AI 生成的中国的抵押契约

PDF & Word - 2026 已更新

使用AI智能工具快速生成中国抵押契约模板,专业可靠,支持房产抵押、贷款担保等场景,助您高效办理抵押手续。

免费即时文件创建。

根据 中国 法律量身定制。

无需注册或月度订阅。

Docaro 定价

基本

免费

文档生成

无需注册

无订阅

下载带水印的 PDF

高级

$4.99 USD

文档生成

无需注册

无订阅

下载干净的 PDF

下载 Microsoft Word

下载 HTML

下载文本

电子邮件文档

免费生成您的文档。 仅当您喜欢结果 并需要无水印版本时付费。

在中国何时需要抵押契约?

- 购买房产时当你用房产作为贷款担保时,需要抵押契约来证明房产归属于抵押方。

- 获得银行贷款时抵押契约帮助确保贷款人能收回资金,如果借款人无法偿还。

- 企业融资时公司可以用资产抵押来获取资金,契约记录抵押细节以保护各方权益。

- 避免纠纷时一份清晰的抵押契约可以防止误解和法律冲突,确保交易顺利。

- 符合法律要求时在中国,抵押资产必须通过正式契约登记,以获得法律保护和有效性。

- 为什么需要专业起草专业的抵押契约能避免错误,确保所有条款符合法规并保护你的利益。

中国抵押契约的法律规则

- 抵押物要求抵押物必须是合法拥有的财产,如房屋或土地使用权,不能是非法所得。

- 当事人资格抵押人和抵押权人必须是具有完全民事行为能力的自然人或法人。

- 合同形式抵押契约应采用书面形式,并由当事人签字或盖章。

- 登记生效不动产抵押需到相关部门登记后才生效,动产可不登记但建议办理。

- 抵押范围抵押可担保未来的债务,但范围限于约定的债权数额。

- 权利实现债务人未还款时,抵押权人有权拍卖抵押物以优先受偿。

- 禁止事项不得抵押已设定其他权利的财产,或违反国家禁止抵押的财产类型。

重要

使用错误的抵押契约类型或结构可能导致财产权利归属不明或法律效力失效。

一份合适的抵押契约应包含什么

- 抵押人信息明确列出抵押人的姓名、身份证号和联系方式。

- 抵押权人信息详细说明抵押权人的姓名、机构名称和联系方式。

- 主债权描述清楚说明被担保的债务金额、利息和还款期限。

- 抵押财产详情准确描述抵押物的类型、数量、位置和价值。

- 抵押范围定义抵押担保的主债权的具体内容,包括本金和利息。

- 生效与终止条件规定抵押何时生效以及债务清偿后如何终止。

- 权利与义务说明抵押人对财产的维护责任和抵押权人的优先受偿权。

- 违约处理描述如果借款人违约时抵押权人如何处置抵押物。

- 争议解决约定发生纠纷时通过何种方式如仲裁或诉讼解决。

- 签名与日期要求双方签字并注明签订日期以确保有效性。

为什么免费模板使用抵押契约有风险

大多数免费抵押契约模板基于标准条款,未考虑具体财产细节、借款人情况或当地法规差异。错误表述可能导致合同无效、抵押权无法执行,或引发财产纠纷和法律责任。

AI生成的定制抵押契约根据您的具体信息量身定制,确保条款准确、合规,并符合中国相关法律法规,提供更可靠的保护和执行力。

在4个简单步骤中生成您的文档

1

回答几个问题

我们的AI引导您完成所需信息。

2

生成您的文档

Docaro 根据您的要求定制专属文档。

3

审查 & 编辑

审核您的文档并提交任何进一步请求的更改。

4

下载 & 签署

将您的待签名文档下载为 PDF、Microsoft Word、Txt 或 HTML 格式。

Why Use Our Docaro?

快速生成

快速生成全面的 抵押契约,消除与传统文件起草相关的麻烦和时间。

引导过程

我们用户友好的平台将逐步指导您完成文档的每个部分,提供上下文和指导,以确保您提供所有必要的信息,以完成准确的抵押契约。

比合法模板更安全

我们从不使用法律模板。所有文件都是从基本原则逐条生成的,确保您的文件是量身定制的,并专门根据您提供的信息量身定制。这将产生比任何法律模板更安全、更准确的文件。

专业格式化

您的 抵押契约 将按照专业标准进行格式化,包括标题、条款编号和结构化布局。无需进一步编辑。下载您的文档(PDF、Microsoft Word、TXT 或 HTML)。

根据中国的法律量身定制

我们的AI模型在起草过程中考虑了中国最新的法律标准和法规。

划算

免费生成并下载带水印的文档版本。只有在您想要移除水印并获得文档的完全访问权限时才需要付费。没有每月订阅或隐藏费用。一次性付费,永久使用您的文档。

无需注册或每月订阅

无需付款或注册即可开始生成您的 抵押契约。

需要在其他国家生成 抵押契约 吗?

