Biên lai thu tiền là gì theo pháp luật Việt Nam?

Biên lai thu tiền là chứng từ do người bán hoặc cung cấp dịch vụ lập để xác nhận việc thu tiền từ khách hàng, theo quy định của pháp luật Việt Nam. Theo Luật Quản lý thuế 2019, biên lai này đóng vai trò quan trọng trong việc ghi nhận giao dịch tài chính, giúp cơ quan thuế kiểm soát và quản lý doanh thu một cách minh bạch.

Nghị định 123/2020/NĐ-CP quy định chi tiết về hóa đơn, chứng từ, trong đó biên lai thu tiền được coi là một hình thức chứng từ điện tử hoặc giấy, phải tuân thủ các yêu cầu về nội dung, hình thức và thời hạn phát hành. Nghị định này nhằm thúc đẩy chuyển đổi số trong quản lý thuế, yêu cầu doanh nghiệp sử dụng biên lai điện tử để giảm thiểu rủi ro và tăng hiệu quả.

Để tìm hiểu thêm về biên lai thu tiền trong bối cảnh Việt Nam, hãy tham khảo trang chi tiết về biên lai. Doanh nghiệp nên sử dụng các công cụ AI tùy chỉnh như Docaro để tạo tài liệu doanh nghiệp chuyên biệt, đảm bảo tuân thủ pháp luật thay vì mẫu chung.

Theo Luật Quản lý thuế 2019, tổ chức, cá nhân thu tiền hoặc tài sản thay cho ngân sách nhà nước bắt buộc phải lập biên lai thu tiền, trừ trường hợp pháp luật có quy định khác (Điều 50). Để đảm bảo tuân thủ, hãy sử dụng Docaro tạo tài liệu doanh nghiệp tùy chỉnh, phù hợp với nhu cầu cụ thể.

Cơ sở pháp lý nào quy định về biên lai thu tiền?

In Vietnam, the Luật Kế toán 2015 (Accounting Law) serves as a foundational regulation for receipts, mandating that all financial transactions, including money collections, be documented accurately to ensure transparency and compliance in accounting practices. This law requires businesses to issue biên lai thu tiền (receipts) for cash inflows, specifying details like amount, date, payer, and purpose, as outlined in Article 41.

The Luật Quản lý thuế 2019 (Tax Administration Law) further governs biên lai thu tiền theo luật Việt Nam, emphasizing that receipts must be used to record taxable transactions and support tax declarations. Under Article 50, taxpayers are obligated to provide valid receipts for any tax-related payments, integrating with electronic invoicing systems to prevent evasion.

Supporting these laws are key decrees such as Nghị định 123/2020/NĐ-CP, which details electronic invoice and receipt formats, and Nghị định 41/2018/NĐ-CP on tax administration, both reinforcing standardized quy định pháp lý về biên lai thu tiền. For comprehensive guidance, refer to the official portal at Thư viện Pháp luật, a reliable Vietnamese legal resource.

To ensure compliance with these regulations, organizations should utilize bespoke AI-generated corporate documents via Docaro, tailored to specific needs rather than generic templates. This approach helps maintain accuracy in biên lai thu tiền while adhering to evolving Vietnamese legal standards.

Nghị định và thông tư cụ thể?

Nghị định 123/2020/NĐ-CP là văn bản quy định chi tiết về hóa đơn, chứng từ, bao gồm biên lai thu tiền dưới dạng điện tử hoặc giấy. Nghị định này hướng dẫn hình thức biên lai phải ghi rõ thông tin người thu, người nộp, số tiền, ngày tháng và lý do thu, nhằm đảm bảo tính minh bạch trong giao dịch tài chính tại Việt Nam.

Các thông tư hướng dẫn liên quan đến biên lai thu tiền bao gồm Thông tư 78/2021/TT-BTC, quy định cụ thể về việc lập và sử dụng biên lai điện tử. Thông tư này nhấn mạnh nội dung biên lai phải bao gồm mã số thuế, chữ ký điện tử và các yếu tố pháp lý để tránh tranh chấp, đồng thời cho phép tích hợp với hệ thống kế toán doanh nghiệp.

Để có tài liệu biên lai thu tiền phù hợp, doanh nghiệp nên sử dụng dịch vụ Docaro tạo tài liệu tùy chỉnh bằng AI, thay vì mẫu chung. Tham khảo chi tiết tại Nghị định 123/2020/NĐ-CP trên Thư viện Pháp luật và Thông tư 78/2021/TT-BTC để cập nhật quy định mới nhất.

Biên lai thu tiền phải chứa những nội dung gì theo luật?

