AI Generated Singaporean Debt Settlement Agreement

PDF & Word - 2026 Updated

Docaro Pricing

When Do You Need a Debt Settlement Agreement in Singapore?

- Resolving Unpaid DebtsYou need this agreement when you and your creditor want to settle an outstanding debt through a one-time payment or revised terms instead of full repayment.

- Avoiding Legal DisputesIt helps prevent court battles by clearly outlining how the debt will be handled, giving both sides peace of mind.

- Handling Financial HardshipsThis document is useful during tough times, like job loss or illness, to negotiate affordable repayment options with your creditor.

- Protecting Both PartiesA well-drafted agreement ensures the creditor gets paid and the debtor avoids further collection efforts, reducing future misunderstandings.

- Importance of Proper DraftingHaving a clear and complete document is crucial to make the settlement legally binding and enforceable under Singapore law, avoiding potential issues later.

Singaporean Legal Rules for a Debt Settlement Agreement

- Voluntary AgreementBoth the debtor and creditor must willingly agree to the terms without any pressure or force.

- Clear TermsThe agreement should clearly state the original debt amount, the settlement amount, payment method, and deadline to avoid misunderstandings.

- Consideration RequiredThere must be something of value exchanged, like a reduced payment or new promise, to make the agreement legally binding.

- Written Form PreferredWhile oral agreements can work, writing everything down helps prove the terms in case of disputes.

- Governed by Contract LawThe agreement follows Singapore's general rules for contracts, ensuring fairness and enforceability.

- Enforceable in CourtIf followed properly, the agreement can be upheld by Singapore courts if one party doesn't stick to it.

- Impact on CreditSettling a debt may affect the debtor's credit record, so check with credit bureaus for details.

- Seek Professional AdviceIt's wise to consult a lawyer to ensure the agreement fits your specific situation and complies with all rules.

Using the wrong structure for a debt settlement agreement can invalidate waivers or expose parties to ongoing legal liabilities.

What a Proper Debt Settlement Agreement Should Include

- Parties InvolvedClearly identify the debtor and creditor, including their full names and contact details.

- Original Debt DetailsDescribe the original debt amount, how it arose, and any interest or fees accumulated.

- Settlement AmountSpecify the exact amount agreed upon to settle the debt, which may be less than the full owed.

- Payment TermsOutline how and when the settlement amount will be paid, such as in a lump sum or installments.

- Release of ClaimsState that once paid, the creditor will forgive the remaining debt and not pursue further action.

- ConfidentialityAgree to keep the settlement details private between the parties.

- Signatures and DateInclude spaces for both parties to sign and date the agreement to make it binding.

Why Free Templates Can Be Risky for Debt Settlement Agreements

Generic free templates for debt settlement agreements often fail to address Singapore-specific legal requirements, such as compliance with the Limitation Act or proper structuring under contract law. Inaccurate clauses may lead to unenforceable terms, disputes over payment schedules, or unintended tax implications, potentially worsening your financial situation instead of resolving it.

Our AI-generated bespoke debt settlement agreements are customized to your unique circumstances, incorporating precise Singapore legal standards for clear, enforceable terms that protect all parties and facilitate smooth resolution without hidden pitfalls.

Generate Your Document in 4 Easy Steps

Why Use Our Docaro?