选择国家: 中国

中国

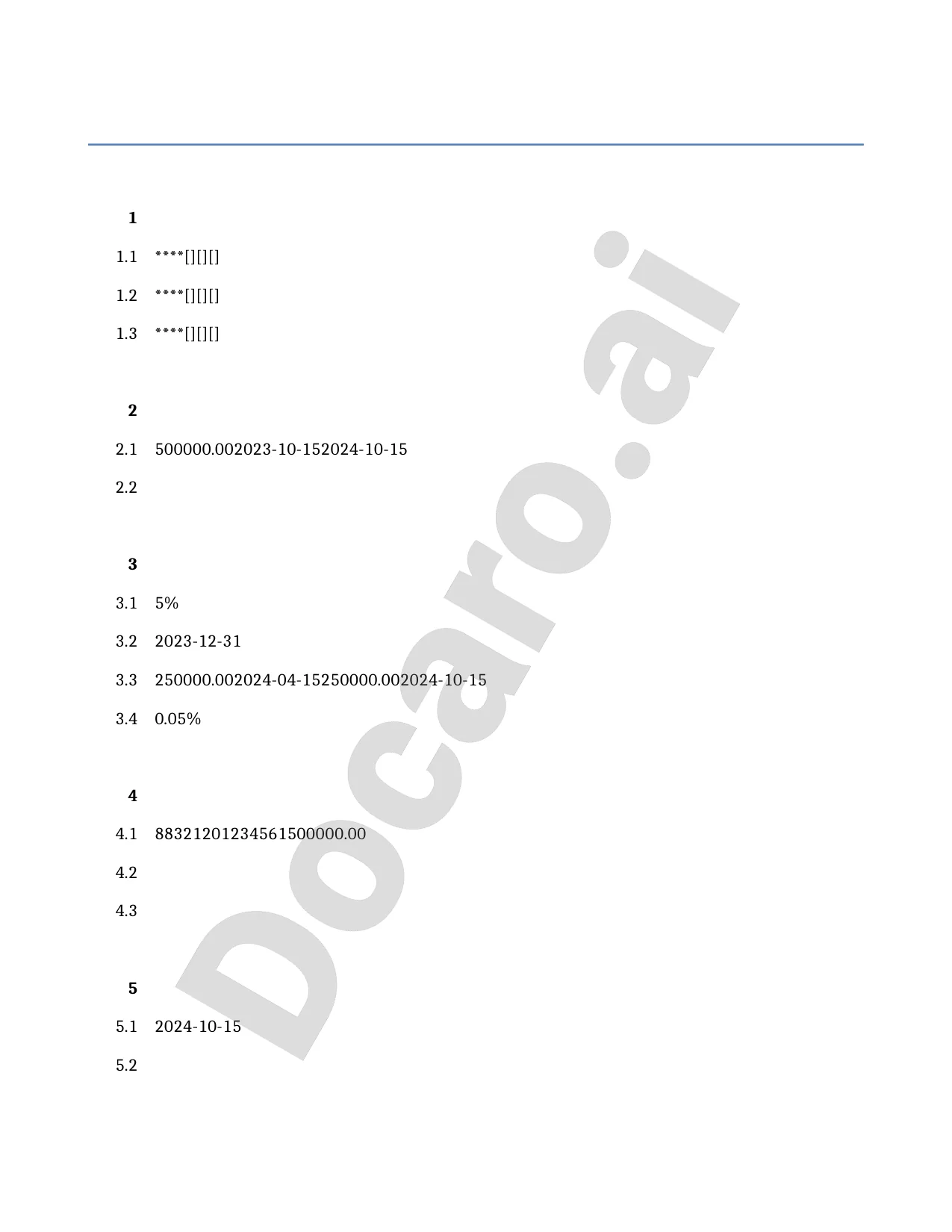

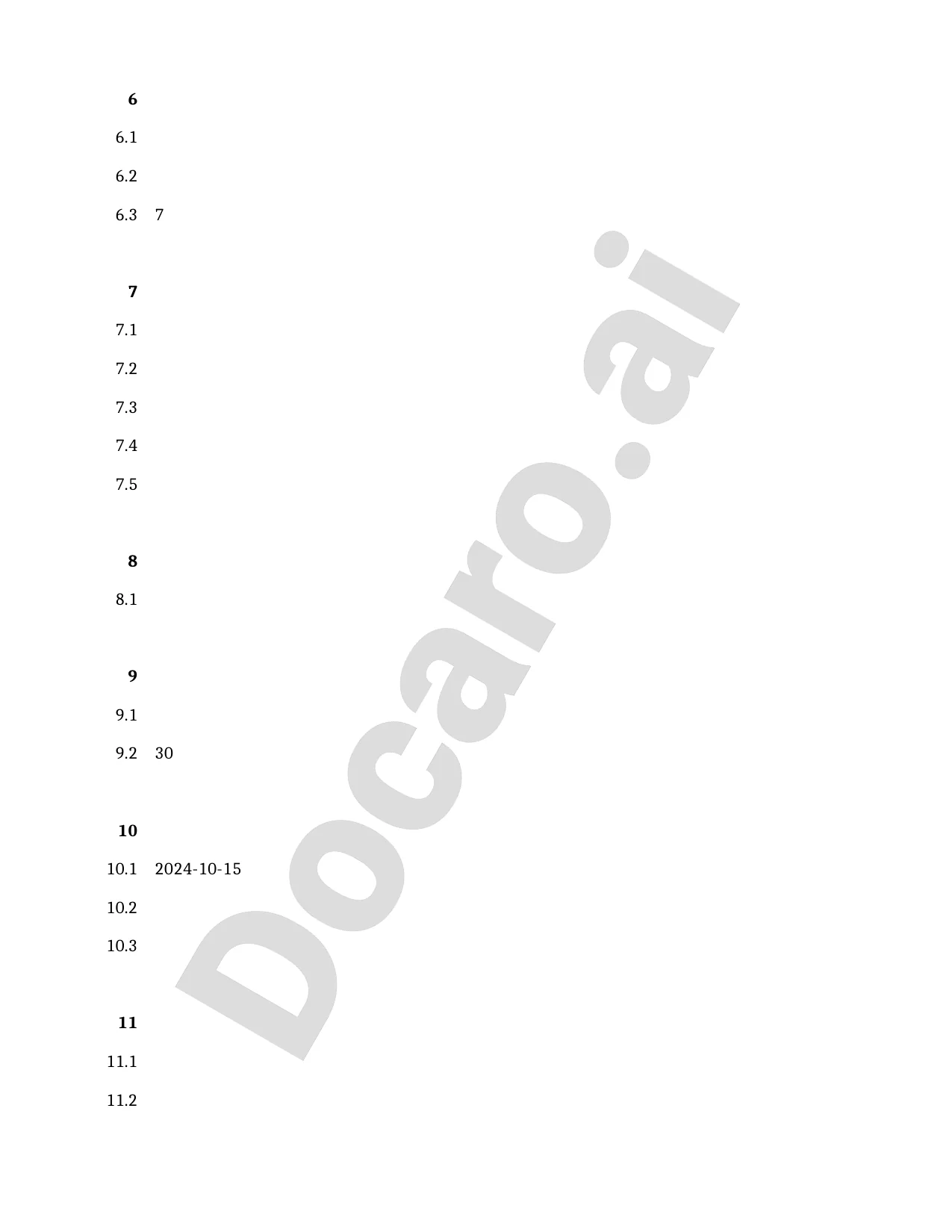

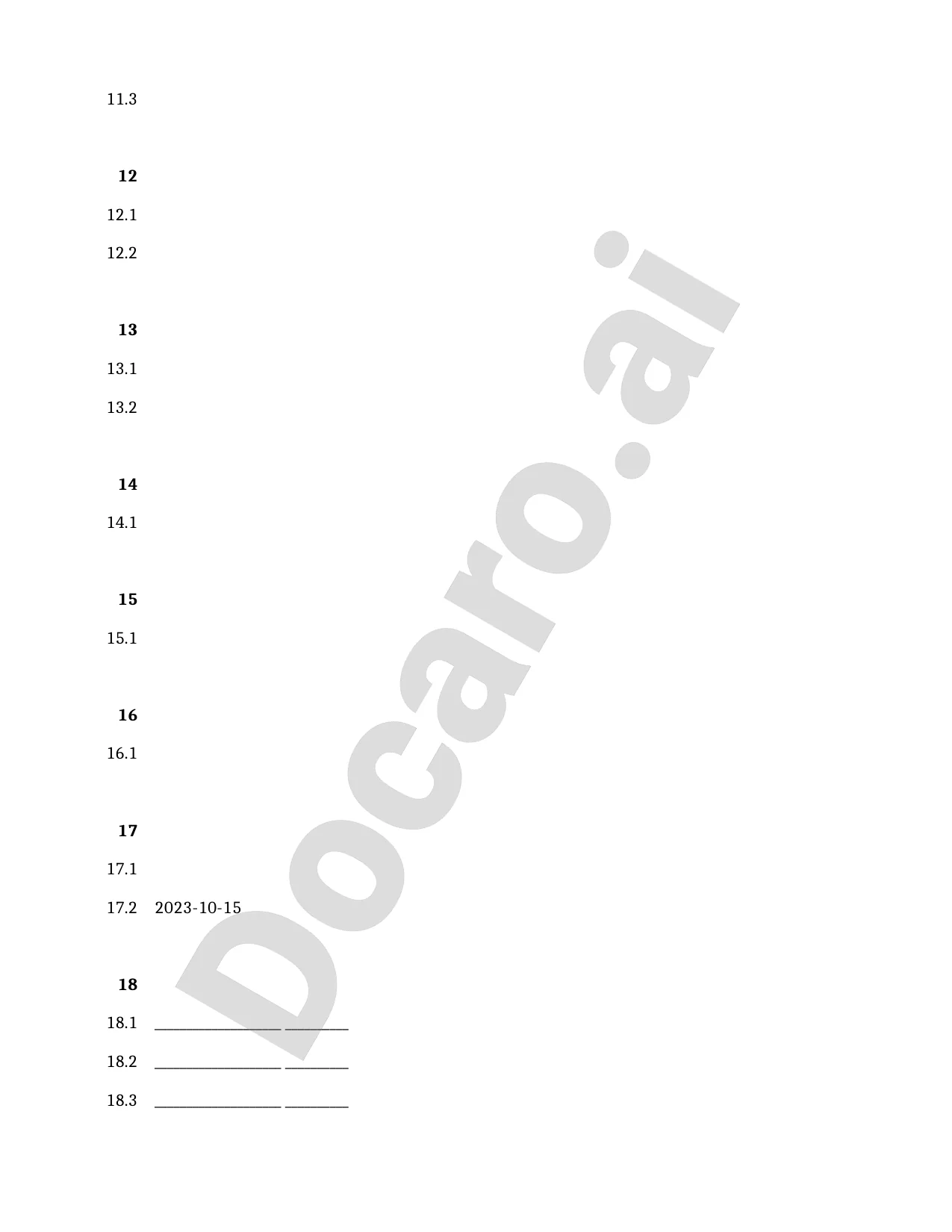

中国免费示例 抵押契约 模板

以下是我们的 AI 模型生成的免费 抵押契约 模板示例,用于在 中国 中使用。

您实际 抵押契约 中的条款将与此示例有所不同,因为它们将完全根据您在问卷中设定的要求量身定制。

Page 1

Page 2

Page 3

Page 4

考虑在 中国 选择 抵押契约 时有用的资源

www.lawsociety.org.uk

www.london-law.co.uk

www.lawsociety.org.uk

www.sra.org.uk

