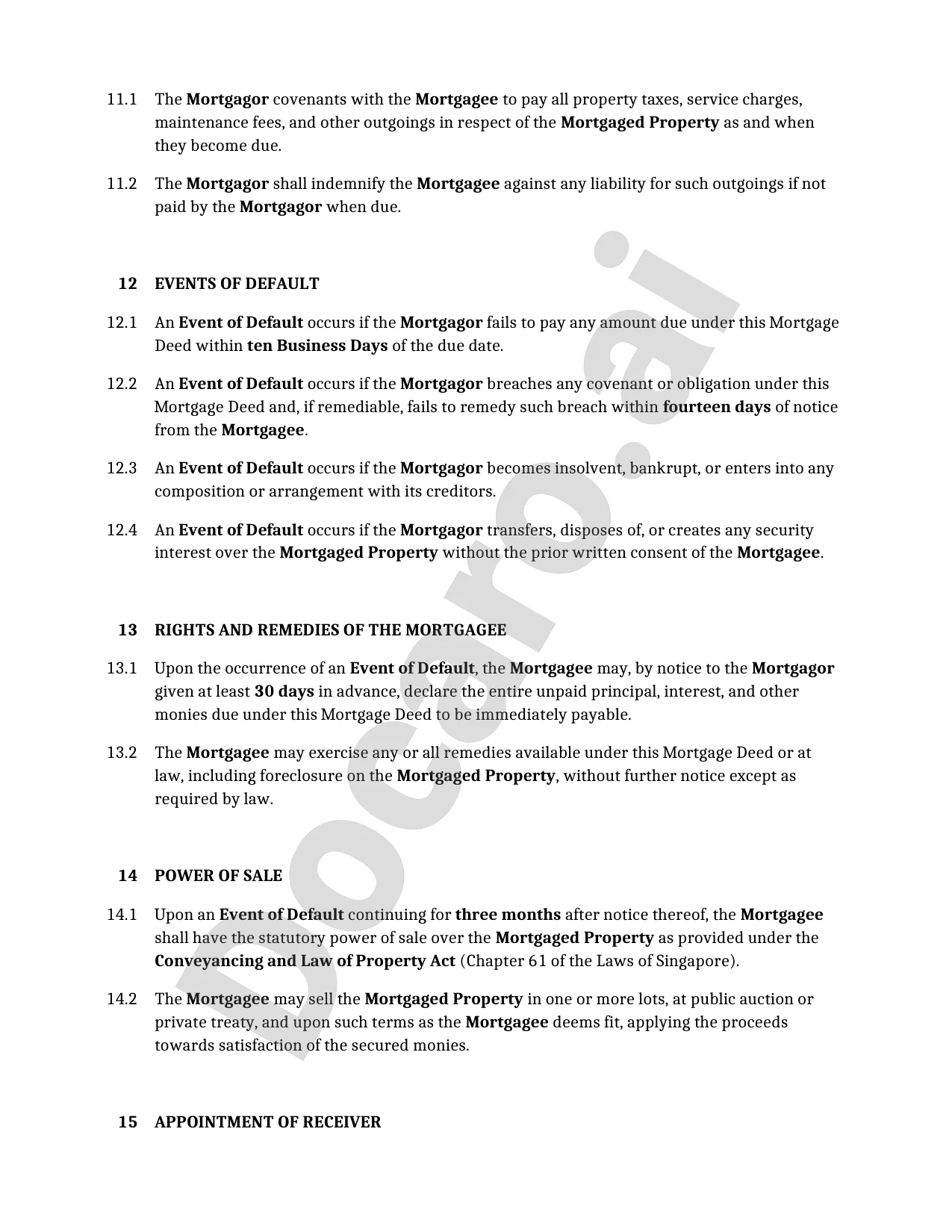

SingaporeFree Example Mortgage Deed Template

Below is a free template example of a Mortgage Deed for use in Singapore generated by our AI model.

The clauses in your actual Mortgage Deed will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

Useful Resources When Considering a Mortgage Deed in Singapore

Singapore Reference Legislation

Mortgage Deed FAQs

Document Generation FAQs

Related Articles