Singapore

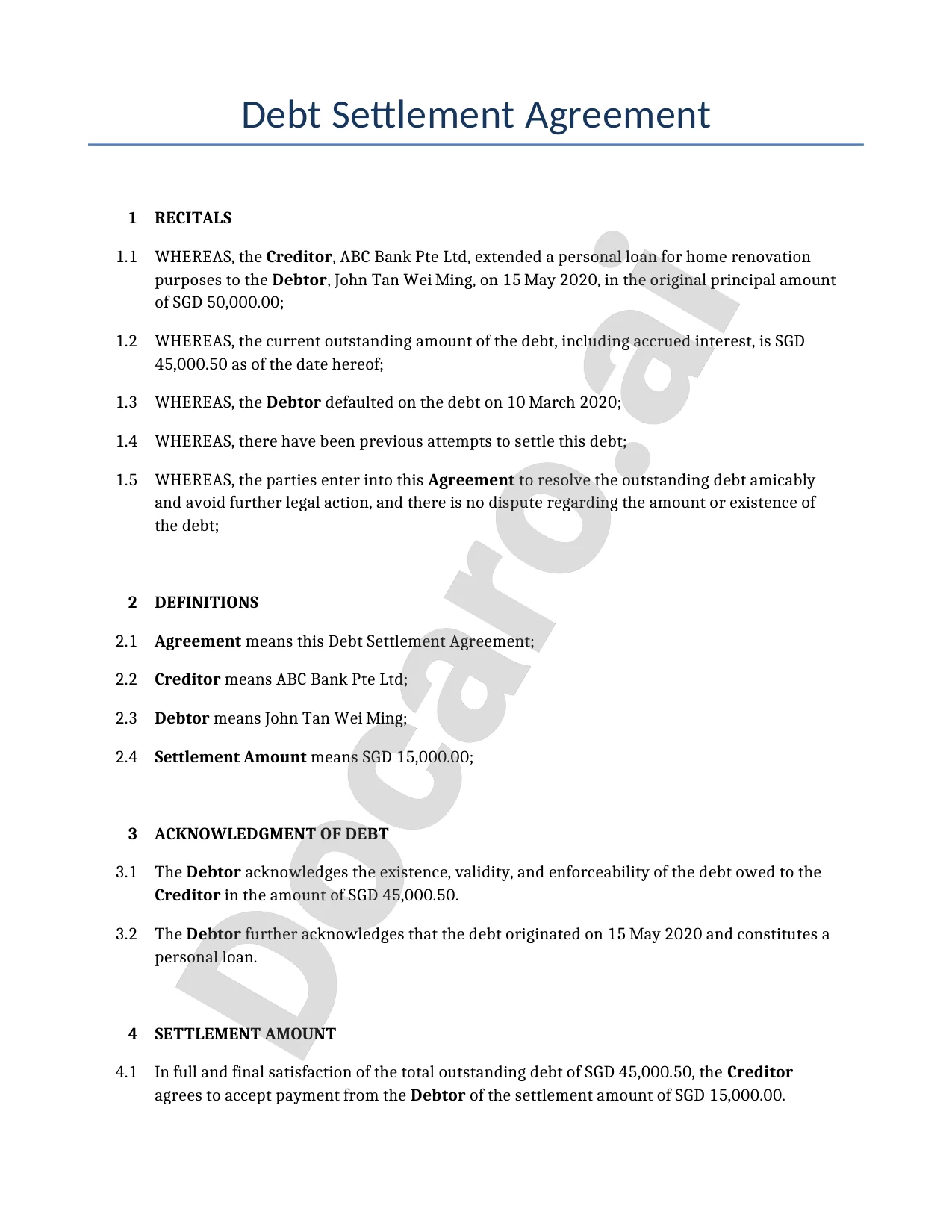

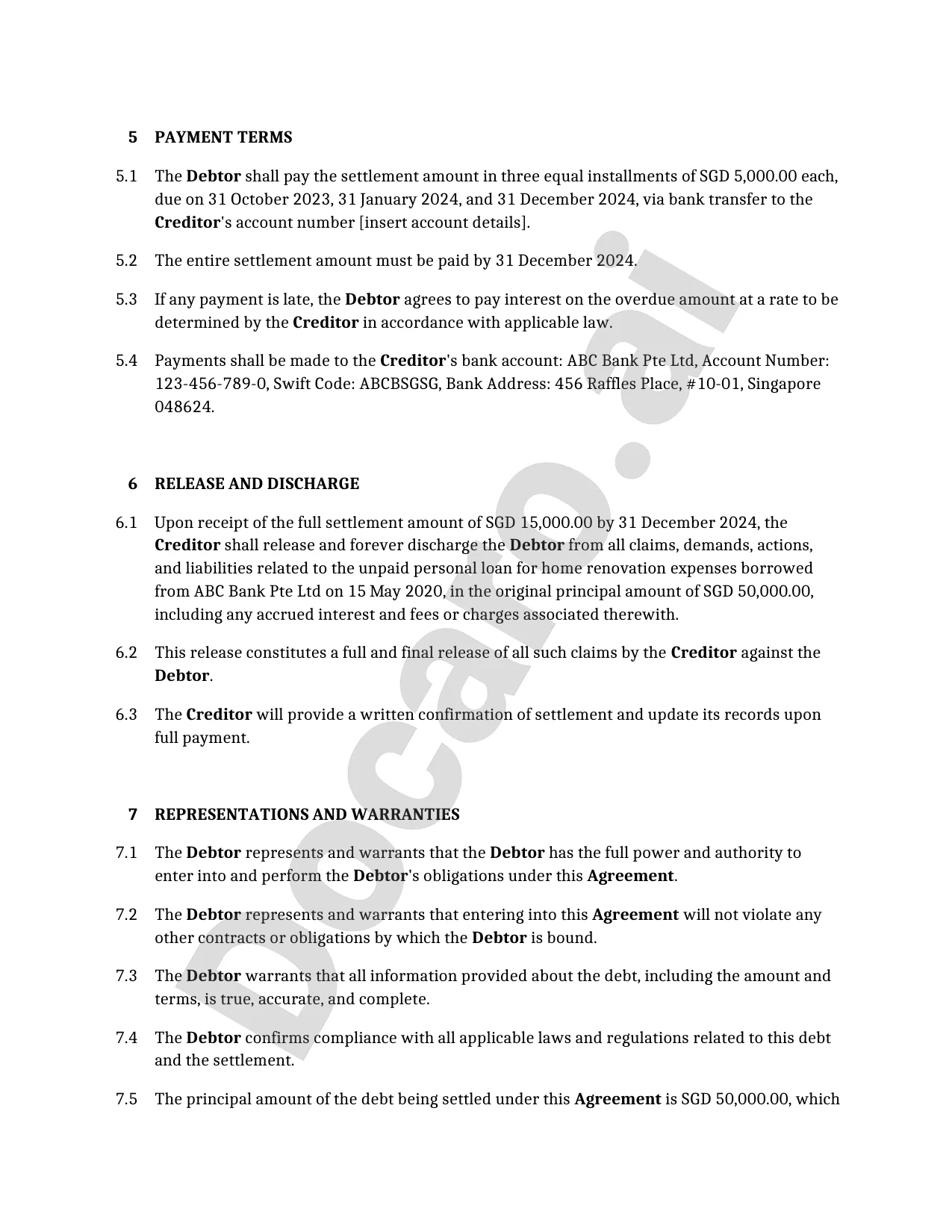

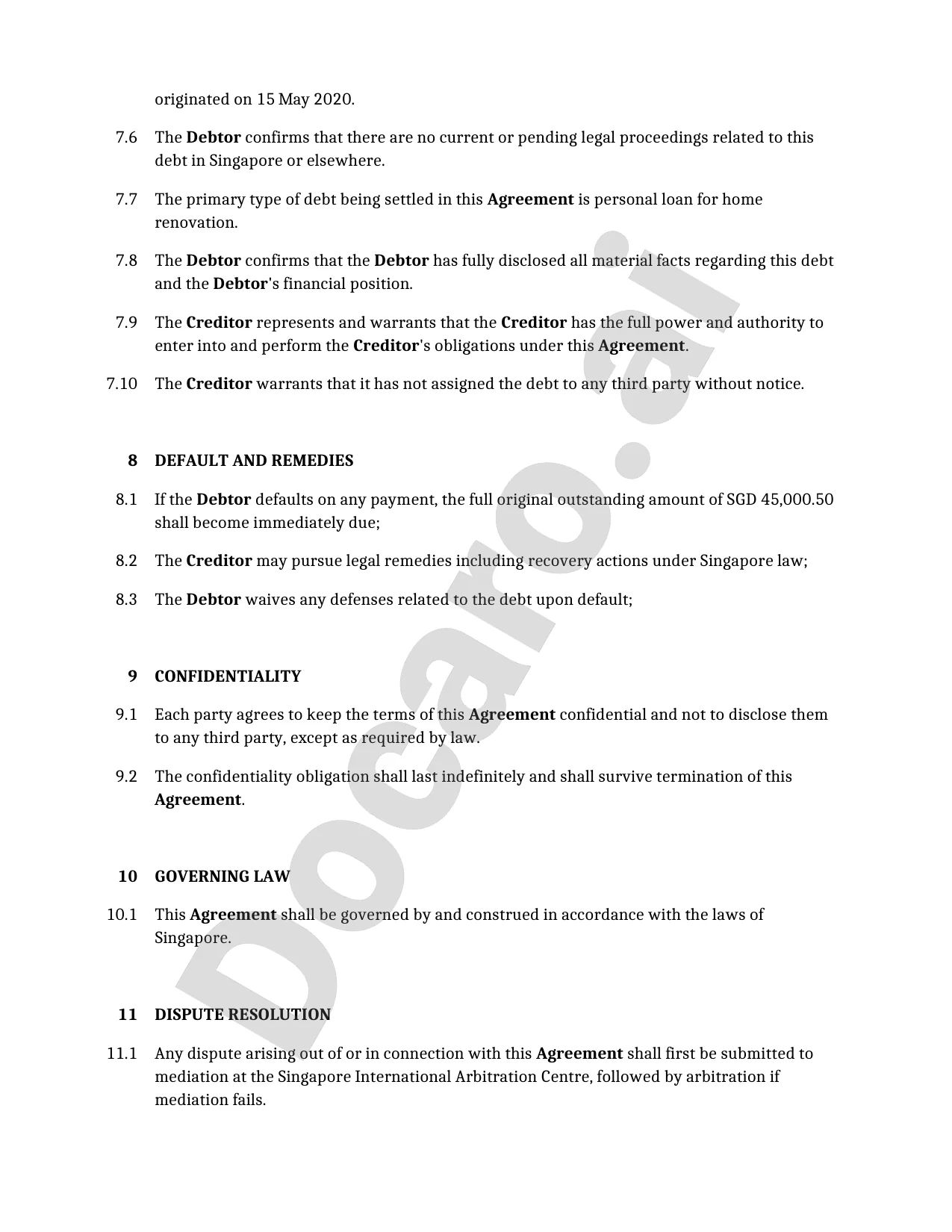

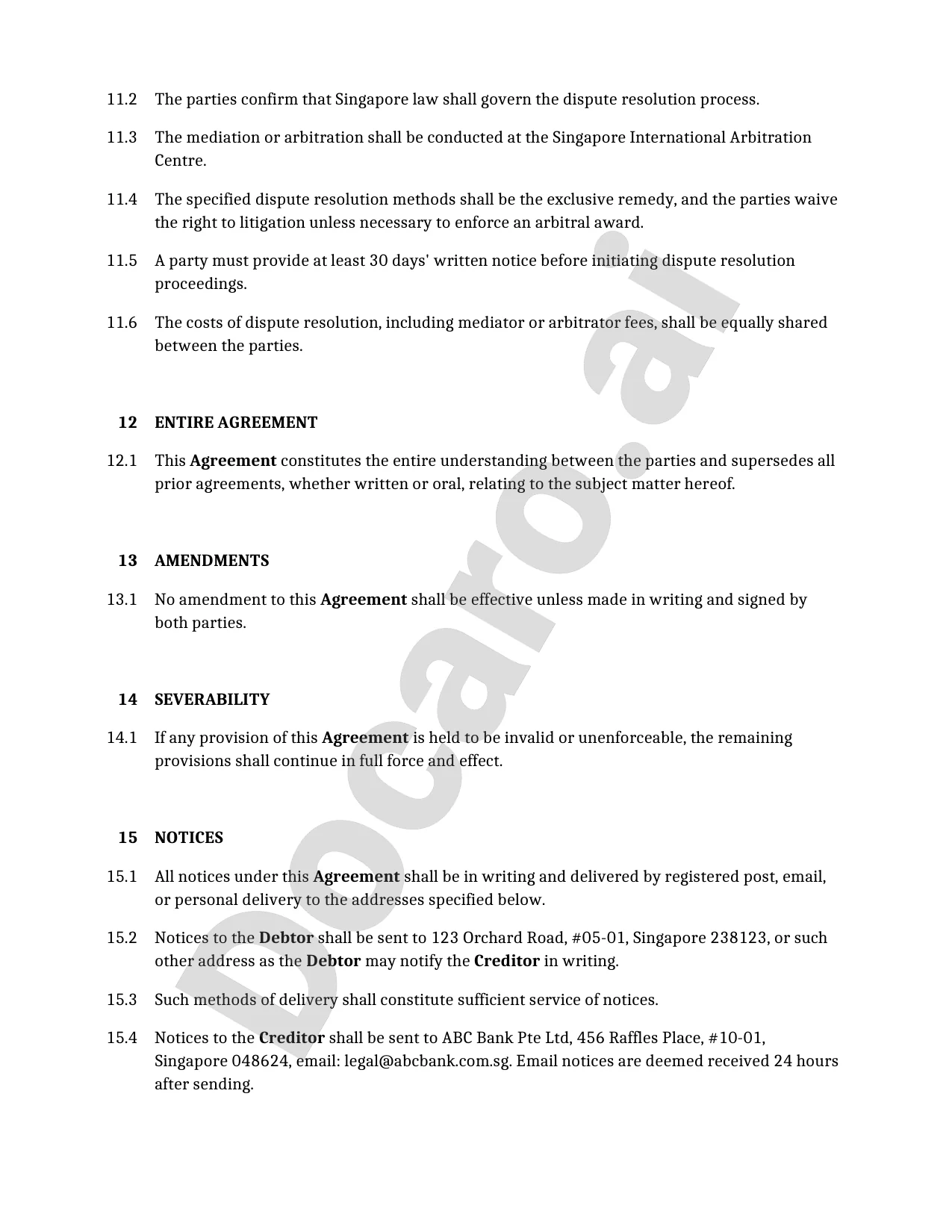

SingaporeFree Example Debt Settlement Agreement Template

Below is a free template example of a Debt Settlement Agreement for use in Singapore generated by our AI model.

The clauses in your actual Debt Settlement Agreement will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

Useful Resources When Considering a Debt Settlement Agreement in Singapore

Singapore Reference Legislation

Debt Settlement Agreement FAQs

Document Generation FAQs

Related Articles