www.taylor-rose.co.uk

deanwilson.co.uk

www.premiersolicitors.co.uk

adkirklawconveyancing.co.uk

www.lawsociety.org.uk

www.sra.org.uk

中国 参考立法

以下立法与在中国生成抵押契约有关:

•

该法规范了抵押权的设立、效力、转移和消灭,包括抵押合同和抵押登记的相关规定,是抵押权的基础法律。

•

规定了抵押担保的法律要件、抵押物范围、抵押登记和抵押权的实现等内容,适用于抵押合同的形成和执行。

•

2021年生效的民法典整合了原物权法和担保法,详细规定了抵押权的设立、登记、转让和优先受偿等规则,是当前主要适用法律。

•

规范抵押合同的订立、效力、违约责任等一般规则,抵押合同作为一种担保合同受其调整。

常见问题

抵押契约是指债务人或第三人不转移财产所有权,将财产抵押给债权人,以担保债务履行的法律文件。在中国,根据《民法典》和《担保法》,抵押契约必须明确抵押财产、债务金额、期限等内容,确保双方权利义务清晰。

文档生成常见问题解答

Docaro 是一款由人工智能驱动的法律和公司文件生成器,可帮助您在几分钟内创建格式完整的法律合同和协议。只需回答几个引导性问题,即可立即下载您的文件。

您可能还对

相关文章

深入了解中国抵押契约的法律定义、基本要求及相关规定。本文详解抵押权设立、登记程序及常见问题,帮助您掌握房地产抵押的核心知识。

本文详细讲解如何在房地产交易中正确使用抵押契约,包括定义、签署步骤、法律注意事项及常见错误。帮助您顺利完成房产买卖,避免风险。

全面解答抵押契约常见问题,包括签订注意事项、法律风险及有效防范策略。帮助您避免合同纠纷,保护权益。专业法律指导,实用建议一网打尽。