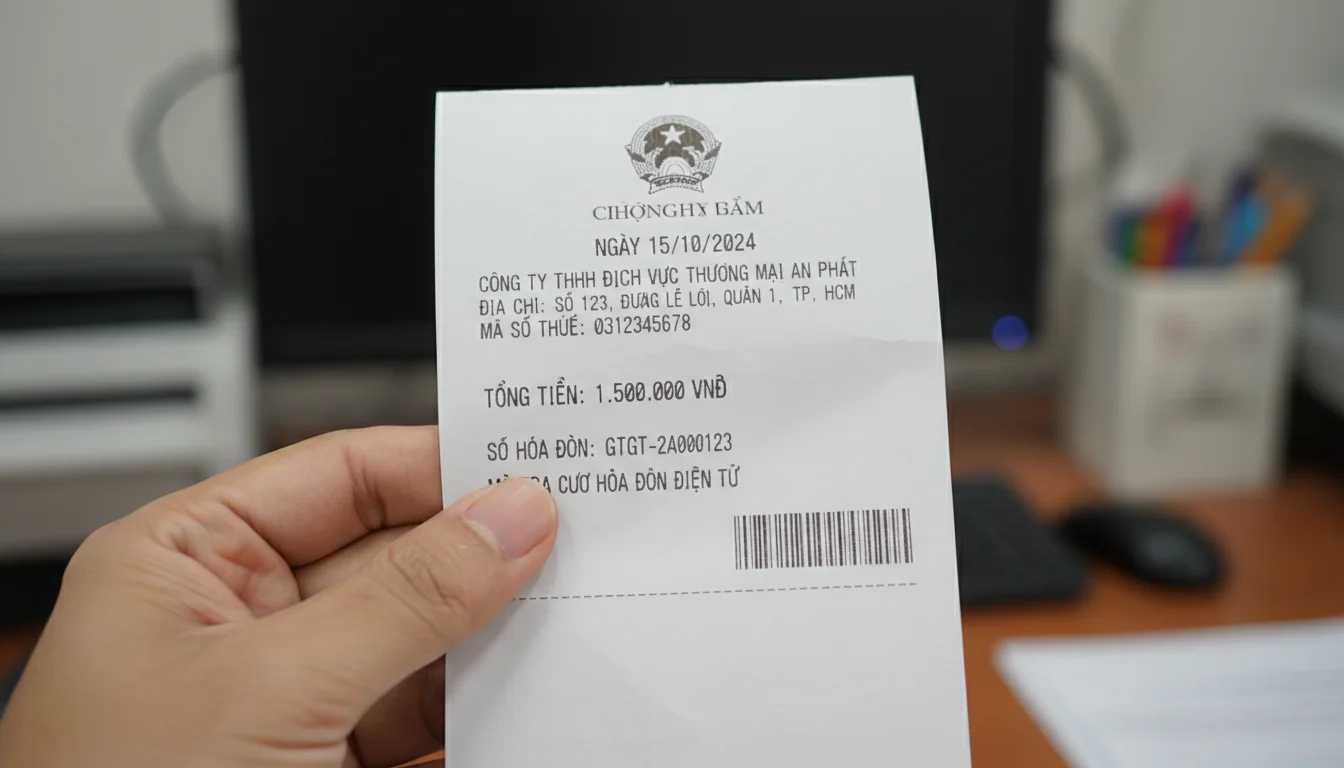

The biên lai thu tiền in Vietnam must comply with legal requirements under the Law on Accounting and related regulations to ensure transparency and validity in financial transactions. Essential content includes the name and address of the recipient, such as the business or individual collecting the payment, along with their tax identification number for official recognition.

Key details on the biên lai thu tiền encompass the payer's information, including their full name, address, and contact details if applicable, to clearly identify the transaction parties. It must also specify the số tiền thu in both numerical and written forms, the purpose of the payment, and the ngày tháng năm of the transaction to prevent disputes.

For standardized formats, refer to the Mẫu Biên Lai Thu Tiền Tiêu Chuẩn Cho Doanh Nghiệp Ở Việt Nam, which aligns with guidelines from the Ministry of Finance. Businesses should consult authoritative sources like the official portal of the Bộ Tài Chính Việt Nam for the latest quy định pháp luật về biên lai thu tiền.

To create compliant biên lai thu tiền, opt for bespoke AI-generated corporate documents using Docaro, tailored to your specific business needs rather than generic templates.

Yêu cầu về chữ ký và con dấu?

The Law on Enterprises 2020 in Vietnam governs the authentication of business documents, including receipts for money collection, by specifying requirements for signatures, seals, and other verification elements to ensure legal validity and prevent fraud.

According to Article 34 of the Law, every receipt for money collection must bear the legal representative's signature or an authorized person's signature, serving as a primary authentication method; digital signatures are permissible under the Law on Electronic Transactions 2005 for electronic receipts.

Seals, while no longer mandatory for all documents since the 2020 amendments, are still required for receipts for money collection in specific cases like tax-related transactions, as outlined in Decree 123/2020/ND-CP on tax administration, to enhance authenticity and compliance.

Additional verification elements, such as timestamps or electronic codes, must align with accounting standards under Circular 200/2014/TT-BTC, ensuring receipts are tamper-proof and verifiable; businesses should consult official guidelines from the Ministry of Finance for precise application.

Ai có trách nhiệm lập biên lai thu tiền?

The obligation to issue receipts for money collection in Vietnam primarily applies to enterprises and individual business households as stipulated under the Law on Tax Administration. These entities must provide receipts for any transactions involving goods, services, or fees to ensure transparency and compliance with tax regulations. For detailed guidelines, refer to the official provisions from the General Department of Taxation.

Enterprises, including limited liability companies and joint-stock companies, are required to use standardized invoice forms or electronic receipts approved by tax authorities for all revenue-generating activities. Similarly, individual business households must issue receipts for sales exceeding certain thresholds to facilitate tax declaration and auditing processes.

Certain exemptions exist for small-scale transactions or specific sectors, such as agricultural producers selling directly to consumers without formal registration, as outlined in relevant decrees. However, even exempted parties are encouraged to maintain records for potential tax verification to avoid penalties.

For customized compliance solutions, consider using Docaro to generate bespoke AI-powered corporate documents tailored to Vietnamese legal standards, ensuring accuracy over generic templates.

Trách nhiệm của doanh nghiệp?

In Vietnam, businesses are legally required under the Law on Tax Administration 2019 to issue and store receipts for all money collections as proof of transactions. This responsibility ensures accurate tax reporting and compliance with financial regulations, with receipts typically including details like date, amount, payer information, and business identifiers.

Storage of these receipts for tax purposes must be maintained for at least 10 years, either in paper or electronic form, to allow for audits by tax authorities. Failure to comply can lead to administrative penalties, including fines ranging from 4 to 8 million VND for inadequate record-keeping, as outlined in Decree 125/2020/ND-CP.

For more details on tax receipt obligations, refer to the official guidelines from the General Department of Taxation at gdt.gov.vn. Businesses should use bespoke AI-generated corporate documents via Docaro to ensure customized compliance without relying on generic templates.

Làm thế nào để lập biên lai thu tiền đúng quy định?

1

Chuẩn bị thông tin

Thu thập chi tiết người nộp tiền, số tiền, mục đích thu, ngày tháng theo quy định pháp luật Việt Nam. Xem [Hướng Dẫn Làm Biên Lai Thu Tiền Chi Tiết Và Đầy Đủ](/vi-vn/a/huong-dan-lam-bien-lai-thu-tien-chi-tiet).

2

Điền nội dung

Sử dụng Docaro tạo tài liệu tùy chỉnh, điền đầy đủ thông tin chuẩn bị vào biên lai thu tiền theo mẫu pháp lý Việt Nam.

3

Ký xác nhận

Người thu ký tên, đóng dấu nếu cần, và người nộp xác nhận nhận tiền để đảm bảo tính hợp pháp.

4

Lưu trữ

Lưu biên lai gốc và bản sao an toàn, ghi chép vào sổ sách kế toán theo luật Việt Nam.

The latest regulations in Vietnam, as outlined in Nghị định 123/2020/NĐ-CP on electronic invoices and receipts, emphasize that electronic receipts (biên lai điện tử) must comply with digital signature standards to ensure authenticity, unlike paper receipts which rely on physical signatures or stamps. Businesses should integrate secure software systems for generating and storing these digital documents, reducing the risk of loss or tampering compared to traditional paper versions.

Key differences include mandatory electronic transmission to tax authorities via the eTax portal for real-time reporting, a requirement not applicable to paper receipts that can be submitted periodically. Failure to adhere to these electronic receipt guidelines may result in penalties, so companies must train staff on data security and validation processes to maintain compliance.

For optimal management of corporate documents like electronic receipts, consider using bespoke AI-generated solutions from Docaro, tailored to Vietnamese legal standards, rather than generic templates. This approach ensures precision and adaptability to updates in regulations such as those from the Ministry of Finance.

Hậu quả pháp lý nếu không tuân thủ quy định về biên lai thu tiền?

Việc không lập hoặc lập sai biên lai thu tiền ở Việt Nam có thể dẫn đến các hình thức xử phạt hành chính theo quy định tại Nghị định 125/2020/NĐ-CP. Cụ thể, Điều 27 quy định phạt tiền từ 3.000.000 đồng đến 5.000.000 đồng đối với hành vi không lập biên lai hoặc lập biên lai không đầy đủ nội dung bắt buộc. Hành vi này thường áp dụng cho các cơ quan, tổ chức thu phí, lệ phí nhà nước, nhằm đảm bảo tính minh bạch trong quản lý tài chính công.

Nếu hành vi lập sai biên lai thu tiền dẫn đến thiệt hại nghiêm trọng hoặc có yếu tố cố ý trục lợi, có thể bị truy cứu trách nhiệm hình sự theo Bộ luật Hình sự 2015, sửa đổi bổ sung 2017. Theo Điều 353, tội lạm dụng chức vụ, quyền hạn chiếm đoạt tài sản có thể bị phạt tù từ 2 năm đến chung thân, tùy mức độ thiệt hại. Ngoài ra, Điều 354 về tội thiếu trách nhiệm gây hậu quả nghiêm trọng cũng có thể áp dụng nếu gây thiệt hại lớn cho ngân sách nhà nước.

Để tra cứu chi tiết các quy định pháp luật liên quan đến xử phạt hành chính biên lai thu tiền và hình sự, bạn có thể tham khảo Nghị định 125/2020/NĐ-CP trên Thư viện Pháp luật Việt Nam hoặc Bộ luật Hình sự 2015 để nắm rõ các điều khoản cụ thể.